This post was updated on April 13, 2023 to reflect clarifications on two cited publications.

Investments in place matter. Public spaces such as parks and community centers as well as businesses such as restaurants and bars signal local prosperity, add a richness to the neighborhood, and enhance community wealth by attracting further investment.

Grocery stores are a crucial component of this ecosystem. And premium grocery chains focused on natural, organic, and specialty foods (commonly referred to as “fresh format” stores) such as Whole Foods and Trader Joe’s1 not only provide healthy shopping options for residents, but also serve as markers of high-income, desirable areas, which contributes to increased property values and an image of security and stability. Conversely, the lack of these assets—or the proliferation of chains associated with poverty, such as dollar stores—can indicate to investors and developers that a community is struggling or lacks a clientele that would make investing profitable. These patterns can drive an upward or downward spiral of investment, concentrating wealth in already-wealthy areas while diverting it from struggling ones.

Community investment patterns are often influenced by race as well as wealth. Analyzing the distribution of grocery stores in several large U.S. cities, we find that premium grocery stores are less likely to be located in Black-majority neighborhoods, regardless of the average household income of those neighborhoods, and are substantially more likely to be located in neighborhoods where the Black population share is less than 10%.

In other words, businesses and the broader real estate and financing sectors are not investing even in prospering Black-majority neighborhoods, which devalues these communities and hinders opportunities for growth.

Devaluation of Black communities has led to disparities in food access

Uneven food systems across neighborhoods of varying racial compositions reveal ways that American society signals the value it places on the people in those communities.

The devaluation of Black neighborhoods is linked with redlining and mid-20th century “urban renewal” projects that labeled many Black neighborhoods as “slums” and demolished them. Meanwhile, federal, state, and local leaders invested in infrastructure that brought suburban white residents to and from urban cores, signaling the higher intrinsic value of white communities. These policies acted on the presumed lower value of people and assets in Black communities, which shows up in the kinds of amenities a community offers.

Federal Housing Finance Agency appraisal reports have allowed researchers to confirm that homes in Black neighborhoods are valued roughly 20% lower than equivalent homes in non-Black neighborhoods, and are nearly twice as likely to appraise below the contracted selling price. Similar devaluation patterns have been found in commercial real estate in Black-majority neighborhoods, which makes it difficult for Black entrepreneurs to get loans to start new businesses or invest in existing ones. Customer-facing businesses that do establish themselves in Black-majority neighborhoods face lower customer ratings and less revenue.

One part of the larger structure of business and commercial real estate devaluation in Black-majority communities is “food apartheid,” or disparities in access to food that have been produced by structural racism in residential and investment patterns, such as supermarket redlining. Though differences in food access are often blamed for elevated food insecurity and worse nutritional outcomes in Black communities, the relationship may not be as strong as is often believed, as our Brookings Metro colleagues pointed out in a 2021 report. They found that while there has been a tendency to frame the problem of food insecurity and poor nutrition in low-income neighborhoods as one of “food deserts” (areas with limited access to affordable and nutritious food), a number of recent studies have shown that greater access to food retailers does not correlate to reduced food insecurity, and that shoppers, even those without vehicles, do not necessarily choose to shop at the nearest supermarket.

Furthermore, the rise of food delivery services during the COVID-19 pandemic has resulted in greater access to grocery delivery services for most Americans living in traditionally defined “food deserts.” While financial insecurity and the higher cost of healthier food play a bigger role in food insecurity and nutritional deficits among low-income Americans, segregation and differing retail options in Black-majority neighborhoods still matter, because they are symptoms of a broader problem of devaluation and underinvestment in Black communities, which has real consequences for local wealth retention and development.

Beyond issues of access, this report presumes that store type is an economic statement of value that can spur or throttle investment in an area. The store types present in a community are a judgement of the level of investment a community is worthy of.

Premium grocery stores are absent from wealthy Black-majority communities

We analyzed the locations of premium grocery retailers in 10 U.S. metro areas with populations over 1 million and substantial numbers of high-income, non-rural census block groups with Black-majority populations.2 We found strong evidence for underinvestment across all 10 metro areas.

As seen in Table 1, in seven of the 10 metro areas studied, none of the Black-majority, non-rural block groups in the top quartile for household income were located within 1 mile of a premium grocery store and only in one metro area—Washington, D.C.—was the percentage above 5%. For block groups in the same income brackets but with less than a 10% share of Black residents, the percentage that were located within 1 mile of a premium grocery store ranged from 10% in Atlanta to 34% in Los Angeles. Furthermore, Black-majority block groups in each income quartile of all the metro areas studied had a lower chance of being within 1 mile of a premium grocery store than block groups in that metro area overall.3

While we see the same pattern of underinvestment in wealthy Black communities across all 10 cities in our sample, there are significant differences between metro areas as well. Figure 1 highlights the difference in the shares of Black and non-Black neighborhoods near premium grocery stores. The differences in premium grocery store prevalence in wealthy neighborhoods are lowest in the low-income metro areas (New Orleans and Memphis, Tenn., which have median household incomes below $60,000), and largest in Washington, D.C., New York, and Los Angeles (which are among the wealthiest metro areas in our sample).

Another difference appears when we look at low-income block groups. In some metro areas (Atlanta and Baltimore in particular), the deficit of premium grocery stores is similar across low-income and high-income Black neighborhoods. However, in two metro areas (Houston and Chicago), Black-majority communities in the bottom income quartile were actually more likely to be located near a premium grocery store than low-income communities with few Black residents. In both cases, the differences are small, and the low-income Black neighborhoods in question are in relatively dense urban areas adjacent to higher-income neighborhoods.

Comparing premium grocery store locations in the Washington, D.C. and Atlanta metro areas

The Washington, D.C. metro area is the highest-income metro area that we studied, with a median household income of $111,000 according to 2021 American Community Survey (ACS) 5-year estimates. It is also home to Prince George’s County and Charles County in Maryland, the second-highest and highest-income Black-majority counties in the country. Still, our analysis demonstrates the differences in investment distributions between Black-majority and predominantly white neighborhoods. For example, the absence of high-end retailers, including premium grocery outlets, in Prince George’s County has been a point of concern in those high-income Black communities for decades.

The Washington, D.C. area is home to roughly 20 Trader Joe’s and Whole Foods locations each, as well as two local organic chains: MOM’s Organic Market and Yes! Organic Market. The national chains are much more likely to be located in neighborhoods with few Black residents across the income spectrum, while the two local chains show a much smaller racial disparity. In the case of Yes! Organic Market, this is partly a consequence of the fact that all of their stores are located in the urban core—often in gentrifying areas—and thus close to historically Black communities. However, it may also be evidence that locally owned stores are less likely to undervalue Black neighborhoods than national chains with less familiarity with the areas where they operate.

As seen in Figure 2, a belt of high-income block groups with Black-majority populations wraps roughly a third of the way around the Capital Beltway in the District’s eastern and southern suburbs. However, while high-income areas in other parts of the Washington, D.C. suburbs are scattered with Whole Foods, Trader Joe’s, and MOM’s Organic Market locations, the two MOM’s locations in the belt are near its ends, in areas with less predominately Black populations, and neither of the national chains has any locations in the belt. In fact, while each of the chains has a single location in Prince George’s County and none in Charles County, these stores are located within a mile of each other, and very near the University of Maryland’s flagship campus, in a part of the county that is not majority-Black.

A similar pattern is seen in the locations chosen by the Kroger-owned conventional grocery retailer Harris Teeter (Figure 3), which began to move into the Washington, D.C. area in the early 2000s and has focused its expansion on upscale markets. Although Harris Teeter is now the third-largest grocery chain in the region with 44 stores, it has no stores in Charles County and only two in Prince George’s County—neither in a Black-majority neighborhood and both near the county’s border with majority-white Baltimore suburbs.

The distribution of premium grocery chains in Atlanta, shown in Table 3 and Figure 4, provides a good comparison to Washington, D.C., since Atlanta has the smallest percentage of top-quartile block groups within 1 mile of a premium grocery store among the metro areas we studied. While relatively few block groups in the Atlanta area are located near premium grocery stores, nearly all of those that are have few Black residents.

Premium grocery stores are rare overall in the Atlanta area, but the ones that are present are nearly all confined to a corridor running north of downtown that has some of the region’s smallest shares of Black residents. The major suburban “edge city” job clusters of Buckhead and Perimeter Center are also home to pairs of premium grocery stores.

Dollar stores are more common in Black-majority communities at all income levels

The absence of premium grocers from even high-income Black-majority communities is an example of the disinvestment side of food apartheid. However, there is a second component to the different food retail ecosystems in Black and non-Black (especially white) neighborhoods: the prevalence of less-desirable food options. Studies have shown that the prevalence of fast-food restaurants is positively correlated with the percentage of Black residents in urban neighborhoods in the U.S. Similar trends have been found for liquor stores.

Chain dollar stores are one example of food retailers that have targeted Black-majority urban neighborhoods for store locations, often saturating these communities with outlets and making it more difficult for local businesses and other grocery chains to become established. While dollar stores can fill a need in low-income neighborhoods, they are often regarded as predatory businesses that harm communities more than they benefit them, due to very low wages, displacing other grocery options while failing to sell fresh food, store design that increases the rate of armed robberies, and OSHA and FDA violations that put customers and employees at risk.

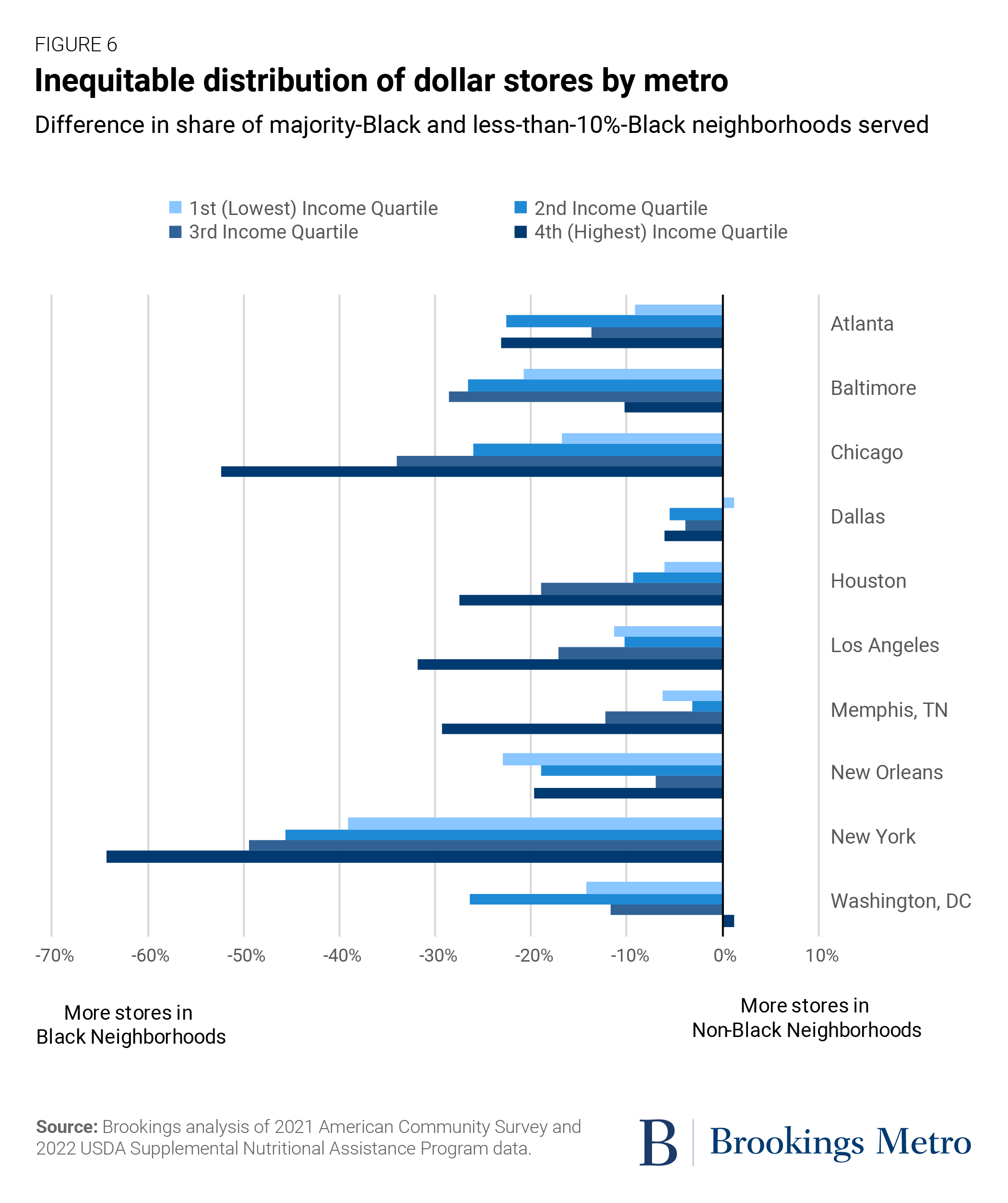

As shown in Table 4, in every metro area in our cohort except Washington, D.C. (where dollar stores are less prevalent overall, likely due to the metro area’s substantially higher incomes), Black-majority neighborhoods in the top income quartile were more likely to have a dollar store within 1 mile than high-income neighborhoods with a share of Black residents lower than 10%. Furthermore, in six of the 10 metro areas (New York, Los Angeles, Chicago, Houston, New Orleans, and Memphis), most Black-majority neighborhoods in the top income quartile were within 1 mile of a dollar store. In fact, in New York and Chicago, Black-majority neighborhoods in the top income quartile were more likely to be near a dollar store than non-majority-Black neighborhoods in any income quartile.

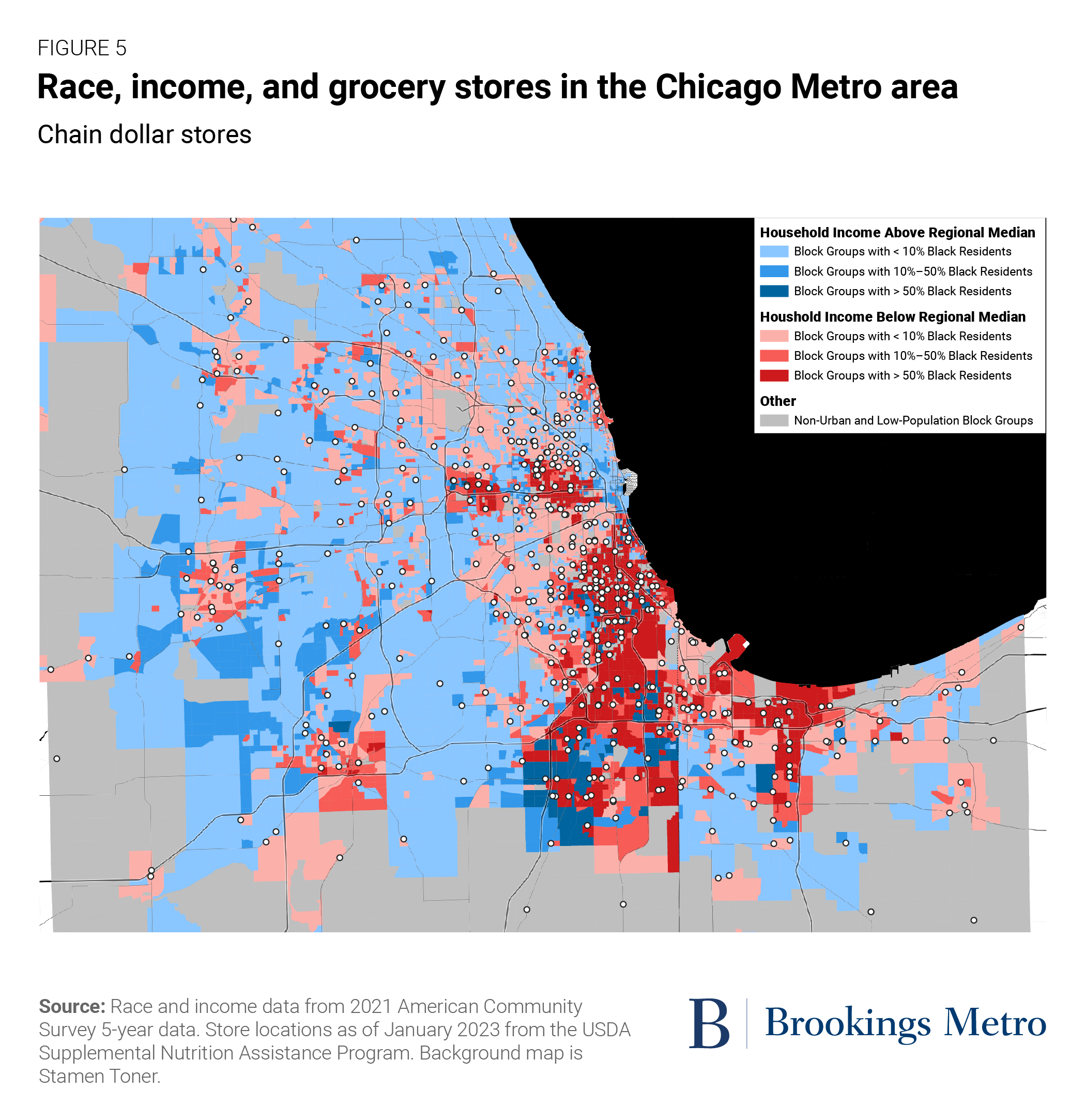

Figure 5 shows the situation in Chicago, where dollar stores are concentrated in and near Black-majority areas, including the higher-income ones south of the city. Dollar stores are significantly less common in areas with few Black residents. While chain dollar stores are much more numerous than fresh-format grocery stores, they still concentrate in neighborhoods with lower incomes and higher shares of Black residents. Many of these neighborhoods have not just one, but a cluster of several dollar stores—making it especially hard for businesses that compete with them to become established.

As shown in Figure 6, Black-majority block groups were more likely than block groups with a share of Black residents lower than 10% to be within 1 mile of a dollar store for each income quartile in each metro area, with two exceptions: the highest quartile in Washington, D.C. (where dollar stores are especially rare) and the lowest quartile in Dallas (where the racial differences in dollar store locations are smallest overall). And while there is an overall trend toward more dollar stores in Black-majority neighborhoods, the patterns in each metro area are very different.

Dallas has especially small differences—never more than 7 percentage points—in dollar store prevalence between Black-majority block groups and those with Black population shares lower than 10%, while there is a very large variation in dollar store prevalence by income, with roughly 85% of lowest-quartile and 30% of highest-quartile block groups within 1 mile of a dollar store. And among cities with substantial racial disparities, these disparities follow different patterns with income. In Washington, D.C., dollar stores are most over-represented in low-income Black neighborhoods, while the difference is smaller in third-quartile neighborhoods and negative in neighborhoods in the fourth income quartile. On the other hand, Atlanta, Baltimore, and New Orleans show similar disparities across income quartiles, while Houston, Los Angeles, Memphis, Chicago, and New York show the biggest disparities in high-income neighborhoods, which have few dollar stores when they have few Black residents but far more when they are majority-Black.

Like other local assets, grocery stores influence investment decisions

No single asset type alone determines the value of a place or the willingness of entrepreneurs, businesses, developers, and private individuals to invest in it. Rather, community, consumption, institutional, and other asset types are all part of a unified ecosystem that creates value and indicates potential investment opportunities.

The decisions food retailers make have obvious direct impacts on residents, such as the length of a trip to their preferred store. But their indirect impacts can be even more important. The presence of premium (or discount) retail in a community can drive the decisions of other retailers to locate in or avoid the community, thus strengthening or weakening the tax base. Furthermore, the presence of premium amenities in a community makes it more appealing to wealthier residents, which raises home values and potentially contributes to firms’ decisions on where to locate offices.

The less obvious outcomes of these choices—including their implications for place-based, racialized wealth divides—are no less important. Local assets and infrastructure matter to community well-being and development, and the differences in grocery store chains indicate a broader structural issue of financing practices and corporate underinvestment in Black communities. The tendency to frame this solely as a problem of access has led to suggestions that delivery services can bring about equality between communities. However, disparities in access were always just a symptom of a deeper and more fundamental problem of devaluation and divestment that need to be directly addressed.

Authors

-

Footnotes

- Technically, Trader Joe’s is classified as a “limited assortment” chain, along with Lidl, Aldi, and Save A Lot, because of its small number of items for sale and focus on store brands. However, unlike other limited assortment stores, it focuses on natural, organic, and specialty foods rather than discount products.

- Our panel consisted of metro areas in all four census regions: New York in the Northeast; Chicago in the Midwest; Los Angeles in the West; and Dallas, Houston, Washington, D.C., Atlanta, Baltimore, New Orleans, and Memphis, Tenn. in the South. According to 2021 ACS 5-year estimates, two metro areas (New Orleans and Memphis) have median household incomes at least $10,000 per year below the national median of $69,000 per year, while four (New York, Los Angeles, Washington, D.C., and Baltimore) have median household incomes at least $10,000 per year above the national median.

- Income quartiles were calculated separately for each metro area by ranking non-rural block groups (those where at least 50% of the population lived in a 2020 census urban area) with reported median household incomes. While median household incomes are available for most block groups, they are absent for those with few households—usually parkland or industrial/commercial areas with few residents, or prisons, nursing homes, and college dormitories, where residents live in “group quarters” rather than households.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).