By now the economic impacts of the COVID-19 pandemic are well known. Either you are one of the tens of millions of Americans who has filed for unemployment in the last six months, or you’ve read about the impact on the stock market, hiring, business closures, and functionally every other economic indicator there is. In response, the federal government passed the Coronavirus Aid, Relief, and Economic Security (CARES) Act in March, which provided an array of financial supports for businesses and households to help them weather the financial impacts of widespread economic shutdowns necessitated by the spread of the virus.

Now the federal government is debating a second round of financial support, either through the bills working their way through Congress or through executive actions. Left unaddressed in many of these discussions, however, is that the implementation of the first round of economic supports through the CARES Act often led to long delays, confusion, and frustration for households trying to access their benefits. These delays almost certainly had a disproportionate impact on the economically vulnerable. Households with low incomes and minimal savings would experience a delay in receiving their Economic Impact Payment much differently than higher-income, wealthier households. In this analysis, we examine whether households were able to access the expanded unemployment benefits and Economic Impact Payments offered through the CARES Act during the first months of the pandemic, and the degree to which different groups of people experienced more of a delay in receiving these benefits than others.

The expanded unemployment benefits and Economic Impact Payments were the centerpieces of the supports offered to individual households through the CARES Act. Of the $560 billion allocated to support individual households through the policy, $300 billion went to the Economic Impact Payments and $260 billion financed the expanded unemployment benefits. The amount of these benefits for households were substantial. The expanded unemployment benefits offered an additional $600 per week payment for individuals receiving unemployment insurance, while the Economic Impact Payments offered a one-time payment of $1,200 for every adult and $500 for every child in the U.S. who met the eligibility criteria set by the program.

While these payments were a necessary (if often insufficient) lifeline for struggling households, their implementation was beset by problems. Reports came in from around the country of delays in receiving unemployment benefits after filing for them and, for some people, it took weeks to get through to the unemployment office in order to file for benefits. The way the federal government decided to deliver the Economic Impact Payments also led to delays. If the IRS didn’t have someone’s direct deposit information on file, then that person would either have to enter their direct deposit information online or wait to receive a check in the mail. In practice, this meant that people who didn’t file their taxes in 2018 or 2019—who were often elderly or had low incomes—had to take extra steps to receive their payments.

While it is commonly acknowledged that there were delays in Americans accessing unemployment benefits or receiving their Economic Impact Payments, there is little evidence on exactly who experienced these delays. Given that these two programs functionally represent the entirety of federal legislative efforts to support households during the pandemic, understanding the degree to which different households could or could not access these programs in a timely fashion is an important economic equity issue and can help improve the design of future economic responses to the COVID-19 pandemic or other large-scale crises.

Additionally, disparities in the receipt of these benefits are important because we know that different populations were already much more vulnerable to economic shocks prior to the pandemic. A large body of research demonstrates that low-income households face a combination of low emergency savings and financial volatility that leaves them at regular risk of hardships like food insecurity, eviction, and so on. Related work from the Federal Reserve shows that in 2019—when the economy was close to its pre-pandemic peak—roughly 30 percent of U.S. households could either not currently pay their bills or were one financial setback away from not being able to pay their bills. Additionally, it shows that Black households, Hispanic households, and those with lower educational attainment were uniquely vulnerable. In light of this, it is essential to understand the degree to which these economically vulnerable populations were able to actually access government benefits during this economic crisis.

We use new data from the nationally-representative Socioeconomic Impacts of COVID-19 Survey, administered by the Social Policy Institute at Washington University in St. Louis to roughly 5,500 households between April 29 and May 20 to compare the characteristics of households who received these benefits at the time of the survey against those who did not. To identify whether households who needed unemployment benefits were still waiting for them, we asked respondents whether anyone in their household was currently receiving unemployment benefits. Respondents had four response options to this question: (1) “Yes”; (2) “No, but a member of my household has filed for unemployment benefits”; (3) “No, but a member of my household has attempted to file for unemployment benefits”; and (4) “No.” These response options allow us to distinguish between those who successfully received unemployment benefits and those who needed unemployment but were still stuck in the system, either due to time lags between filing for and receiving unemployment or due to an inability to file for benefits at all (e.g., being unable to reach the unemployment office).

To identify whether respondents were still waiting for their Economic Impact Payments, we asked the following question: “Many households are receiving a relief payment from the federal government (paid by the IRS as a check or direct deposit) as a result of the COVID-19 pandemic. Has your household received this relief payment?” Respondents could answer “yes,” “no,” or “I’m not sure.” Given that the Economic Impact Payments were scheduled to go out in mid-to-late April, those who had not received the payments at the time of the survey (fielded from late April to mid-May) can be considered to have experienced at least some delay in receiving the payments.

Figures 1 and 2 show the overall rates in receiving unemployment benefits and Economic Impact Payments, respectively. In total, 22.5 percent of respondents to our survey had someone in their household who was either receiving unemployment, had filed for unemployment but was waiting to receive payments, or had attempted to file but could not for some reason. We refer to these households as being in the unemployment system. Half of those seeking unemployment (11.9 percent) either had not received their benefit or were unable to apply in late April through mid-May, potentially because they were facing difficulties navigating the unemployment system. Turning to Economic Impact Payments, we see a similar story. Forty-four percent of surveyed households were still waiting to receive their payments in late April through mid-May.

What this means is that roughly half of those households who stood to benefit from these two major federal relief initiatives were left waiting for them even as unemployment was spiking. This likely exposed these households to an increased risk of an array of hardships (food insecurity, skipped bills, etc.) and financial distress.

To investigate if there were any patterns in who was left waiting for these relief payments, we used a technique known as linear probability modeling. This approach allows us to look at the relationship between household characteristics like race/ethnicity, income, age, and so on, and the probability that a given household was left waiting for unemployment benefits or Economic Impact Payments. An advantage of this technique is that it allows us to examine these relationships while controlling for other factors, so we can look at the relationship between, say, race and Economic Impact Payment delays while accounting for other factors like that may affect this relationship, such as differences in income or age.

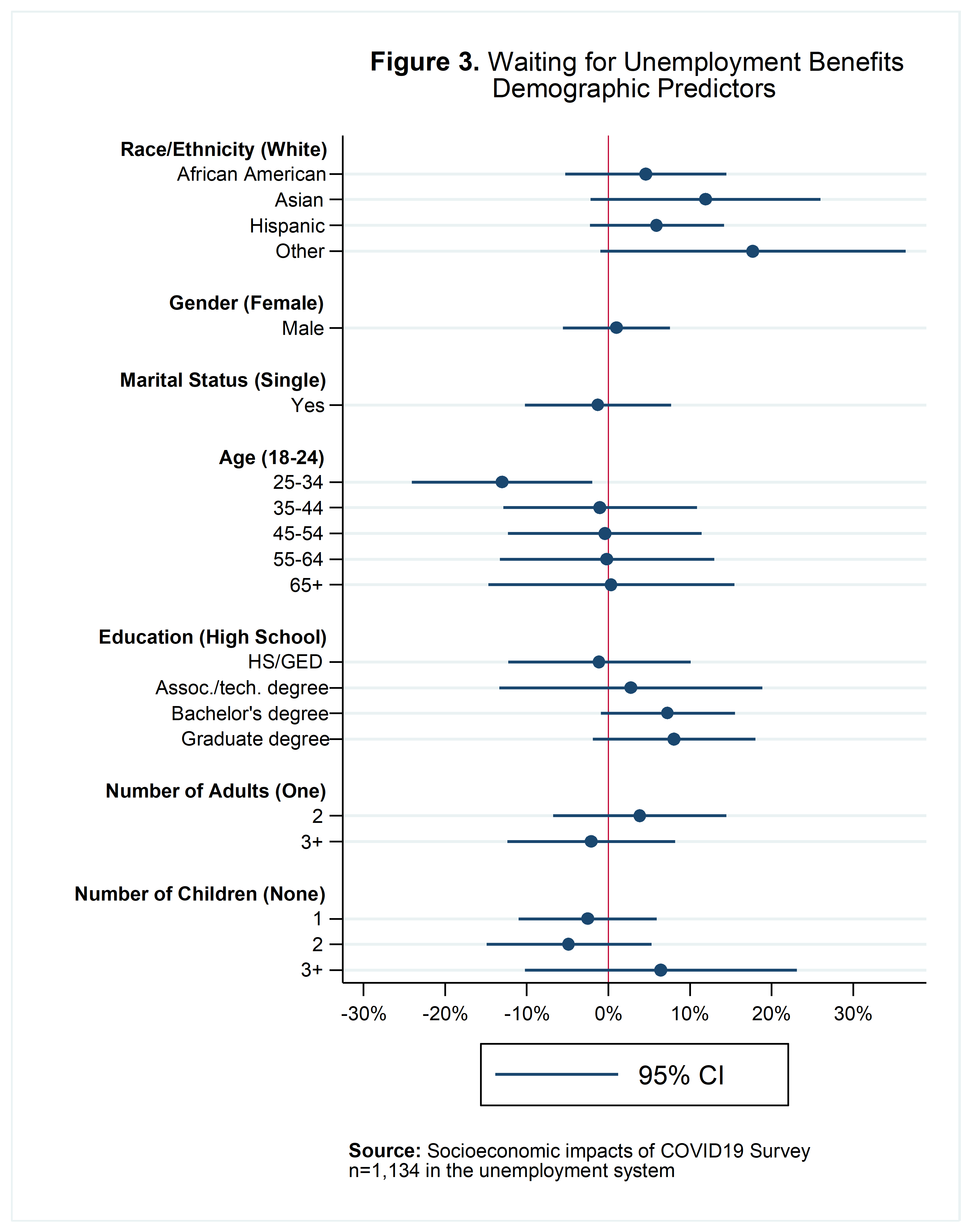

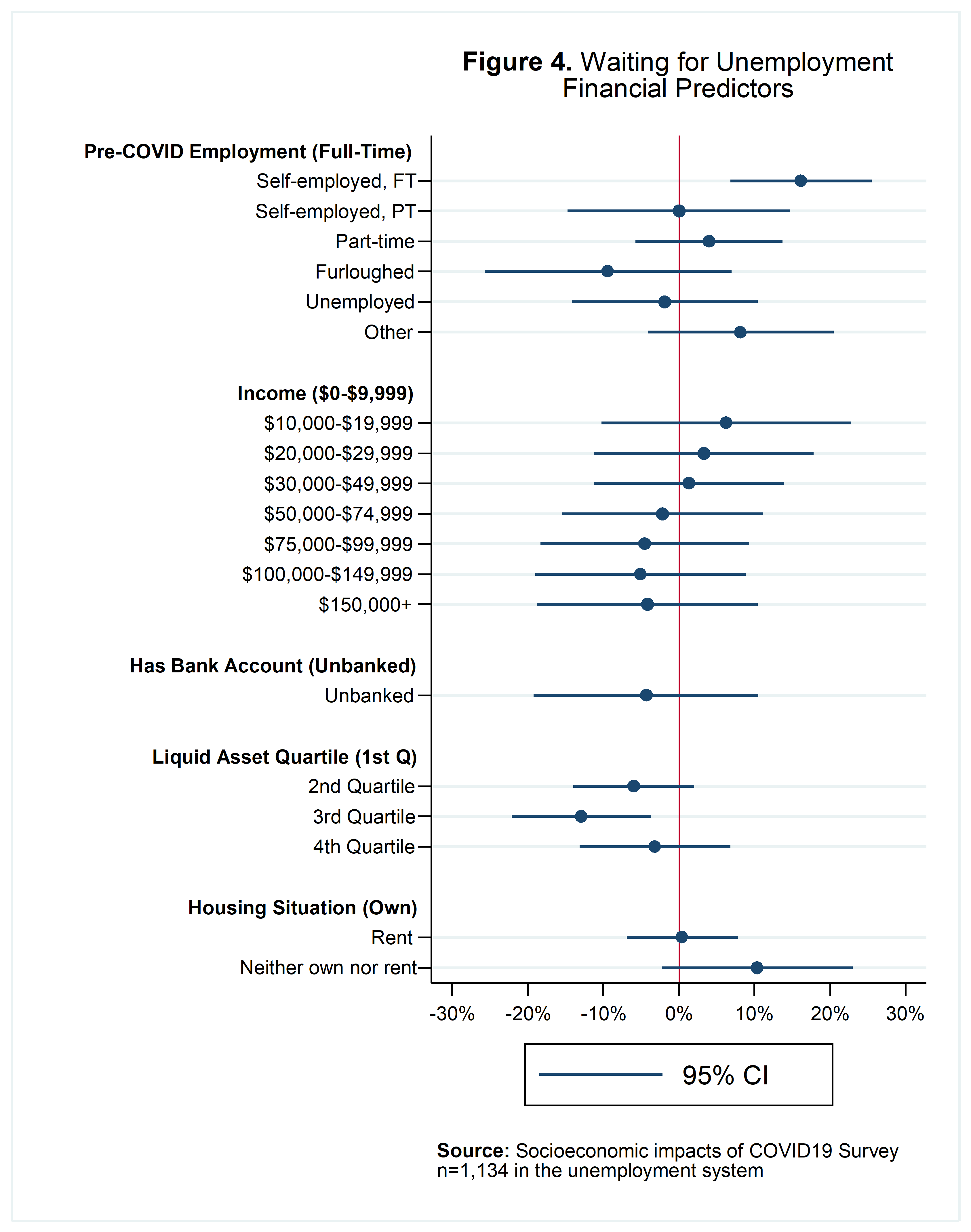

Figures 3 and 4 examine the relationship between waiting for unemployment benefits and household characteristics. We restricted our sample to only those in the unemployment system, allowing us to directly compare those who had received unemployment with those who were still waiting. In these figures, any time a blue bar (the 95 percent confidence interval) crosses the vertical red line at zero, it means there is no statistically significant relationship between a given characteristic and waiting for unemployment.

Interestingly, there is not much of a systematic relationship between household characteristics and waiting for unemployment benefits. A few indicators (certain levels of liquid assets, being self-employed full time, certain age groups, etc.) significantly predict waiting for unemployment insurance, but generally speaking there is limited evidence of any patterns in experiencing unemployment payment delays.

One interpretation of this finding is that everyone—rich or poor, white or minority, with children or without—ran the same risk of waiting for unemployment benefits after they became unemployed. In a sense, this could be seen as a good thing. The strains put on outdated state unemployment systems by the pandemic did not appear to discriminate in their effects. On the other hand, the fact that roughly half of our households were still waiting for unemployment at the time of the survey likely means that large proportions of the most vulnerable—those with low incomes or low savings, or those with children, for example—were stuck in a very precarious situation.

Note: This figure graphs the results of a linear probability model estimating the relationship between household characteristics and having to wait for unemployment benefits. The dots represent the point estimates, and the lines represent the 95 percent confidence interval around those estimates. The reference group for each estimate is in parentheses. For example, with regard to gender we estimate the impact of being male on waiting for unemployment benefits, relative to being female (the reference group).

Note: This figure graphs the results of a linear probability model estimating the relationship between household characteristics and having to wait for unemployment benefits. The dots represent the point estimates, and the lines represent the 95 percent confidence interval around those estimates. The reference group for each estimate is in parentheses. For example, with regard to gender we estimate the impact of being male on waiting for unemployment benefits, relative to being female (the reference group).

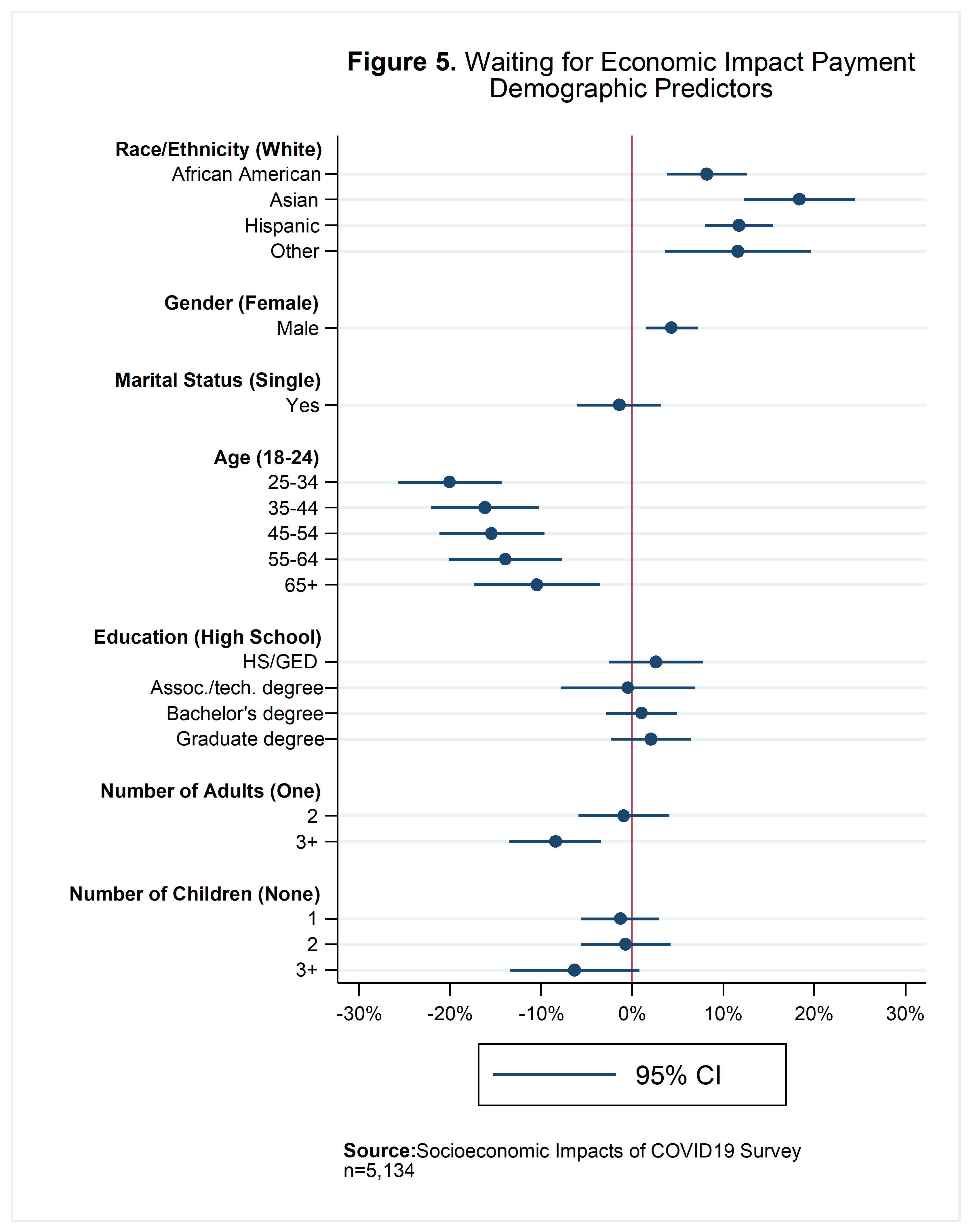

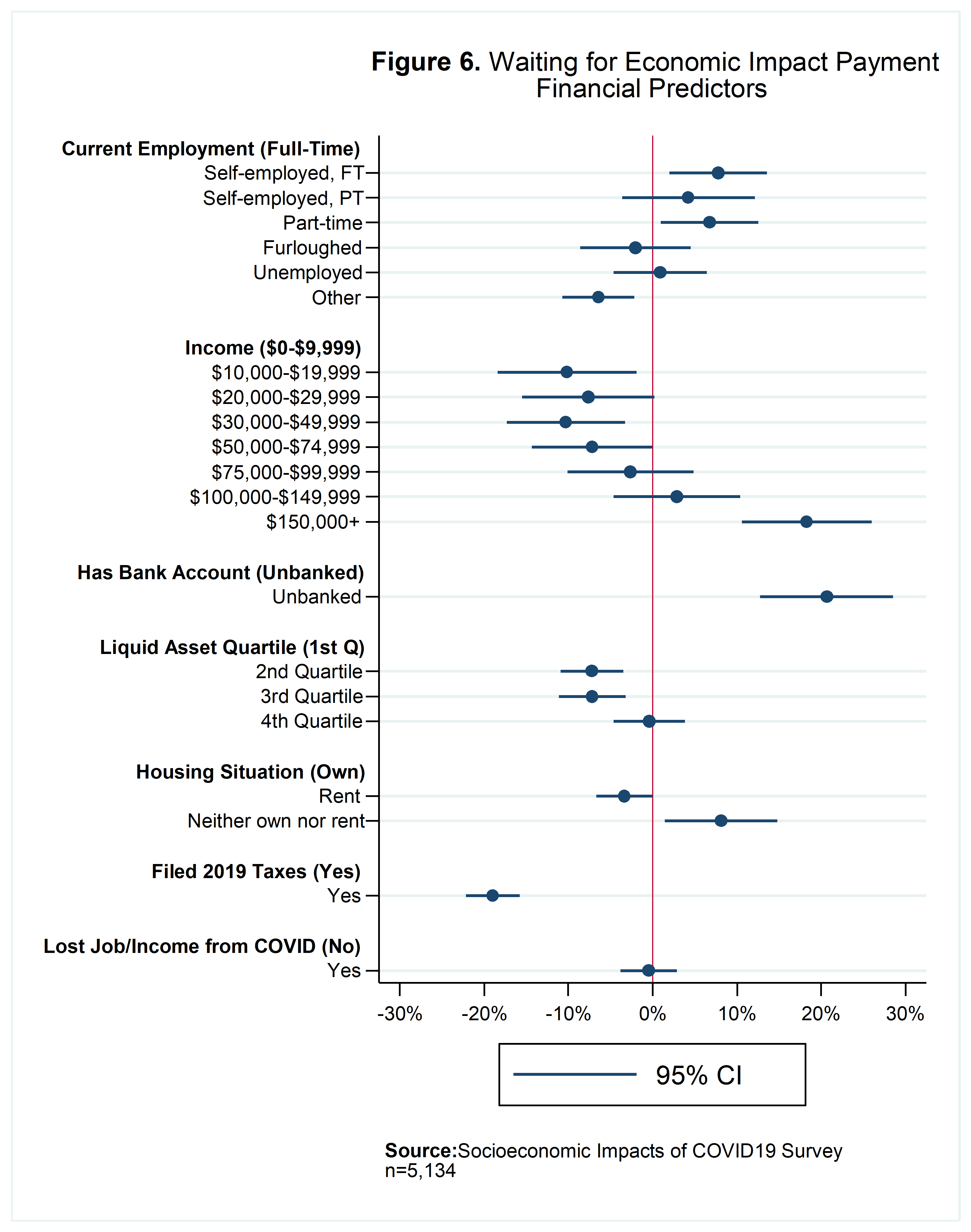

When we examine the relationship between household characteristics and delays in receiving Economic Impact Payments, it is a very different story. Here, we see very strong and consistent relationships between these characteristics and waiting for these payments. Specifically:

- Compared to white respondents, racial minorities were much more likely to experience Economic Impact Payment delays in their households. For example, Black households were 8 percentage points more likely to experience a delay, and Hispanic households were 11 percentage points more likely to experience a delay.

- Men were more likely than women to experience a delay.

- The probability of experiencing a delay decreased as respondents’ age increased.

- Full-time self-employed and part-time wage-and-salary (i.e., not self-employed) respondents were more likely to experience a delay than full-time wage-and-salary respondents.

- Very low-income (less than $10,000 in 2019) households were more likely to experience delays than those with higher incomes.1

- Those without bank accounts and those with low levels of liquid assets were much more likely to experience delays. Specifically, those without bank accounts were 20 percentage points more likely to be waiting for payment than those with bank accounts.

- Respondents who had not filed their 2019 taxes were 18 percentage points more likely to still be waiting for a payment than those who had filed their 2019 taxes.

- Homeowners were less likely to still be waiting for their payment than those who rented or had some other living situation.

Note: This figure graphs the results of a linear probability model estimating the relationship between household characteristics and having to wait for Economic Impact Payments. The dots represent the point estimates, and the lines represent the 95 percent confidence interval around those estimates. The reference group for each estimate is in parentheses. For example, with regard to gender we estimate the impact of being male on waiting for Economic Impact Payments, relative to being female (the reference group).

Note: This figure graphs the results of a linear probability model estimating the relationship between household characteristics and having to wait for Economic Impact Payments. The dots represent the point estimates, and the lines represent the 95 percent confidence interval around those estimates. The reference group for each estimate is in parentheses. For example, with regard to gender we estimate the impact of being male on waiting for Economic Impact Payments, relative to being female (the reference group).

Why are we seeing these patterns? The strong relationships observed between receiving the Economic Impact Payment and bank account ownership or filing 2019 taxes are not surprising. In order to get your Economic Impact Payment quickly, the IRS needed your direct deposit information. They could get this if you filed your taxes and opted to have your tax refund directly deposited to a bank account (assuming you received a refund), or if you entered your direct deposit information through the IRS website. As such, you functionally needed a bank account to receive your payment quickly.

Some of the other relationships are more surprising. Income, race/ethnicity, asset levels, employment, and gender were all predictive of delays in CARES Act receipt. One explanation is that the way the government administered the Economic Impact Payments required individuals to go through a separate process to receive the payments if they didn’t file their taxes, receive a refund, and have direct deposit set up with the IRS. If they didn’t file their taxes, they had to use one of the IRS online tools to access payments. These extra steps, in conjunction with the reports of problems and confusion with the rollout of the IRS payment tools, likely created additional barriers for many people seeking payment.

Our results indicate that these barriers disproportionately affected economically vulnerable households. Households with low incomes or liquid savings, part-time or self-employed households, or those who did not own or rent their own place of residence were more likely to experience delays in Economic Impact Payments, as were very young adult and racial/ethnic minority households. The underlying causes of these relationships are likely complex. For example, it is possible that, even controlling for bank account ownership, some of these groups may have been less familiar with the requirements to receive the payments via direct deposit, or less familiar with the process by which they could share their direct deposit information with the IRS. It is also possible that households with low incomes or low assets, or those with relatively unstable housing situations, had more difficulty accessing the tools provided by the IRS to receive payments quickly. For example, poorer households or those without their own place of residence may have less access to broadband internet connections or computers that would allow them easy access to the relevant websites.

Delays in these payments can have real and severe costs for households. As just one example, research from the Social Policy Institute shows that even a small delay in receiving tax refunds leads to increases in food insecurity in the months after tax filing. Given that our study on delayed refunds was done at a time of economic growth rather than economic collapse, it stands to reason that delays in payments at a time when millions of households are facing steep income declines exposes them to even greater amounts of hardship. This is particularly true when considering the Economic Impact Payments. Delays in these payments disproportionately affected economically vulnerable groups: those with low incomes or low assets, part-time workers, the unbanked, and racial/ethnic minorities. Given that these groups tend to experience higher levels of hardship in good economic times, delaying payments to these groups only serves to make a bad situation worse.

In the early days of the COVID-19 pandemic, policymakers had to act quickly to deliver a massive benefit program to households, businesses, and state and local governments in a very short amount of time. Delays or inconsistencies in the delivery of these benefits to households may have been an inevitable—albeit unfortunate—consequence of the speed with which these programs were implemented. What our research shows is that it was not enough to simply offer these benefits to Americans. Preexisting barriers, such as the inability of state governments to handle massive unemployment shocks or the unequal access to banking services in the United States, hindered the efficient and equitable delivery of these benefits. Going forward, policymakers should seek to either simplify the ways in which households can access economic relief payments or pair these payments with funding support to help government agencies increase their capacity and modernize their infrastructure so they can handle the demands placed on them by this and future crises.

Related Content

Authors

-

Footnotes

- While those with more than $150,000 in 2019 income were also more likely to have not received the Economic Impact Payments, this was likely due in part to the fact that households with more than $198,000 in income were ineligible to receive the payments.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).