Content from the Brookings Doha Center is now archived. In September 2021, after 14 years of impactful partnership, Brookings and the Brookings Doha Center announced that they were ending their affiliation. The Brookings Doha Center is now the Middle East Council on Global Affairs, a separate public policy institution based in Qatar.

Low oil prices, widening fiscal deficits, rising populations, political turmoil, terrorism, religious intolerance and high youth unemployment conjure up a recipe for economic disaster for a region that once controlled the world’s main energy supplies and appeared set fair for long-term economic success. Does the oil curse have the region staring into an economic abyss as fiscal deficits rise?

The current cycle of global oil prices and the consequential erosion of their policies of heavily subsidizing domestic energy consumption have had a dramatic impact on the sovereign wealth fund holdings of the Middle East’s ‘rentier’ states.

Not even the most seasoned economist at the IMF could have predicted the range of economic impacts of the global economic downturn since 2008. Whilst it is still too early to predict with reasonable certainty the outcome of those policies given the recent ‘Grexit’ debacle, austerity policies continue to be prevalent in Western economies, whilst some Asian economies have either reverted to Keynesian economics, or like China, have used direct state intervention to mitigate massive shocks to the stock market.

RISING DEFICITS

In the Middle East however, oil-rich states now have to cope, some for the first time, with rising budget deficits that have necessitated a shift from the classic rentier state economy involving a reduction in their dependence on oil revenues. This major historic shift, which will impact future generations, is increasingly being felt by the current generation of youth as several regional countries suffer mass unemployment, with graduates unable to find employment in the private or public sectors.

The issue of debt management is now a top priority in some Middle East economies, as exemplified by the serious situation faced in Dubai in 2008, when a high profile state-owned entity which led the construction and property sectors, was forced to restructure its debts with a knock-on effect on the rest of that emirate’s economy.

Does this emerging trend signify that the global economy is once again teetering out of balance?

For the past three decades, Middle East sovereign wealth funds to a large extent provided liquidity that helped to bolster the strength of the American dollar, as the pre-eminent global currency, and maintain the dominance of the American banking system. The spectacular growth in credit and the scale of derivatives trading, coupled with rising fiscal budget deficits in the West distorted various asset markets, which were no longer sustainable: sovereign wealth funds were perceived as white knights to the rescue.

The worldwide recession in 2008 led to a rapid collapse in commodity prices and it was only in 2010 before anybody was talking of recovery. The US economy recovered in part thanks to its domestic shale oil and gas boom, but unlike previous recessions, the US revival to 3%-plus growth rates failed to lead pull other countries out of the doldrums. Europe remained sick and virtually stagnant, China and Asia’s growth considerably slowed and some like Indonesia have ended up in recession.

Oil prices are today over 50% less than last year, interest rates have remained low for a considerable time, labor costs have fallen and commodity prices are down, so one should expect reasonable prospects of sustained economic growth, but some pundits remain pessimistic as developed economies other than the US and the UK show little signs of rapid recovery.

Low oil prices would normally boost economic growth. Why is this not happening? Much of the 50% fall in prices has yet to be passed on to consumers in the developed world, as pump prices have fallen only 10-15% given that the majority of the retail price in many countries is made up of taxes that have not been cut. Consumer confidence has also failed to bounce back, as property prices outside capital cities have been slow to recover, and unemployment for many in Europe remains historically high especially amongst the younger generation.

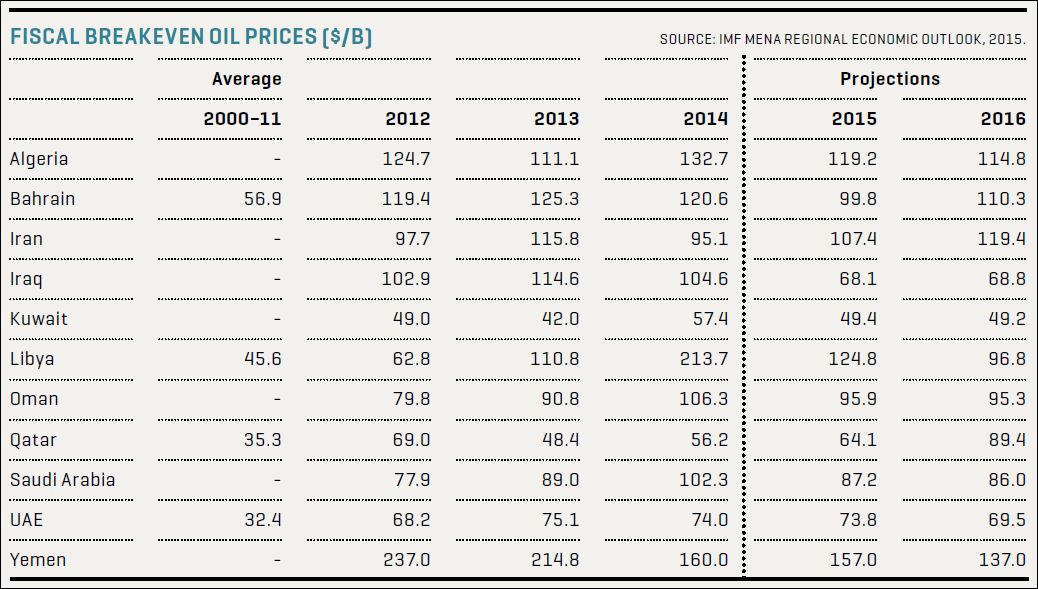

Lower oil prices have weakened the external and fiscal balances of oil exporters, with revenue in 2015 projected to drop by some $300bn compared to 2014. Current account surpluses are likely to disappear and some of the GCC oil exporters are facing fiscal deficits for the first time in two decades. Many will be able to avoid deep cuts in government spending in the short term, as they have substantial fiscal buffers of both sovereign wealth funds and foreign reserves built up over numerous profitable years, and even at $50/B they are still making some profit.

However, other countries like Egypt, Morocco, Tunisia and Algeria have reduced subsidies on fuel and food and introduced other spending cuts in public investment. Iraq faces a growing deficit as oil export revenues fall well short of official budget projections amid a protracted and expensive war with ISIS (see p24). It is worth noting that Iraq’s foreign currency reserve has already declined from $77bn (December 2013) to $67bn (May 2015). The current dilemma for countries like Iraq is how to finance their deficits, in contrast to countries such as the UAE, Kuwait, Qatar and Saudi Arabia, which have the option to either liquidate assets or reduce foreign reserves.

Saudi Arabia, which does not have a sovereign wealth fund but a monetary authority, has seen its foreign assets fall by $60bn, or 8.3%, since end-December 2014 to $664bn by end-June 2015, according to official figures. Kuwait has approved a budget deficit for 2015 of some $27bn and is considering issuing bonds, whilst dipping into its sovereign wealth fund estimated at $548bn. Oman, expecting to increase public expenditure, has approved a budget deficit of $6.47bn for 2015. Bahrain expects a deficit of $3.9bn, equal to 11% of it GDP, and is removing subsidies on fuel, food, electricity, water and meat for its expat community. Even the UAE, which has avoided a deficit, thanks to its policy of economic diversification aimed at reducing dependence on oil revenues, has deregulated transport fuel prices of gasoline and diesel, with effect from 1 August (MEES, 31 July). It is also prudently drafting laws for corporate tax and VAT, just in case it needs to implement them in the near future. Furthermore it has increased indirect taxes in connection with expatriate visas, local government administration, traffic fines etc.

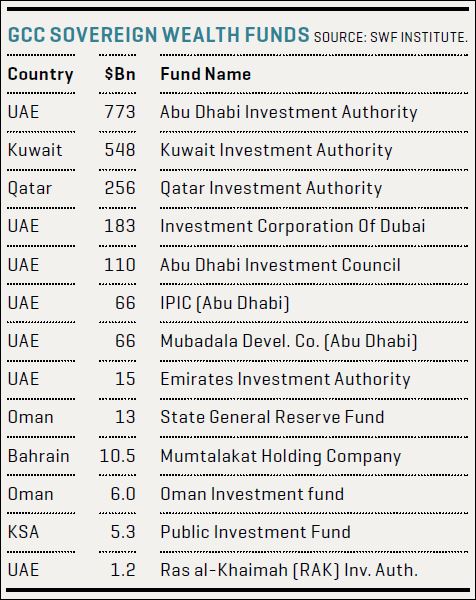

GCC and other Arab sovereign wealth funds have historically invested in US treasury bonds and other European government debt securities, as well as property in the capital cities around the world – especially in London and New York. In recent years there has been an increase in investment by the wealth funds in the private sector, directly or indirectly, via private investment trusts. For instance, Mubadala Development Company (a UAE government company) has placed 90% of its investments in the private sector, as demonstrated by increasing its stake of the Carlyle Group, which is currently the world’s largest private equity investment trust.

However, as low oil prices seem to be here for the next few years, oil revenues may no longer cover the anticipated rise in government spending. So, investment funds are likely to dry up.

Oil-financed sovereign wealth funds are unlikely to grow substantially in the short- to medium-term and one cannot rule out future fire sale of assets to finance budget deficits. Treasury bond markets are likely to see fewer buyers, which might exert pressure to raise interest rates, as bond prices are likely to fall and the commercial and luxury property market may also face a slowdown. Any decline in GCC future spending, will only increase uncertainty and the lack of confidence in many markets.

Does the current period of low oil prices and Iran’s potential entry into the oil market, following the recent P5+1 nuclear deal in Vienna mark the start of a long-term decline in the MENA region’s economic importance? If the agreement with Iran is ratified by the US congress, this will invariably further depress low oil prices, whilst Iran and Arab producing states will compete for regional and global market share. Furthermore, the dramatic increase in US shale oil production since 2010 has reduced US crude imports and increased oil product exports by fivefold to some 5mn b/d. Increases elsewhere in Russia, Africa and the Caspian Sea have added to the supply, in a period when demand has stagnated, due to fuel economy measures and a slowdown in economic growth, particularly in the Far East. Much of recent oil discoveries from Africa and shale oil are sweet oil and thus more marketable than Middle Eastern sour oil. OPEC countries will now have to fight to retain their market share as their only major advantage being their relative low costs of production.

Most of the oil producing states have embarked upon a policy of economic diversification, but the only clear ‘success story’ is the UAE. Faced with low oil prices, rising competition, and little else other than oil to offer the world, these oil-dependent economies may be facing a bleak future if the world economy remains subdued. The emergence of alternative energy sources, many of which are offering a clean alternative to fossil fuels, will only add further to the woes of many MENA economies as the energy mix grows.

The geopolitical nightmare posed by ISIS is far from attractive to foreign investment. Foreign direct investment has been in decline in the region for some time. Only Qatar saw an increase last year mainly because of construction work related to its hosting of the football world cup in 2022. Even the UAE suffered a small dip. Elsewhere the fall has been significant, Saudi Arabia attracted $39.5bn back in 2008 and in 2014 the figure was only $8bn. Last year Kuwait saw a $1bn fall from just $1.5bn, Bahrain suffered a fall of 30% because investors are losing faith with the region, typified by Shell, whose focus is (notwithstanding any lifting of sanctions with Iran) now on Arctic oil, rather than to increase further its investment in the low cost MENA region. Mosque bombings, terror attacks on tourists, the growth of ISIS and al-Qa’ida are all giving the region a high risk factor.

Investors are also put off by existing laws, which are overly bureaucratic, and often impose restrictions on ownership and employment. These restrictions seemingly discourage diversification and the growth of the private sector economy in many countries. Locals seemingly prefer to seek the security of public sector employment rather than face the uncertainties and pressures of the private sector.

Economic reforms, downsizing government employment, privatization and encouragement of the private sector are long overdue in some states. In fact it may be too late for many to address the problem of investor confidence, even in the UAE property prices in recent months have been subdued and have even fallen in some areas of Dubai and Abu Dhabi.

CLOSING WINDOW OF OPPORTUNITY

It seems clear to many outside commentators that the oil-rich Arab world’s window of opportunity is closing; the rise of the energy mix and increased competition on cost and supply of oil and gas is eating into profit margins. Technological development in the near future will bring about further reductions in the cost of energy production, and increased diversity of supply could significantly reduce the currently rich Arab states’ market share in oil and gas. Meanwhile, their populations will continue to grow in the face of ever increasing regional instability and rising unemployment. The World Bank has already forecasted the need for a 100 million job opportunities to be created in the MENA region by 2020, in order to absorb the next baby boomer generation. Job creation seems to be well beyond the ability of most politicians who have often squandered oil riches in creating bloated government bureaucracies awash with corruption and cronyism, or built up reserves rather than build infrastructures that could provide the platform for economic diversification and employment prosperity for their populations.

Are we witnessing the curse of oil dependency, creating the slow death of the region as sovereign wealth funds are being gradually depleted to fund fiscal deficits? Many nations have failed their unemployed younger generation and now will have little to offer the next generation. Regional infighting, corruption, religious intolerance, a growing sectarian divide all usually fuelled by foreign interference and triggered by transnational terrorist groups, will only condemn the region to generations of poverty, unless the situation today becomes a wake-up call for the ruling dynasties to take responsibility and accountability for their own economic development, security and welfare, before all is lost to terrorism and criminality. The UAE has proven that economic security is possible, but few others states in the region have had forward looking politicians as capable as some of the past and present visionary rulers of Abu Dhabi and Dubai.

This article was originally published in the Middle East Economic Survey.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Op-edGulf oil economies must wake up or face decades of decline

August 14, 2015