The student loan program has seen significant changes in recent years, from the rise of student loan debt following the Great Recession, the COVID-19 pandemic payment pause, significant changes to the income driven repayment (IDR) options, and a series of legal challenges. Congress enacted important changes to the student loan program as part of the One Big Beautiful Bill Act (OBBBA), signed into law in July 2025. This collection of reports and events from the Brookings Center for Economic Security and Opportunity illuminates that transformation.

SAVE in the balance: The future of income-driven repayment for federal student loans

Sarah Reber and Sarah Turner

In the last two decades, income-driven repayment options in the Federal Student Loan Program became more generous to borrowers. The wide array of IDR options—and litigation against the SAVE plan—have created significant confusion for borrowers. This report provides an overview of income driven repayment plan policy leading up to major changes passed in the summer of 2025, including the purpose and history of IDR plans, how IDR plans work, and key design trade-offs. The report provides a comprehensive comparison of pre-OBBBA IDR plans.

40%

of federal student loan borrowers, or roughly

12M people

are enrolled in IDR plans, accounting for

$700 billion

in loan balances.

How OBBBA reshapes student lending

Adam Looney, Jordan Matsudaira, and Clare McCann

This report provides a comprehensive summary of the student loan provisions of the OBBBA legislation, signed into law in the summer of 2025. Once it takes effect (many provisions begin in 2028), the law will remake the student loan repayment system, limit borrowing for graduate and professional students, create new institutional accountability rules, and expand eligibility for the Pell Grant to short-term, career-oriented training programs. Details about the implementation of the reforms remain uncertain, including the timeline of migrating the repayment system, especially considering the reduction in staff at the Department of Education.

OBBBA’s reforms may moderate student debt growth and shift repayment risk toward borrowers but are unlikely to impose major short-term macroeconomic shocks...In contrast, OBBBA’s borrowing caps and new repayment rules will affect future borrowing and repayment more gradually over many years.

The past, present, and future of the Public Service Loan Forgiveness (PSLF) program

Sarah Reber and Sarah Turner

Public Service Loan Forgiveness (PSLF) cancels remaining federal student loan debt for borrowers who make 10 years of payments while working full time for a government or nonprofit employer. This report discusses the purpose, origins, evolution, and status of PSLF leading up to the passage of the One Big Beautiful Bill Act (OBBBA) and how the new legislation is likely to reshape the program in the future.

By January of 2026, over

1.2 million

borrowers had received

$90.6 billion

in forgiveness, corresponding to average relief of

$75,000

per borrower.

How much is too much? Loan limits in the federal student loan program

In the fall of 2025, the Brookings Center for Economic Security and Opportunity hosted a panel discussion about the proper role of loan limits, how OBBBA changed those limits, and the potential effects on students and institutions of higher education. Panelists agreed that loan limits are a necessary component to any federal student loan program, but also expressed concerns that the loan limits imposed by OBBBA may limit access to valuable post-secondary education for some potential borrowers.

Watch the full Brookings event here

What went wrong with federal student loans?

Adam Looney and Constatine Yannelis

The number of Americans owing federal student loans and the amount owed has soared over the past few decades. Growth in borrowing has not been uniform across institutions, however. This report shows that debt and borrowing have increased most at riskier institutions and among more vulnerable borrowers. Following student loan reform in the late 1990s, college enrollment increased, particularly among those who had been historically underrepresented. These new borrowers disproportionately enrolled in for-profit institutions and community colleges with a history of higher default rates and low student loan repayment rates.

Today’s student loan crisis—and the fact that it is one of a series—highlights the challenges of using a student loan financial aid system to promote access to educational opportunities that vary enormously (but in opaque ways) in their quality, value, and student outcomes.

Minimum payments in income driven repayment plans

Lesley J. Turner, Zaria Roller, and Sarah Reber

The Repayment Assistance Plan (RAP), the new IDR plan authorized by OBBBA, will require a minimum monthly payment of $10, regardless of income. Under prior plans, borrowers paid nothing if their income was below a “protected income threshold.” This report discusses the pros and cons of minimum payments in IDR.

On the one hand, requiring all borrowers to make at least some payment may encourage connection and engagement with the repayment system and help borrowers new to repayment form good habits around loan repayment. On the other hand, paying even $10 a month can be a real hardship for some borrowers, requiring payments may increase hassle costs for borrowers, and the payment may not even cover the cost of collecting the payment.

The value of a shorter forgiveness timeline for low-balance student loan borrowers

Sarah Reber and Sarah Calame

The Biden-era IDR plan SAVE included a new provision to shorten the time a borrower has to make payments before the remaining balance is forgiven for undergraduate borrowers with small loan balances; such borrowers could have their balances forgiven in as few as 10 years. The SAVE plan was blocked by the courts and will be phased out under the OBBBA legislation passed in the summer of 2025. The newly created RAP plan does not include this provision and increases the time to forgiveness to 30 years. This report discusses the costs and benefits of a provision to shorten the forgiveness timeline for low-balance undergraduate borrowers.

Adding a shortened forgiveness timeline for low-balance borrowers on IDR plans can be a well-targeted, low-cost policy to help ease the burden on student loan borrowers who borrow modest amounts and struggle with repayment, often because they did not complete college.

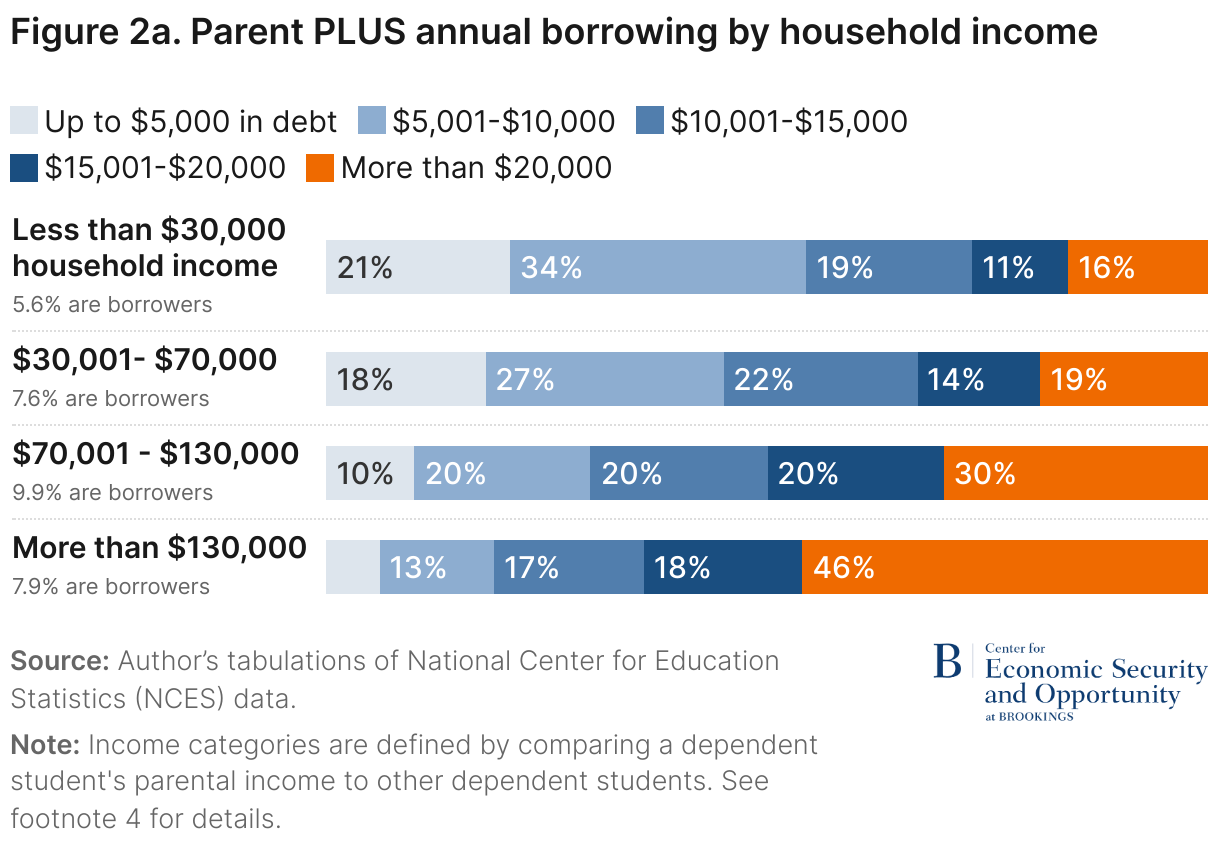

Capping the wrong problem: Why Parent PLUS loan limits may miss the mark

This report analyzes the likely impact of the new, lower limits on how much parents can borrow to finance their children’s education through Parent PLUS loans. The new loan limits are not well-targeted to address real problems with the Parent PLUS program. By focusing on the amount borrowed rather than the capacity of a borrower to repay, the policy will constrain families who could manage larger debts while many low-income parents still borrow more than they can reasonably afford to repay. Families who struggle to repay Parent PLUS loans typically borrow well below the new limits. The OBBBA reform represents a missed opportunity to address the fundamental challenge inherent in the Parent PLUS program that financially vulnerable families are exposed to debt burdens they are unlikely to be able to manage.

OBBBA would extend a student loan tax break that only benefits the best-off borrowers

Adam Looney and Lauren Andrade

This report discusses a student loan provision that allows employees to repay their student loans out of their compensation, free from federal income or payroll taxes. This tax break is costly and ineffective, providing a windfall to high-income workers. Student loan benefits most commonly accrue to the highest paid workers, those who are well-educated, white-collar professionals working for large employers with the sophistication to establish an educational assistance program. This policy is not achieving its intended goal, and well-designed income-based repayment plans would do more to help needy student loan borrowers.

$11 billion

Cost of extending the student loan tax break

over the next ten years.

How are legal challenges to SAVE affecting the student loan program?

Sarah Reber and Sarah Turner

In the summer of 2024, implementation of the Biden administration’s new, more generous IDR plan known as SAVE was blocked by federal courts. The litigation forced the Department of Education to take down the application for all IDR plans several times, so the effects extended beyond the nearly 8 million borrowers who had already enrolled in SAVE. This report discusses the many challenges this legal wrangling has created for millions of borrowers and high cost for taxpayers.

The future of student loan repayment policy

In the spring of 2025, the Brookings Center for Economic Security and Opportunity hosted a lively discussion of the evolution of federal student loan repayment policy. They discussed how policymakers can balance borrower protection, institutional accountability, and fiscal sustainability as the federal government looks to shape the future of student loan repayment plans. The panelists agreed that in the future, at a minimum, federal loan repayment policy should simplify and provide certainty about the process to borrowers.

Watch the full Brookings event here