Summary

The number of Americans insured in the individual health insurance market through exchanges and directly through insurers was at least 13.2 million in the second quarter of 2014 – larger than reported by the government, which only includes the number insured through exchanges – and at least 4.2 million of them would not have been insured in this market had pre-2014 trends continued, but average per-person premiums increased over 24 percent.

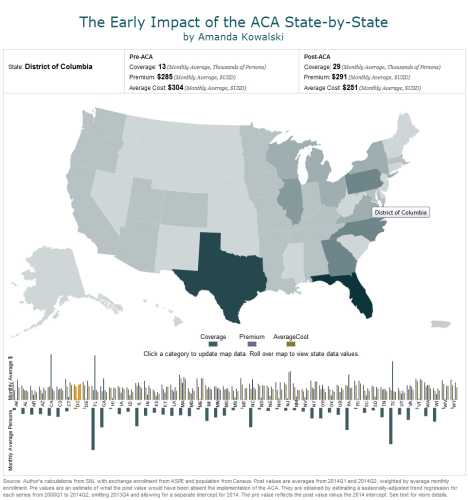

In “The Early Impact of the Affordable Care Act State-by-State,” Brookings nonresident fellow in Economic Studies and Yale University Economics Department faculty member Amanda Kowalski finds that national enrollment trends obscure significant variation across states, as a result of the types of people who opted in and how insurers set premiums. Across all states, from before the fourth quarter of 2013 to the first half of 2014, enrollment-weighted average per-person premiums in the individual health insurance market rose by 24.4% beyond what they would have had they simply followed state-level seasonally-adjusted trends. This large increase stands in contrast to the experience in Massachusetts, which saw premium decreases after its 2006 reform, as documented by Kowalski in previous joint research. Massachusetts also saw decreases in markups (premiums minus costs), which have been rare in other states in 2014.

Kowalski focuses on the individual insurance market using data through the second quarter of 2014 after the open enrollment period ended. She characterizes states into five groups, based on their involvement in the implementation of the ACA. On one extreme were the 5 “direct enforcement” states that ceded all enforcement of the ACA to the federal government (Alabama, Missouri, Oklahoma, Texas, and Wyoming). On the other extreme were 8 states (Colorado, Connecticut, DC, Kentucky, New York, Rhode Island, Vermont, and Washington) that took the implementation of the ACA into their own hands by implementing the Medicaid expansion and setting up their own exchanges. Another group of 5 of these states also set up their own exchanges and expanded Medicaid, but experienced severe technology glitches (Hawaii, Maryland, Minnesota, Nevada, and Oregon), so she examines them as a distinct group. The two groups in the middle of the implementation spectrum include a set of 11 states that adopted the Medicaid expansion but did not set up their own exchanges (Arkansas, Arizona, Delaware, Iowa, Illinois, Michigan, North Dakota, New Hampshire, New Mexico, Ohio, and West Virginia) and a set of 19 “passive” states that did not fit into any of the other four groups (Alaska, Florida, Georgia, Idaho, Indiana, Kansas, Louisiana, Maine, Mississippi, Montana, North Carolina, Nebraska, Pennsylvania, South Carolina, South Dakota, Tennessee, Utah, Virginia, and Wisconsin) – they took some role in implementing the ACA, but did not implement the Medicaid expansion, and they used the federal exchange. All comparisons exclude California and New Jersey because their data are not complete, and they also exclude Massachusetts, because Massachusetts implemented its own reform in 2006.

She finds that individuals in “direct enforcement” states – those states that that ceded all enforcement of the ACA to the federal government (Alabama, Missouri, Oklahoma, Texas, and Wyoming) – are worse off by approximately $245 per participant on an annualized basis, relative to participants in states that were passive implementers of the ACA.

Kowalski also finds, not surprisingly, that the 5 states that had severe glitches with their exchanges (Hawaii, Maryland, Minnesota, Nevada, and Oregon) are worse off than other states with well-functioning state exchanges (Colorado, Connecticut, DC, Kentucky, New York, Rhode Island, Vermont, and Washington), by a large magnitude – approximately $750 per participant on an annualized basis. On the other hand, participants in states that set up well-functioning exchanges were better off than they would have been had their states been passive by approximately $420 per enrollee.

Reviewing data on the 27 states that adopted the Medicaid expansion, she finds that those that expanded were better off than all other states, although the amount is not statistically significant.

Kowalski also divides states based on whether they allowed renewal of non-grandfathered plans in response to the backlash that if people “liked their plan they could keep it” (27 did, but DC and the remaining 23 did not). She finds that participants in states that allowed renewal of non-grandfathered plans are worse off by around $220 annually than participants in other states who did not allow grandfathered non-compliant plans – likely because the people who remained in non-grandfathered plans were healthier than other people in the individual health insurance market.

Using the most recent data collected by the National Association of Insurance Commissioners (NAIC) and compiled by SNL Financial, which includes individual health insurance enrollment outside of the exchanges, Kowalski takes a broader view than the widely-cited report from the U.S. Department of Health and Human Service’s Office of the Assistant Secretary for Planning and Evaluation (ASPE), which reported 8 million exchange enrollees in May. By taking a broader view, Kowalski is able to observe trends in the individual health insurance market from before the exchanges opened for business. Taking these trends into account, at least 4.2 million enrollees are newly-covered in this market (many were likely previously uninsured, but some may have switched from other types of coverage).

Looking at the states individually, she finds that the law benefitted enrollees in at least 13 states (Alaska, Connecticut, DC, Indiana, Kentucky, Maryland, Maine, North Dakota, New Hampshire, Nevada, New York, Rhode Island, and Vermont), with Maine enrollees gaining the most at around $1500 per market participant annually, whereas Oregon (a state with severe glitches on its website and roll-out) experienced the greatest loss – around $850 annually per participant.

She cautions that the paper is based on early data and that “the national experience might evolve over time. Given that the open season for coverage on the exchanges ended at the end of the first quarter, enrollment is unlikely to change dramatically in the short term. However, it might be the case that even though newly-insured individuals paid their premiums in the first half of 2014, they will use their coverage with a lag, resulting in smaller markups as the year progresses. As long as the cost lag does not vary along the same dimension as other state policies (and we have no reason to expect that it will), what we have learned by comparing states with different policies should be more robust than what we have learned in single states. The differential impact of state policies is likely to be stable in the short term, at least until the next open season for coverage and likely until those policies are changed,” she concludes.

Related Content

Related Books

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).