On November 28, Greece finally swapped its so-called private sector involvement (PSI) bonds, which had a face value of 29.6 billion euros (but only 20 billion euros of current secondary market value), with five new bonds. The maturities for these new bonds are spread over 2023-2042 and have variable coupons, ranging from 3.5 percent to 4.2 percent. Reuters cited a government official as saying that, as of November 29, the take up reached 86 percent of bondholders.

The PSI bonds, which had a principal of only 1.5 billion euros, were projected to add illiquidity in the Greek Government Bond (GGB) secondary market. The five new issues (which have maturities of five to 25 years) take the place of the PSI bonds, allowing for a decent yield curve that will facilitate Greece’s goal of returning to the market next August. The August 2018 deadline matters because it is when the third bailout program ends, after which the country has to fund itself by the market.

The swap, publicized since November 15, had the approval from the IMF, the European Stability Mechanism (EMS), and the European Central Bank.

This is a sort of riskless rearrangement of almost 30 billion euros in GGB maturities, seemingly supported by the market. However, as with any exchange, it entails a “buy and a sell side,” with diverse interests. Through all of this, the question remains, is this a necessary action that prepares Greece to exit to the primary markets next August? Before being 100-percent positive, we need some answers.

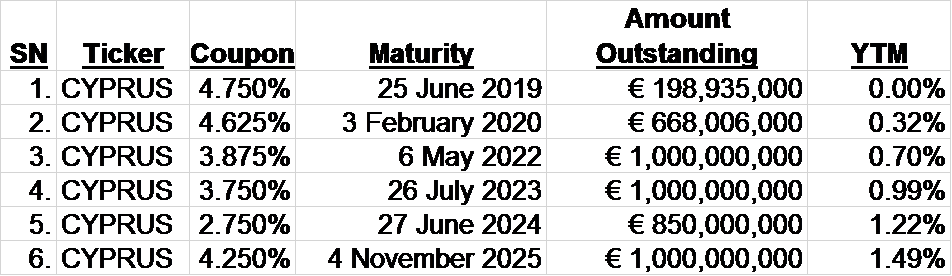

As for the PSI bonds, 1.5 billion euros per issue is quite large and does not seem to impact yields, for example in the case of Cyprus. As detailed below, Cyprus has issuances of less than 1 billion euros each that are non-investment grade, and the European Central Bank is not buying them.

Figure 1: Cyprus’ bonds coupons and maturities

This is because long-term bond investors have appetites for credit and duration and are less concerned with individual issue size. Normal investors have plenty of liquidity if needed. Even the largest positions can be bought and sold over a matter of weeks. Long-term investors are “buy and hold” investors who want stability. The real investors examine economic exposure and duration to calculate public financial management stability. Short-term trading issues are for hedge funds.

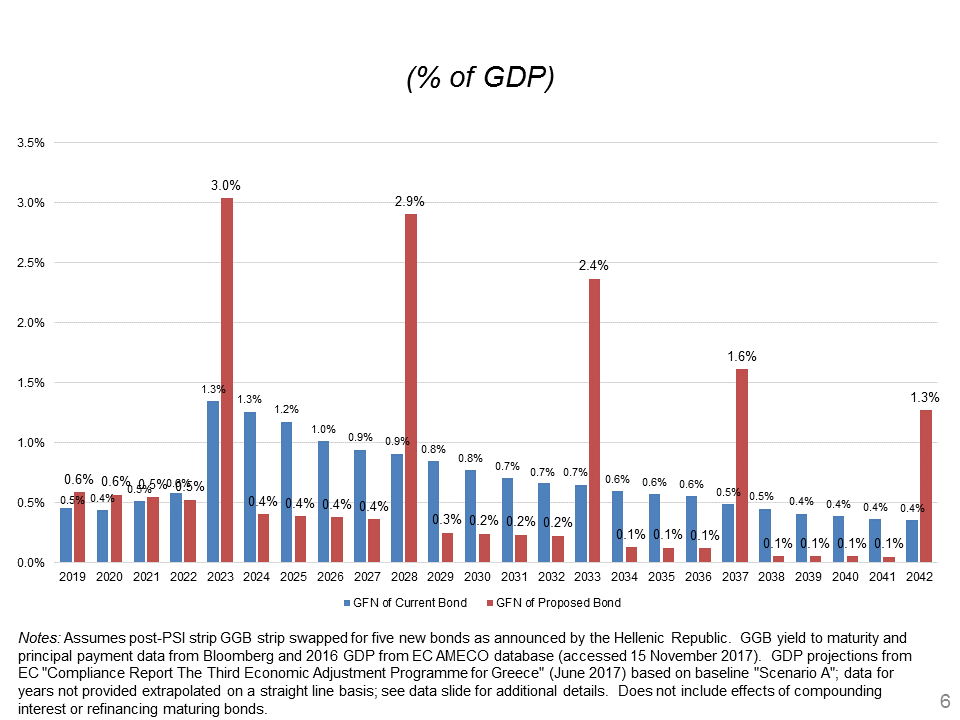

A close look at Gross Financial Needs (GFN) as they pertain to both the current bonds as well as the proposed bonds in relation to Greece’s projected gross domestic product is illuminating.

Figure 2: GGB swap GFN comparison

The swap is supposed to normalize periodically maturities; however, PSI bonds maturities seem to be perfectly smoothed, while proposed maturities entail spikes that increase abruptly in 2027, 2032, 2037, and 2042 by on average 2 percent for each year (see Figure 2 above).

Going from low, smooth annual GFNs to higher gross financing may lead to uncertainty and, potentially, increase financial risk in the future. On the contrary, PSI bonds offered a wider range of maturities periodically. This allowed investors to buy the bond that fits their maturity schedule preference. The swap may exclude investors seeking more year-on-year flexibility.

Estimates state that the exchange is net present value (NPV) positive for the existing bondholders, incentivizing them to offer their PSI bonds to the exchange. NPV gains should be around 1.4 percent for the whole period, larger in the long-end of the PSI maturity period of 2037-2042. But, it is emphasized that the NPV gains is a small buffer only to incentivize investors. As to how the new bonds will be trading after the exchange, it remains to be seen.

So, let’s wait and see whether benefits from the proposed swap will outweigh potential risks during a critical period when the Greek economy needs stability and a speedy recovery.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

To swap or not to swap? Greece issues 5 new bonds

November 30, 2017

Theodore Pelagidis discusses how Greece’s most recent bond swaps could facilitate the country’s goal of returning to the markets next August.