Studies in this week’s Hutchins Roundup find that growing inequality in life expectancy by socioeconomic status reduces the progressivity of retirement benefits in the US, China’s official statistics appear to understate GDP growth, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Widening inequality in life expectancy by socioeconomic status has made retirement benefits less progressive

The gap in life expectancy between Americans in the top 20 percent of lifetime income and the bottom 20 percent has been increasing over time. Alan Auerbach of the University of California, Berkeley, and co-authors find that this growing gap in life expectancy has led to a gap in the present value of benefits received in retirement, including Social Security, Disability Insurance, Supplemental Security Income, Medicare, and Medicaid. They find that, for people born in 1930, the top and bottom income quintiles receive about the same benefits in present value, but for those born in 1960, the top income quintile receives about $130,000 more in benefits than the lowest quintile. They suggest that policymakers should take this growing gap in benefits into account when contemplating entitlement reform.

China’s official published statistics do not overstate its GDP growth

Analysts have long suspected that China’s official statistics overstate its GDP growth. However, using 2004-2013 data on satellite-recorded nighttime light as an independent benchmark of economic activity, Hunter Clark and Maxim Pinkovskiy of the New York Fed and Xavier Sala-i-Martin of Columbia conclude that the official statistics do not overstate growth and might actually understate it. Using the predicted values from their model for more recent years, they conclude that the Chinese economy continued to grow about in line with official statistics in recent years, and find no evidence to support the speculation that it experienced a “hard landing” in late 2015.

Immigrants crowd out employment of natives more in some industries than in others

Using data on US commuting zones from 1980 to 2012, Ariel Burstein of UCLA, Gordon Hanson of UCSD, and Lin Tian and Jonathan Vogel of Columbia find that the effects of immigration on local labor markets are different in tradeable sectors (e.g. manufacturing) than non-tradeable sectors (e. g. housekeeping). In particular, an inflow of labor in tradeable sectors leads to increased production and increased exports to other regions, and has little effect on native workers. In contrast, an influx of immigrants in non-tradeable sectors crowds out employment and lowers wages of native workers.

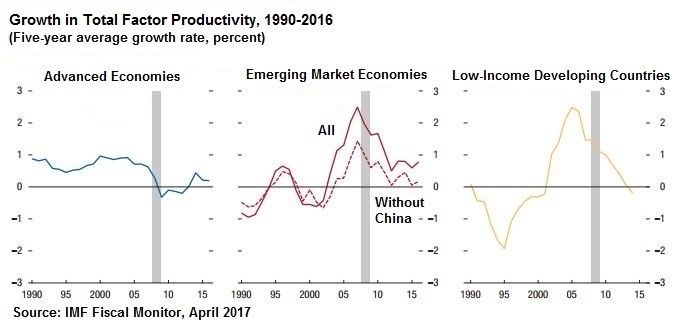

Chart of the week: Growth in total factor productivity, the key driver of improvements in living standards, is falling all around the world

Quote of the week: “Can the Fed be too predictable?” asks Fed’s Vice Chairman Stanley Fischer.

“[I]t is hard to argue that predictability in our reaction to economic data could be anything but positive… clarity about the Fed’s reaction function allows markets to anticipate Fed actions and smoothly adjust along with the path of policy. But there is a circumstance where it might be reasonable to argue that the Fed could be too predictable—in particular, if the path of policy is not appropriately responsive to the incoming economic data and the implications for the economic outlook. Standard monetary policy rules suggest that the policy rate should respond to the level of economic variables such as the output gap and the inflation rate. As unexpected shocks hit the economy, the target level of the federal funds rate should adjust in response to those shocks as the FOMC adjusts the stance of policy to achieve its objectives. Indeed, it is these unexpected economic shocks that give rise to the range of uncertainty around the median federal funds rate projection of FOMC participants, represented through fan charts… The Federal Reserve could be too predictable if this type of fundamental uncertainty about the economy does not show through to uncertainty about the monetary policy path, which could imply that the Federal Reserve was not being sufficiently responsive to incoming data bearing on the economic outlook.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: US life expectancy, China’s GDP growth, and more

Thursday, April 20, 2017