Decline in retirement plan participation most pronounced for low-income and young earners

Using data from the Survey of Consumer Finances between 1989 and 2013, Sebastian Devlin-Foltz, Alice Henriques, and John Sabelhaus of the Federal Reserve Board find that participation in retirement plans increased until 2001, stabilized through 2007 and then declined during the Great Recession and has remained low in recent years. The decline in participation was most pronounced among young and low-income earners; between 1995 and 2013, the participation rate for those in the bottom 50% of the income distribution had fallen by 9 percentage points, but only by 1 percentage point for those in the next 45%, and by 2 percentage points for those in the top 5%.

Accommodative monetary policies increase the risk of future financial crises

Òscar Jordà of the Federal Reserve Bank of San Francisco, Moritz HP. Schularick of the University of Bonn, and Alan M. Taylor of the University of California, Davis, find that, by creating mortgage and housing price booms, looser monetary policies increase the probability of future financial crises. They say this relationship has strengthened since World War II.

Higher tax progressivity leads to lower level of maximum sustainable debt

Hans Holter of University of Oslo, Dirk Krueger of University of Pennsylvania, and Serhiy Stepanchuk of École polytechnique de Lausanne argue that as income tax progressivity rises, the maximum sustainable debt level for a country falls. Specifically, they conclude that if the United States were to adopt Danish-style progressivity (the highest in the OECD), the maximum sustainable debt level would be less than 250% of GDP, compared to 350% if it were to adopt a flat income tax.

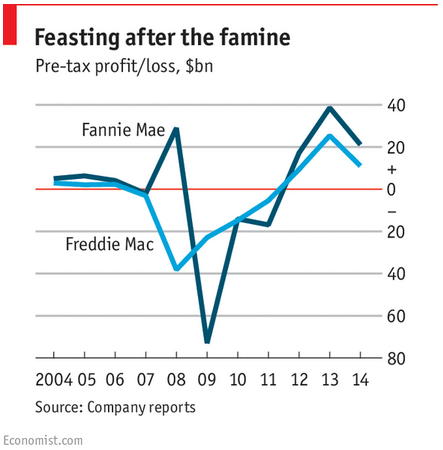

Chart of the week: After a sharp dip in profits in 2014, Fannie Mae and Freddie Mac are more profitable than before the financial crisis.

Quote of the week: Central bankers should set a high bar for interfering in the market

“[F]inancial stability need not seek to eliminate all risks. We need to learn, but not overlearn, the lessons of the crisis. I believe there should be a high bar for “leaning against the credit cycle” in the absence of credible threats to the core or the reemergence of run-prone funding structures. In my view, the Fed and other prudential and market regulators should resist interfering with the role of markets in allocating capital to issuers and risk to investors unless the case for doing so is strong and the available tools can achieve the objective in a targeted manner and with a high degree of confidence.”

–Jerome Powell, Member of the Federal Reserve Board of Governors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Retirement Savings, Monetary Policy and Housing Bubbles, and More

February 26, 2015