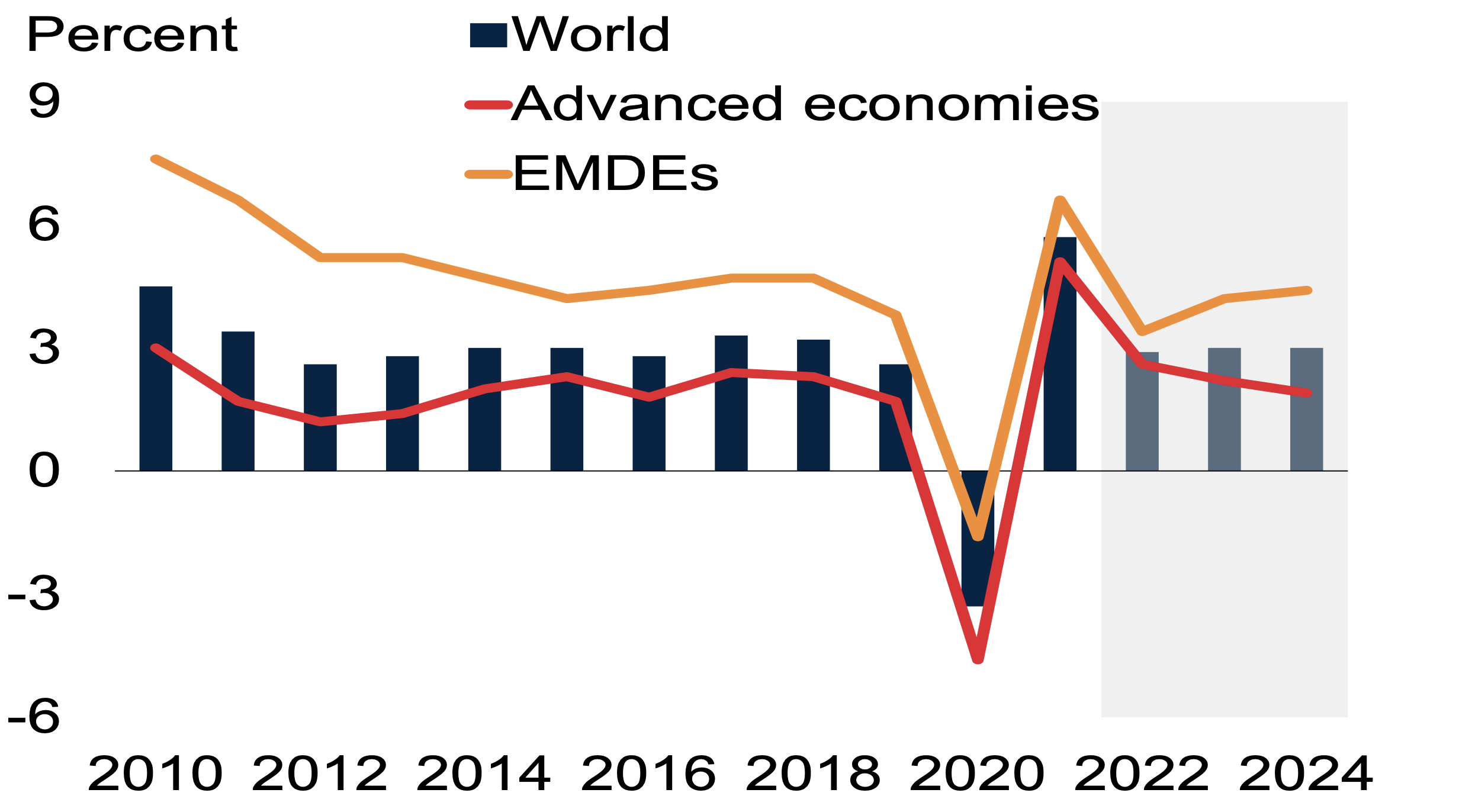

The Russian Federation’s invasion of Ukraine was yet another supply shock to a global economy still reeling from the consequences of the COVID-19 pandemic. According to the June 2022 edition of the Global Economic Prospects report, global growth is projected to slow sharply from 5.7 percent in 2021 to 2.9 percent this year (Figure 1). The effects of the invasion account for most of the 1.2 percentage point downward revision to this year’s global growth forecast. Growth in emerging market and developing economies (EMDEs) is expected to slow from 6.6 percent in 2021 to 3.4 percent in 2022 due to negative spillovers from the war in Ukraine and a deteriorating global environment. Other than the pandemic-induced recession in 2020, this is the weakest year of EMDE growth since 2009.

Arrayed against this baseline of sharply diminishing global growth are various overlapping and mutually reinforcing downside risks, including intensifying geopolitical tensions, rising financial instability, and continuing supply strains. Three of these, which are discussed and quantified in the sub-sections below, may already be materializing. If these shocks materialize at the same time, they could lead to a much sharper global slowdown in 2022-23 than projected in the baseline.

Figure 1. Global growth

Source: World Bank.

Source: World Bank.

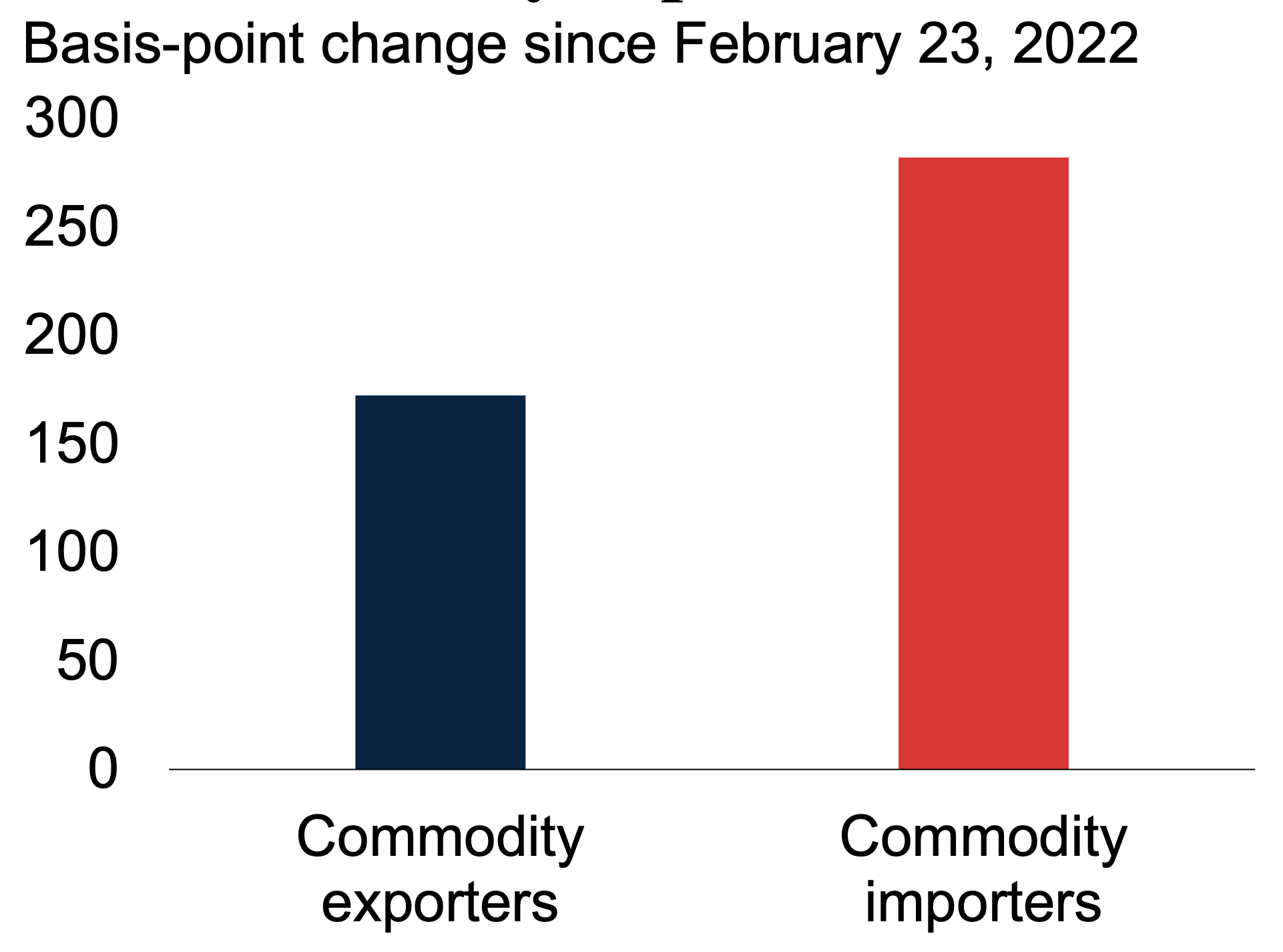

Note: EMDEs = emerging market and developing economies. Bars show cumulative output losses over 2020-24, which are computed as deviations from trend, expressed as a share of GDP in 2019. Output is measured in U.S. dollars at 2010-19 prices and market exchange rates. Trend is assumed to grow at the regression-estimated trend growth rate of 2010-19. EMDE commodity exporters exclude the Russian Federation and Ukraine.

Rising financial stress

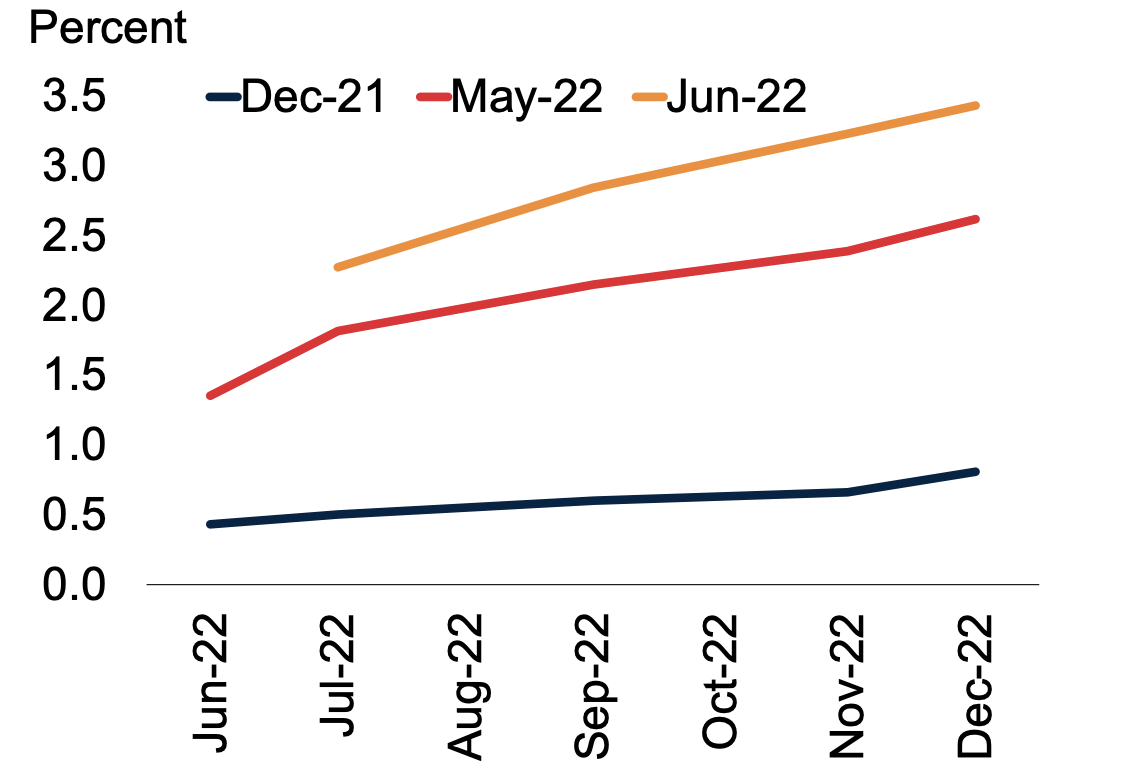

Relentless inflationary pressures have led to chaotic repricing of monetary policy expectations across the world. Prior to June, markets were pricing in an increase in the U.S. Federal Funds rate to 2.5 percent by end-2022. Barely a few short weeks later, in response to another inflation surprise—total CPI inflation reached 8.6 percent year over year in May—end-2022 expectations surged above 3 percent (Figure 2). Similar revisions have beset other major central banks, sending stock markets plunging amid sustained equity volatility. In turn, EMDE financial conditions have reached their tightest level since the start of the pandemic. Sovereign spreads have increased steadily across EMDEs, particularly in commodity importers, where debt service may be increasingly strained (Figure 3).

Figure 2. Market-based expectations of Fed policy rates

Sources Bloomberg; World Bank.

Sources Bloomberg; World Bank.

Note: Figure shows changes in market-based expectations of monetary policy rates over time. “Dec-21” refers to December 21, 2021. “May-22” refers to May 26, 2022, and “Jun-22” refers to June 28, 2022.

Figure 3. Changes in EMDE sovereign spreads by commodity exporter status

Sources: J.P. Morgan; World Bank.

Sources: J.P. Morgan; World Bank.

Note: Figure shows the difference in bond spreads between the latest available data and February 23, 2022 (day prior to the invasion of Ukraine). Last observation is June 24, 2022.

Expectations of faster monetary tightening in the United States could trigger financial stress in EMDEs starting in the third quarter of this year. In this scenario, the Federal Reserve would see no choice but to raise the policy rate to 4 percent by the first quarter of 2023, causing a sharper tightening of EMDE financial conditions. Several major EMDEs would experience large-scale capital outflows and soaring bond spreads, ultimately forcing authorities to accelerate fiscal consolidation efforts. Global growth would be reduced by 0.3 percentage point in 2022 and a further 0.6 percentage point in 2023 compared to current baseline forecasts. EMDEs would be disproportionately affected, with their aggregate growth reduced by 0.5 percentage point in 2022 and 0.9 percentage point in 2023.

Disruptions in energy markets

The war in Ukraine has caused significant supply disruptions and higher price volatility across several commodities, including energy, food, and fertilizers. There are many possible triggers for further upward movements in energy prices. These are all driven by the Russian invasion of Ukraine and could include an immediate ban by Russia on all energy exports to EU members, additional G-7 sanctions targeting shipping companies, and the possibility of secondary sanctions on third parties purchasing Russian energy supplies.

In a scenario of additional major disruptions to energy markets centered around Europe, the prices of natural gas, oil, and coal could spike in the third quarter of 2022 and remain elevated over the remainder of the scenario horizon, reflecting both precautionary buying and lower global supplies. Growth would slow sharply in advanced economies—particularly in the euro area—while EMDEs would face notable headwinds from higher energy prices and weaker foreign demand. On net, global growth could be reduced by 0.5 percentage point in 2022 and a further 0.7 percentage point in 2023.

Recurring lockdowns in China

Economic activity in China is recovering from the deep disruptions caused by strict lockdowns in response to large-scale outbreaks of COVID-19. But the country could experience renewed pandemic disruptions. This possibility of recurring pandemic lockdowns in China is explored in a third risk scenario for global growth. Large-scale COVID-19 resurgences would trigger intermittent lockdowns all the way through 2023, reducing growth in China by 0.5 percentage point in 2022 and a further 0.3 percentage point in 2023. Global spillovers would be modest, unlike in the first two scenarios, but the risks of prolonged disruptions to global supply chains would increase substantially.

Possibility of a sharp global downturn with three shocks

The simultaneous materialization of all three scenarios presented above could reduce global growth to only 2.1 percent in 2022 and 1.5 percent in 2023—0.8 and 1.5 percentage points slower than in the baseline forecast (Figure 4). This would correspond to a sharp global downturn and effectively push the global economy to the brink of recession. The prospects of a dire global economic outcome, so soon after the pandemic global recession, could have devastating consequences for the world’s poor.

Figure 4. Global growth scenarios

Sources: Oxford Economics; World Bank.

Sources: Oxford Economics; World Bank.

Note: Scenario outcomes produced using the Oxford Economics Global Economic Model. Scenarios are linearly additive.

Policies can help!

Even if several downside risks materialize, policymakers may be able to fend off the worst economic outcomes. At a national level, a forceful policy response would require an urgent reprioritization of spending toward targeted relief for vulnerable households, steadfast commitment to credible monetary frameworks, and a general restraint in the use of distortionary policies such as export restrictions and price controls. Once the global economy has stabilized, reversing the damage inflicted by the dual shocks of the pandemic and the war in Ukraine will require an unwavering commitment to growth-enhancing policies, including large-scale investment in education and digital technologies, and the promotion of labor force participation—especially female participation—through active labor market policies.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How sharp will be the global slowdown?

July 1, 2022