In a previous blog, one of us, Martin, argued that China’s rise from poverty to upper-middle-income is consistent with predictions of well-known development models. In this blog, we posit that China’s current development challenges and the policies needed to sustain growth across the threshold to high income and beyond are not very different from those of erstwhile middle-income countries (MICs). This is not to deny the importance of the specific institutional legacies bestowed by China’s long history and, especially, seven decades of communist rule. Yet, China’s recent economic slowdown parallels the experience of other MICs as they approached the high-income threshold. The policies needed to sustain growth consequently echo recipes that have worked elsewhere.

Our conclusion is based on the results of a recent report produced jointly by China’s Development Research Center under the State Council and the World Bank: Innovative China: New Drivers of Growth. Its main findings note China’s growth prospects will depend on three “Ds:” the reduction of market distortions to improve efficiency, the greater diffusion of technological advances throughout China’s vast economy, and the discovery of new products and processes as a result of innovation. In a nutshell, China needs more market competition, investments in advanced skills, and better governance.

Productivity growth has slowed down

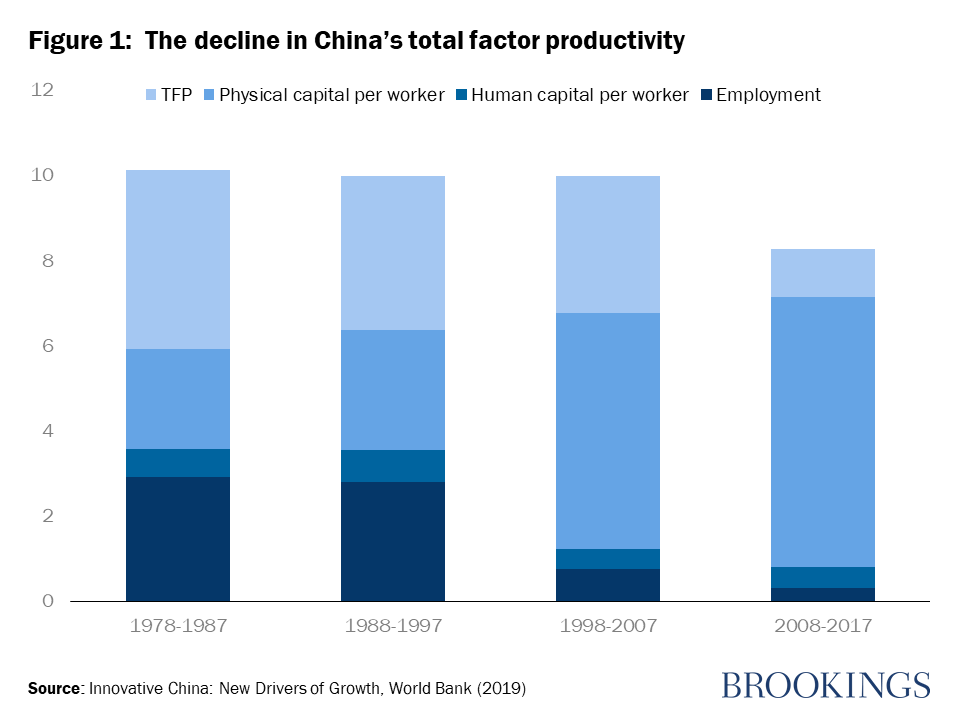

The empirical basis of the argument consists of two parts. First, the contribution of Total Factor Productivity (TFP) to China’s economic growth has fallen markedly since the global financial crisis. TFP growth fell from 3.5 percent in the three decades up to 2008 to just 1.5 percent in the decade since (Figure 1).

Productivity growth has slowed everywhere over this period, but the decline in China is especially large. Moreover, growth has been sustained by a massive investment effort financed largely by Chinese public-owned banks and intermediated mainly by state-owned enterprises. This has led to rising debt and declining returns to investment. At the same time, China’s demographic window of opportunity is closing and labor force growth is projected to start declining over the coming decade. In other words, boosting productivity is the only way to keep China’s growth engine humming.

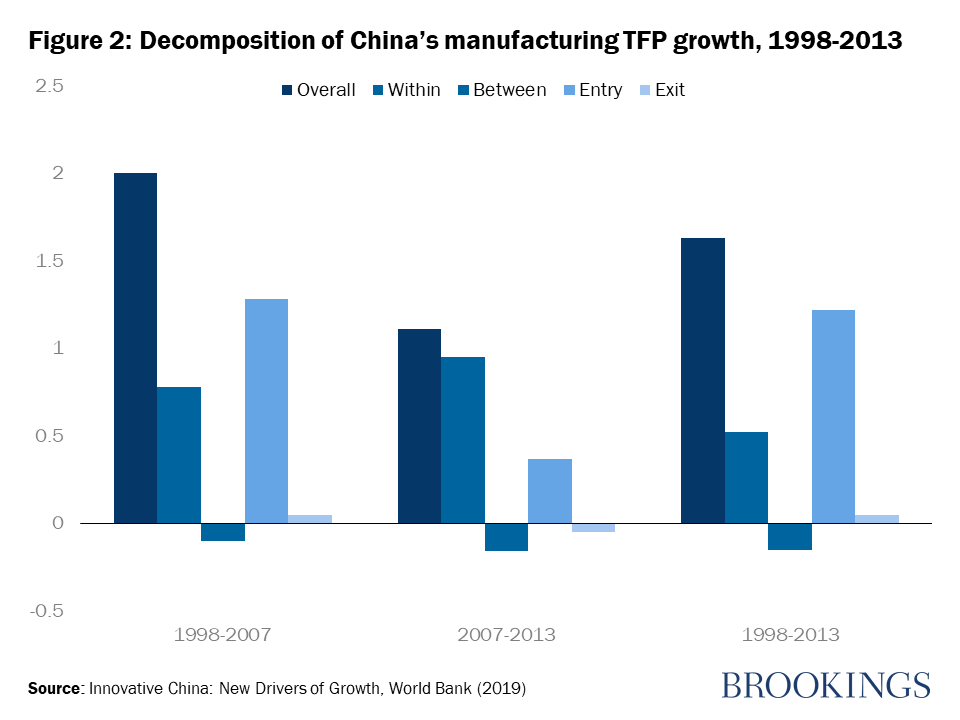

The second part is based on a microeconomic analysis of productivity growth using firm-level data. This demonstrates that over the same period that overall TFP declined, the contribution of structural change to TFP also fell sharply. While within-firm productivity growth rose by 17 basis points to 0.92 percent per year during 2007-13, the contribution of firm entry to overall TFP fell by 0.91 percent (Figure 2). To increase productivity, China will need both higher within-firm productivity growth through innovation, and greater gains from the entry and exit of firms and the reallocation of resources to more productive enterprises driven by greater competition.

These insights are not unfamiliar. From the Soviet Union in the 1980s, Japan in the 1990s, South Korea after the Asian financial crisis, to Brazil and Turkey today, MICs have found that growth through investment alone is not possible beyond a certain level of development. These countries all faced declining returns as the benefits of reallocating surplus labor from agriculture to industry and then from urbanization started to diminish. They also found that the heavy hand of the state in allocating investment resources began to create ever-larger distortions and exacerbated the decline in productivity. Unsurprisingly, the thrust of the report’s recommendations echoes themes that were relevant in former MICs.

Needed: Market Competition, Advanced Skills, and Improved Governance

First, China needs more market competition. The country has engineered advanced technological capacity in a wide range of sectors, often led by the state. At the same time, there is a wide dispersion in productivity levels across firms. Distortions in capital and labor markets, as well as weaknesses in management capacity imply that new technologies are not diffused sufficiently throughout the economy. By reorienting state innovation policy to correct genuine market failures and reform financial markets to grant better access to SMEs, China could achieve substantial productivity gains. China would also benefit from further opening up, particularly in services and cross-border investment. While the extent of China’s technological progress towards the frontier is unique among MICs, the need to strengthen product market competition and reduce factor market distortions to ensure greater diffusion of ideas and technologies is not.

Second, after several decades of huge investment in physical infrastructure, China must now rebalance public spending towards human capital. Large regional and socioeconomic disparities remain in educational attainment. This—combined with the rapid shifts in the demand for skills due to technological change—calls for continued improvement in access to quality education and lifelong learning opportunities. While building a stronger human capital base, China could improve the use of its existing labor force through further reforms of the hukou and pension systems, and measures to improve women’s labor force participation. In the face of rapid aging, these efforts can hardly be overemphasized. China shares this challenge with many MICs; the advantage it has is that it can afford to spend more on social services.

Third, the development of new drivers of growth requires shifts in economic governance. Private sector investment and innovation require stable rules, an even playing field and a recalibration of the roles of the state and the market. While China has introduced many important new policies and regulations over the past five years, their consistent implementation remains a challenge—especially with regard to foreign investment, in the operation of state-owned enterprises, or in adhering to new environmental standards. Local governments that are responsible for the bulk of public spending have emphasized growth and investment over the quality of services and the sustainability of local finances. With growing demands and hardening budget constraints, their emphasis will need to shift. Some of the report’s recommendations about economic governance are specific to China. But the need for the state to evolve from an active player to a coordinator and regulator of private enterprise can be seen in earlier transitions to high income from Eastern Europe to East Asia.

In the coming decade, China will likely cross the threshold into high income. In doing so, it will join a small number of countries that have been successful, while providing both inspiration and insights for others. But China’s progress is not guaranteed. In considering policy adjustments, China would do well to learn the lessons of countries that succeeded in converging quickly towards the world’s wealthiest economies—both on the problems they encountered and the policies they adopted.

Related Books

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

To sustain growth, China can learn from previous transitions to high income

October 18, 2019