In response to the global financial crisis, governments around the world introduced large fiscal stimulus packages. There was much debate about the size and timing of the response. Today, the widely-held view is that the introduction and the intention of a temporary stimulus were appropriate. However, efforts were insufficient to consolidate public finances as the crisis faded. Fiscal deficits have persisted, debt has climbed, and fiscal buffers have been depleted. This experience has taught us valuable lessons; some of these are old forgotten ones. With risks of another crisis looming on the horizon, it is not too late to apply these lessons.

Lesson 1. Counter-cyclical fiscal policy can be an effective tool in crises; its impact is country- and situation-specific.

After the crisis, most economists concluded that the fiscal stimulus was effective and helped support confidence. The impact of fiscal policy is economy- and state-dependent, and especially effective with policy interest rates near the zero bound. Do we have stronger evidence now about the effectiveness of fiscal policy? Only to the extent that policymakers relegated fiscal policy in advanced economies to a seemingly secondary role of helping smooth cyclical fluctuations through automatic stabilizers.

The need to measure the effectiveness of fiscal policy has revived work on fiscal multipliers. The evidence about the size and significance of multipliers is mixed, but they are state-dependent and are larger in recessions than in expansions. The size of the multiplies for the American Recovery and Reinvestment Act (ARRA) is estimated to be about 1.2 after 10 quarters. Estimates for developing countries have a wider range and less precision, but most are well-below unity and lower than those for advanced economies.

Lesson 2. Fiscal policy should be counter-cyclical in both good and bad times.

Debts accumulated during a crisis must be repaid and buffers rebuilt in calm times. Often, spending initiatives started during a crisis become entrenched, thus the so-called “deficit bias” of fiscal policy. Central banks usually remove the punch bowl as the party is in a full swing. Governments, however, find it harder to lock the drinks cabinet when the economy is starting to improve substantially.

Lesson 3. To be effective, fiscal stimulus must be large enough, temporary, and targeted.

In the U.S., the stimulus was smaller than many believed it needed to be because of worries about increasing the size of the government. In the European Union, the stimulus was smaller still because of worries about the market reaction and with fiscal rules limiting the size of the fiscal response.

Many governments did not keep the stimulus temporary. Keeping the spigot of fiscal policy open does not provide a temporary boost to spending, it permanently shifts the stance of fiscal policy. Permanently expansionary fiscal policy does not work; it is unsustainable.

It is often difficult to assess a priori if a shock is temporary or structural. Nonetheless, if economists estimate growth to be below potential year in and year out, it is likely that the potential has changed and estimates of potential growth must be adjusted down. Attempting to return to the stronger growth before the crisis led to more fiscal expansion than warranted, distracting governments from focusing on productivity reforms.

Lesson 4. Fiscal policy alone cannot fix structural problems, and it may exacerbate them.

The underlying causes of the financial crisis were financial imbalances that resulted from regulation out of step with economic developments, limited competition, and inflexible education systems. Fiscal stimulus was an effective tool for preventing a sharper contraction in economic activity. Untargeted and protracted stimulus, however, helped neither the recovery nor productivity. Examples around the world include governments baling out banks by helping oligarch borrowers avoid suffering the consequences or supporting uncompetitive industries to stay afloat. In other cases, the fiscal stimulus provided short-term gain but conflicted with the country’s longer-term goals of rebalancing its growth model.

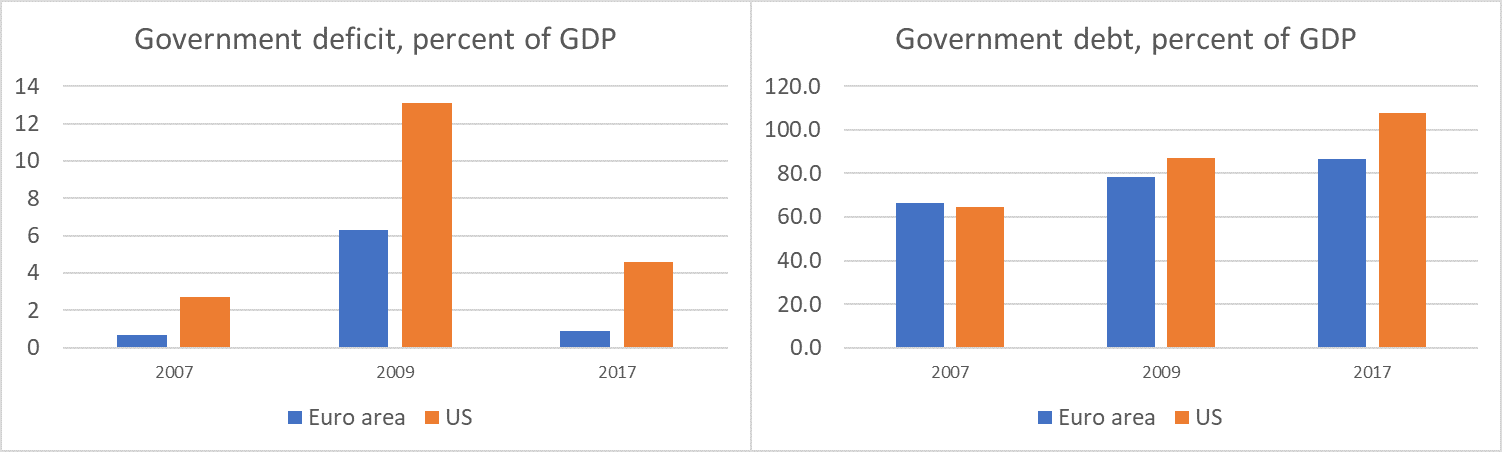

A comparison between the U.S. and EU experience during the crisis helps illustrate some of these lessons. In the U.S., the fiscal stimulus during 2008-2010 amounted to 10 percent of GDP, boosting the fiscal deficit to 13.1 percent by 2009. In the EU, the European Economic Recovery Plan (EERP) called for a fiscal stimulus of about 2 percent of GDP that widened the deficit to only 5.6 percent in 2009. The U.S. has removed the stimulus more slowly than the Euro area, creating fiscal vulnerabilities.

Figure 1: Government deficit versus debt

Many have argued that since the epicenter of the crisis was in the U.S., a much larger package was justified. The more modest EU response was due largely to three factors:

- The unfinished fiscal architecture: The lack of a central public finance authority in the EU left most of the efforts to the member states.

- The EU fiscal rules: Despite the rules, the EU countries had fiscal deficits larger than 3 percent on GDP half the time during the boom of 2001-2007, leaving the EU ill-prepared for the crisis. Government debt in seven of the eurozone countries had government debt above 60 percent of GDP in 2007. Although not conducive to EU’s fiscal health, the rules were not revised before the crisis and, clearly, were neither they enforced.

- The debate between those in favor of stimulus and those in favor of austerity: When countries did not improve their fiscal health before the crisis, there was the concern that market sentiment will force fiscal prudence in the crisis, even though this is bad economics and even worse politics. Many policymakers and economists worried that markets will punish countries with “profligate fiscal policy.” Even then, however, the concern was out of proportions. The EERP included, even during the crisis, consolidation measures equivalent to 1 percent of GDP.

The hope now is that such lessons will be taken to heart so that the world is more prepared for the next crisis, which may not be far away.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

10 years later: 4 fiscal policy lessons from the global financial crisis

June 25, 2018