At the end of each week, one of the rotating editors for Future Development—Shanta Devarajan, Wolfgang Fengler, Indermit Gill, or Homi Kharas—provides recommended literature on a specific development topic.

Last Thursday, at an event sponsored by Duke University’s Sanford School of Public Policy and its program on American Grand Strategy, Nikki Haley, the U.S. ambassador to the United Nations, gave a talk on American leadership in dealing with today’s global challenges. She covered a lot of ground, from Syria, Israel, Iran, to Russia, Ukraine, and North Korea. Judging by the sounds from the crowd during the hour-long session, I’d say she changed many minds.

Toward the end, Ambassador Haley responded briefly to a question about the “trade war” with China. Her main point was that the back-and-forth with China on tariffs is better understood using game theory, not Ricardian rules (she said this a lot more eloquently: Go to 57:00 in the video).

An Overdue ‘China Correction’

In this blog post, I’ll try to convince you that the Trump administration should be given the benefit of doubt about its actions on China. I recommend some readings about the ongoing argument that, taken together, make three simple points:

- The first is that for trade to be fair it has to be free. Since China has displayed no intention to engage in free trade, its current trade strategy is decidedly and deliberately unfair. I think that this is a sentiment shared in most countries that trade with China.

- The second is that almost every country is too weak or too small to call China out on its unfair practices in trade and investment relations. But the U.S. is neither weak nor small, and the Chinese obviously depend more on U.S. markets than Americans do on markets in China. For everyone’s sake, the U.S. should be encouraging—even forcing—China to play by the rules.

- The third is that the cost of China’s unfair trade practices should be measured not just in trade deficits and intellectual property losses, but also in the harm they cause by undermining faith in American-style market capitalism and by making state capitalism look artificially attractive. I’m convinced that market—not state—capitalism is responsible for the impressive rise in living standards in the developing world during last three decades. So what may also be at stake in this spat is the future of global prosperity.

Before I go on, a couple of clarifications. First, no additional tariffs have actually been imposed on China; for now, it’s all talk. Second, the U.S. Trade Representative’s office seems to have done its homework (see, e.g., pages 91-110 of this report) and there are few signs that things are being done in a hurry (see, e.g., this press release on intellectual property theft).

China’s trade practices are neither free nor fair

In a 2016 paper in the Journal of Labor Economics titled “Import Competition and the Great U.S. Employment Sag of the 2000s,” five economists concluded:

“We estimate that import competition from China, which surged after 2000, was a major force behind both recent reductions in U.S. manufacturing employment and weak overall U.S. job growth. Our central estimates suggest job losses from rising Chinese import competition over 1999–2011 in the range of 2.0–2.4 million.”

Losing close to 2.5 million jobs in 12 years is seriously destabilizing even in a big economy if the losses are geographically concentrated. The U.S. Midwest bore the brunt of these losses. But changes in employment patterns should be expected when trade increases. The real question is whether the trade was free and fair.

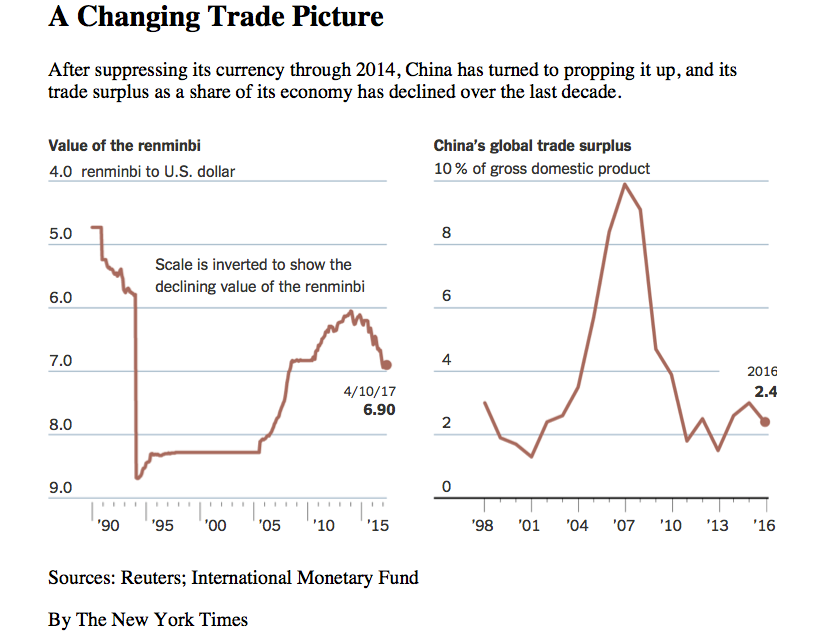

There is considerable evidence that it was not. Figure 1 is from The New York Times indicting that China kept its currency undervalued between 1999 and 2011. Manufacturing workers in the U.S. Midwest whose jobs moved to China would be justified in concluding that the game was rigged. Trade and technology would have led to a steady loss of manufacturing jobs, but the scope and speed of these losses would have been more manageable had the renminbi reflected its fair market value.

Figure 1. A changing trade picture

This raises another question. Since China’s currency is no longer undervalued, isn’t pointing to its trade practices as unfair shutting the stable door after the horse has bolted? The problem is that unfair practices take many forms. This Bloomberg article by Andrew Polk documents another way China is keeping foreign banks out:

“Consider that the four largest banks in the world are all Chinese state-owned institutions. Together they have $11.9 trillion in assets. The world’s next five biggest banks roughly match up to China’s Big Four, accounting for $11.8 trillion, but they represent the largest institutions in four separate countries—Japan, the U.S., the U.K., and France. No single country has financial firepower on China’s scale. Just taking America’s banking sector—where the concept of ‘too big to fail’ originated—it would require the combined balance sheets of the top 10 lenders to equal the assets of just China’s top four…”

Add the growing evidence of the Chinese government muscling foreign firms doing business in China into transferring technology, and state-sponsored efforts to steal cutting-edge technology from firms around the world, and the case against China is even stronger. Martin Feldstein thinks that this may be the real reason for the fight over tariffs.

China has a lot more to lose in a trade war

China is now the world’s leading trader and has the second-largest market. Is the U.S. too late in trying to change the terms of trade? Opinion is divided about this. One side is nicely summarized by Steven Dunaway of the Council on Foreign Relations, the other side by Yale economist Stephen Roach.

Look at the numbers and make up your own mind. U.S. exports of goods and services added up to about $3 trillion in 2016, which is about 15 percent of its GDP. China’s exports are about $2.5 trillion, about 25 percent of its GDP. In 2017, the U.S. ran a goods trade deficit of $375 billion with China and a services trade surplus of about a 10th of that. China’s goods exports to the U.S. were more than half a trillion dollars, about one-fifth of China’s total exports. In comparison, exports to China are less than a tenth of U.S. worldwide exports of goods.

Imports from China into the U.S. are mainly things also produced elsewhere, such as small appliances and apparel. Outside of farm products such as soybean and pork, Chinese imports from the U.S. are more sophisticated and less easily replaced. It’s not hard to figure out who’s more dependent on whom, at least in the goods trade.

Financial relations are more complicated. China has close to $3 trillion in official reserves, and holds a lot of U.S. Treasury bonds. The argument goes that if the Trump administration annoys China, the U.S. might not find buyers of its debt. But these outsized holdings of dollar assets have come from outsized bilateral trade imbalances. If China wants to keep running a trade surplus with the U.S. but not hold dollar-denominated assets, it will have to swap the unwanted dollars for other currencies. That’ll result in appreciation of other currencies such as the euro and the pound, and a depreciation of the dollar. And while a rise in interest rates might hurt the U.S. economy, it will also result in big capital losses for China.

Finally, it is likely that a trade war will result in slowing growth in China. This will undoubtedly destabilize China, a one-party state that relies on steady growth as the principal stabilizer. U.S. politics will become more turbulent, but while democracies are going through a tough patch, they are always more stable than they seem. Besides, while instability will be bad for China’s communist party, it may well be good for the Chinese people. Major reforms in China have generally followed periods of instability.

What’s also at stake is continued global prosperity

The U.S. Trade Representative’s Office has quantified both trade imbalances (about $375 billion annually in the goods trade) and losses due to the theft of intellectual property (about $500 billion each year). What it cannot quantify is the loss in goodwill for U.S.-style capitalism. This might well be in trillions of dollars.

The world has made unprecedented progress in the last three decades: Read this book by Gregg Easterbrook if you aren’t convinced. Poverty in the world has fallen a lot, incomes and living standards have increased, people are living longer and better lives, and health and education standards have improved everywhere. The country most responsible for this is the United States.

America has changed the world in many ways—mass education, the light bulb, the automobile, the airplane, air conditioning, the internet, the smartphone, etc.—simply put, the innovations are astounding. But America’s biggest contribution is perhaps to show that market capitalism can be made to improve the lot of common people. Wherever the American template has been applied, economic progress has quickly followed—be it in Chile or China, in India or Poland.

Standing by as a state-led economy reaps enormous benefits by accessing the world’s largest and most dynamic liberal market economies and then picking apart their individual enterprises isn’t a winning game plan—for the U.S. or for any other market economy. The Trump administration is doing what smaller economies cannot do: Recalibrating the rules of international economic relations.

Globalists everywhere should be openly supporting Trump’s “China correction,” not wishing that he fails.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Future Development Reads: Trusting Trump on trade

April 6, 2018