Unlike in much of the developed world, the promise of manufacturing to spur economic growth and jobs in Africa has remained elusive, with most of the continent’s economies facing deindustrialization. This trend is characterized by declining share of manufacturing in gross domestic product (GDP) and wage employment. All is, however, not lost considering emerging structural shifts, with services and other non-manufacturing industries promising economic transformations. These promising nonmanufacturing industries, termed “industries without smokestacks” (IWOSS), demonstrate key features of manufacturing such as high productivity, agglomeration, and job opportunities. The IWOSS sectors are diverse, cutting across financial services, horticulture, information and communication technology (ICT), tourism, transit trade, and wholesale trade. As part of a broader research project, the Brookings Institution’s Africa Growth Initiative partnered with the Kenya Institute for Public Policy Research and Analysis (KIPPRA) to assess which of these IWOSS might be best poised to unlock jobs in Kenya.

Right now, the country faces significant labor-market challenges in the form of unemployment, time-related underemployment, and inactivity—all of which are more severe for the youth and women. Between 2009 and 2019, the country’s population grew by an average of 2.2 percent annually, but the labor force expanded by an even higher rate of 3.1 percent per annum over the same period, rising from 15.8 million people to 20.7 million people. Unemployment is high: In 2016, the overall unemployment rate of the working-age group (15 to 64 years) was estimated at 7.4 percent, that of women was 9.6 percent, and that of the youth (15 to 24 years) was 17.7 percent. Time-related underemployment was estimated at 20.4 percent for the working-age population, and 26 percent and 35.9 percent for the women and youth, respectively. In addition, despite Kenya’s long prioritization of industrialization as an avenue for mass employment creation and economic growth, the manufacturing sector contribution to GDP has declined from 11.3 percent in 2010 to 7.5 percent in 2019. The formal sector wage employment contribution of manufacturing has also remained stagnant, averaging 13.0 percent over the last two decades.

Can support to horticulture, ICT, and tourism help address Kenya’s youth unemployment problem?

To examine the potential of IWOSS more closely, the KIPPRA team chose three IWOSS with strong sectoral growth performance, contribution to GDP, and strong export performance—horticulture, ICT, and tourism—and found that all three sectors demonstrate above-average output growth and projected that they can be significant sources of wage employment for youth up to the year 2030. At the aggregate level across all IWOSS, labor-output productivity is twice that of manufacturing and 1.7 times that of other non-IWOSS. Except for construction, the industrial sectors performed below average with respect to output growth over the two decades up to 2018.

Within IWOSS, we also found that ICT, tourism, and trade have the highest potential for wage-employment growth resulting from respective GDP growth of these sectors (Table 1). However, horticulture is characterized by nonwage employment in the form of family labor.

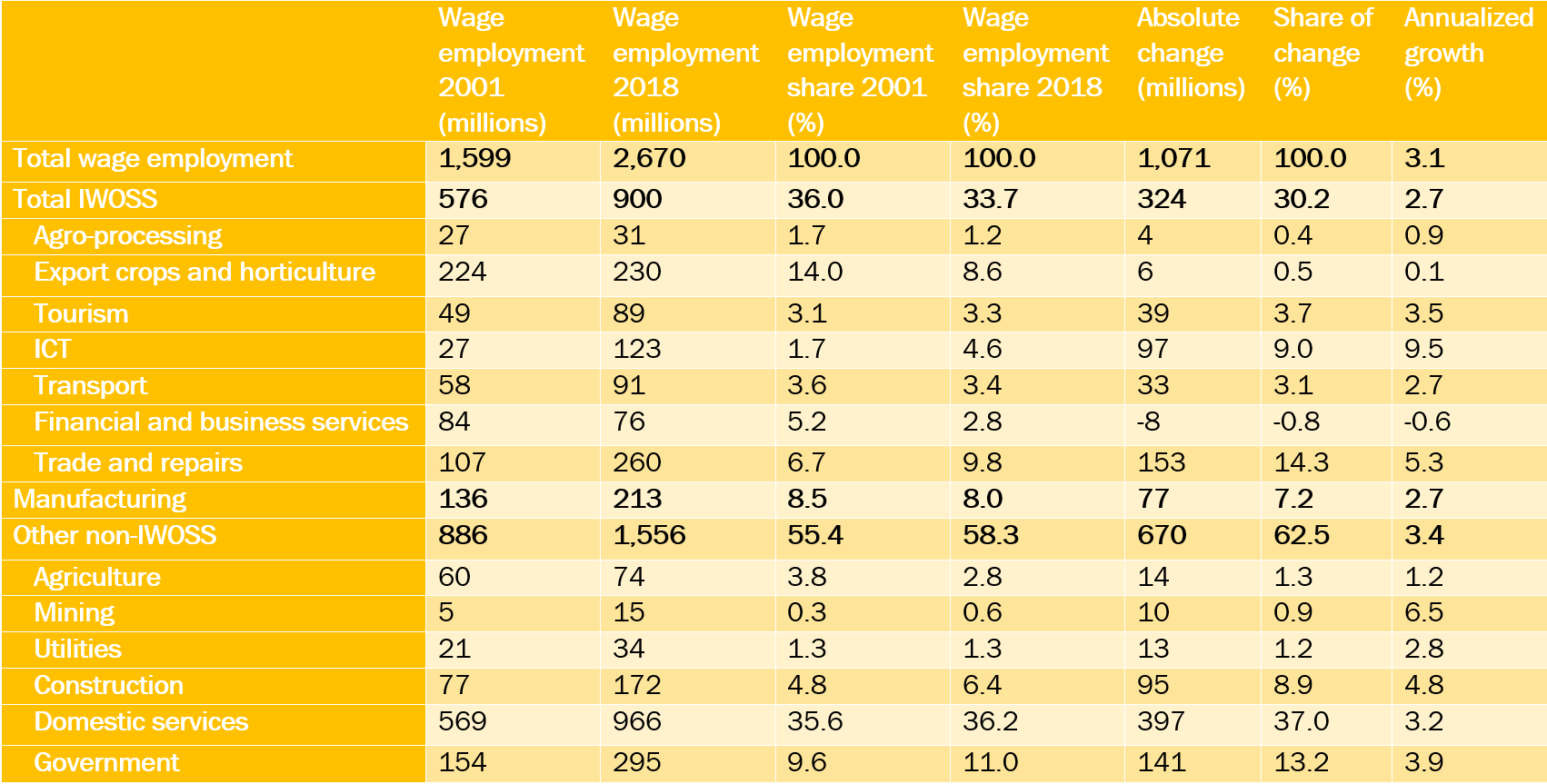

Table 1. Changes in formal employment and its share in IWOSS and non-IWOSS, 2001-2018

Note: Manufacturing excludes agro-processing.

Source: Authors’ calculations based on data from KNBS (Various), Statistical Abstract.

The projections to the year 2030 reveal that there will be wider sex disparities in wage employment if the prevailing growth trends persist and no policy interventions are put in place. Male youth (15 to 24 years) will dominate manufacturing, construction, and trade, with their respective numbers projected to be 1.5, 13.8, and 1.2 times higher than females. In ICT, there will be 3 times more males than females if present growth trends persist. The projections also reveal that there will be more females in horticulture (1.3 times more) and tourism (1.1 times more) relative to males.

Constraints to growth for horticulture, ICT, and tourism

Importantly, for these sectors to meet—or even surpass—their job-creation potential, a number of constraints must be addressed. The study identified both crosscutting and sector-specific constraints affecting the output and employment growth of the three IWOSS sectors. The crosscutting constraints relate to investment climate, which encompasses infrastructure, the business and regulatory environment, and skills gaps.

Infrastructure

The high cost of electricity and the lack of a reliable power supply to firms pose challenges not only across firms in the IWOSS sectors but also across the entire economy as these obstacles hurt firm-level competitiveness and deter investment. The cost of road and railway transport in Kenya is generally higher than in its comparator set of countries. Not only that, but many firms are grappling with poor infrastructure of feeder roads, which leads to large post-harvest losses in the horticultural sector estimated at 42 percent. While Kenya’s ICT infrastructure is among the best in Africa, the relatively high cost of mobile broadband services and the large digital divide between urban and rural areas still hinder the sector’s expansion. These constraints are related to weak competition in Kenya’s ICT sector. Importantly, there is limited (but increasing) interoperability between mobile-payment operators, which affects the ability of smaller players to grow, thus potentially creating an inefficient market with one or a few large players.

Business and regulatory environment

While Kenya was ranked third in Africa in the 2020 World Bank Doing Business Report on account of ease of getting credit and to some extent getting connected to electricity, the regulatory business environment remains complex, especially with regard to starting a business, cross-border trade, and getting construction permits. These constraints hamper the country’s ability to improve its competitiveness, attract investments, and create more jobs and improvements, and will require deeper and broader reforms.

Persistent skills gaps

Skills gaps and mismatches resulting from low educational attainment levels relative to a typical middle-income country also persist in Kenya. About 43 percent of the working-age population have only a primary education (of eight years) as their highest education level, yet the IWOSS sectors heavily depend on post-primary level skills. Further, education quality is characterized by inadequate skills and gaps in required skills even among tertiary graduates.

Skills gap analyses across the three IWOSS sectors reveal that horticulture has skills deficits for occupations requiring post-primary education and skills surpluses for occupations that require at least some secondary education. Tourism has skills deficits for all skill levels, particularly those related to external communications, product quality, value packaging, and quality management.

While over the last decade IWOSS sectors such as horticulture had relatively strong export performance relative to aggregate exports, there are still significant cross-border constraints related to inadequate skills among customs officials, lack of an integrated quality system, limited coordination among exporters, insufficient systems to handle food-safety compliance, and inadequate capacity to trace horticultural commodities. Further, ICT faces additional challenges related to a weak framework to identify and nurture innovations.

Policy recommendations

The relatively high productivity across IWOSS sectors presents a case for policy support to enhance growth and employment opportunities. However, IWOSS are not currently meeting their potential, and a number of policy changes are necessary to help them grow and absorb labor. Thus, the government and other stakeholders should:

- Enhance investments in infrastructure including trunk roads as well as feeder roads and a host of supportive facilities such as cold rooms for horticulture produce.

- Address regulatory bottlenecks through a continuous process of monitoring and evaluation as well as by conducting regulatory impact assessments. For example, an improved policy and regulatory framework on net-metering and wheeling systems would enhance entrants into alternative sources of energy and off-grid systems. Better regulations would also open up markets for more players and hence enhance the role of ICT as an enabler.

- Expand the creation of wage jobs rather than informal jobs in the growing sectors. Reducing barriers to formalization linked to complex regulations, high taxes, and other aspects of cumbersome investment climate is essential.

- Focus education and training systems to produce skills demanded by the market compared to academic credentials. This can be achieved by strengthening partnerships for skills development and enhancing programs that combine on-the-job and in-class training.

- Monitor and forecast skills needs to ensure the youth are equipped for available jobs, and then develop skills of the youth to meet the increasing demand for more educational qualifications. Skills development should take into account basic skills and social skills needed in specific sectors.

For horticulture, the following are the priority interventions:

- Ameliorate the possible effects of the dynamic nontariff trade barriers (NTTBs) by supporting continuous skills transfer and extension services support to local producers, including small-scale farmers.

- Enhance further investments in supportive infrastructure—the feeder roads and cold chain infrastructure such as “cold” collection centers and pack houses.

- Open up more options for transport—especially maritime transport of exports—by investing in a dedicated maritime line to key export destinations.

- Mold the preference of youth toward agricultural training to attract more youth to higher productivity jobs within the sector.

For ICT, a key intervention would be to put in place a policy framework that enhances competitive markets to improve affordability/access to services by the last-mile users. Fast-tracking an all-encompassing policy for e-commerce will open up further investments in the sector. On skills and capacity development, there is a need to promote private-sector-led, skills-development initiatives in high-level ICT skills such as programming. In ICT, best-practice models can be adopted by Kenya to enhance the benefits of ICT services. These include:

- Encourage sharing of communication infrastructure (e.g., masts) by encouraging cross-sector consultations for infrastructure developments.

- Create planning databases containing detailed information of infrastructure available for sharing.

- Enhance interoperability through moral suasion.

For tourism, policies for supporting growth in the sector include:

- Enhance access to reliable electricity and transport infrastructure to reduce operational costs and enhance competitiveness.

- Reform the regulatory and tax regime, with a focus on eliminating multiple taxation and clarifying the unclear tax regime.

- Promote the development of specialized training institutions for crucial high-level and diverse skills. Examples of these skills are film production, decisionmaking and problem-solving, food technology, information technology, and leadership.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Unlocking constraints to industries without smokestacks to catalyze job creation for youth in Kenya

July 29, 2021