Last week, the office of the chief economist for the Africa Region of the World Bank released its biannual publication, Africa’s Pulse. Each edition of Africa’s Pulse analyzes issues that present developmental challenges for the continent. This edition presents the challenges brought about by Africa’s debt burden and poor electricity access. The report also gives an update on the continent’s macroeconomic environment and predicts that GDP growth will improve after the commodity price crash. The report forecasts a GDP growth rate of 3.1 percent in 2018, eventually reaching a 3.6 percent average between 2019 and 2020. The figures below present a depiction of Africa’s current debt structure.

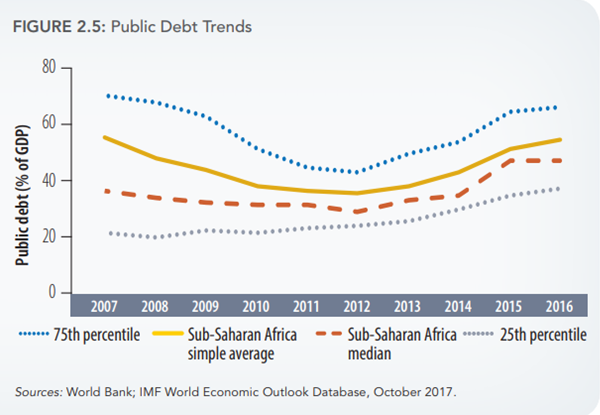

Figure 2.5 shows the trends in sub-Saharan Africa’s public debt in the past 10 years. Africa’s debt-to-GDP ratio had been trending downward until it picked up in 2012, with an increase from 37 to 56 percent of GDP between 2012 and 2016. The report adds that one-third of African countries saw a 20 percentage point increase in their debt-to-GDP ratio. Moreover, the composition of the debt has shifted as countries have moved away from concessional sources of financing toward market-based domestic debt. It is important to note that the average lies above the median, signaling that a few African countries (notably oil exporters) are responsible for the relatively high debt-to-GDP levels.

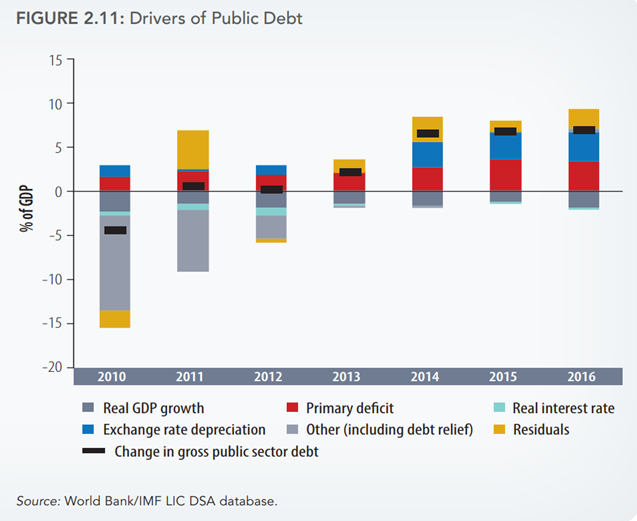

Figure 2.11 identifies the drivers of public debt. Exchange rate depreciation, residuals, and the primary deficit have been the key drivers of public debt in sub-Saharan Africa. The exchange rate depreciation has been in commodity-exporting countries, whose currencies depreciated as commodity prices fell. The primary deficit—the difference between government spending and revenue—can be partly explained by the challenges Africa faces in mobilizing domestic resources and strengthening its tax base. The figure also shows a noticeable decline in the “other” category, which is a debt alleviator, not a driver. The category includes debt relief, which many African countries stopped benefiting from as they graduated out of the Heavily Indebted Poor Countries (HIPC) program, an initiative created in 1996 by the World Bank and the IMF with the aim of ensuring that poor countries do not face debt burdens they cannot support.

While debt on the continent has increased in recent years, African countries have received less debt relief. The last country to receive debt relief under HIPC was Chad in 2015. Presently only three (out of the original 39, which included non-African countries such as Afghanistan) HIPC countries remain: Somalia, Sudan, and Eritrea. While African countries have been accumulating debt at a faster rate, graduation from the HIPC initiative indicates that they are increasingly able to sustain their debt. Today, there is a ravenous appetite by high-risk, yield-seeking international investors for Africa’s debt, given relatively higher returns: The African average lies at 6 percent against 5.5 percent in emerging nations and 4 percent in developing economies in the Asia-Pacific region. Last month, Senegal received nearly $10 billion of orders for a $2.2 billion eurobond. The report suggest that avoiding debt distress will depend on three key factors: reducing fiscal imbalances, maintaining strong economic growth, and managing public debt in an efficient manner.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figures of the week: Africa’s changing debt structure

April 26, 2018