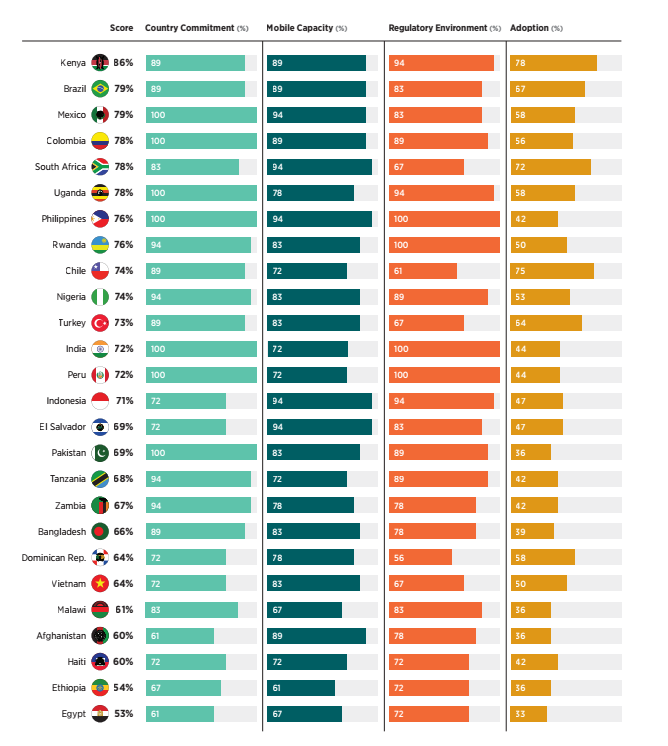

The Financial and Digital Inclusion Project at Brookings recently released its 2017 report focusing on access and usage of financial services in 26 developing countries across Asia, Africa, Middle East, and Latin America. The report, like its past two editions, grades countries on mobile capacity, regulatory environment, adoption of financial services, and country commitment to furthering financial inclusion. Kenya topped the list for a third year running, this result driven largely by its high adoption rates and wide variety of mobile money services, as well as its enabling regulatory environment. According to the report, for the first time all the countries covered are part of a financial inclusion-oriented organization or network. Countries in sub-Saharan Africa hold two spots in the top and bottom five of the aggregate index highlighting the disparities in mobile adoption and financial inclusion within the continent, as seen in Figure 1.

Figure 1. Overall rankings in the Brookings 2017 Financial and Digital Inclusion Project

The report also provides country-level analysis and grading for the various measures for all countries under study. Below is a brief look at what Malawi and Nigeria have done to boost financial inclusion.

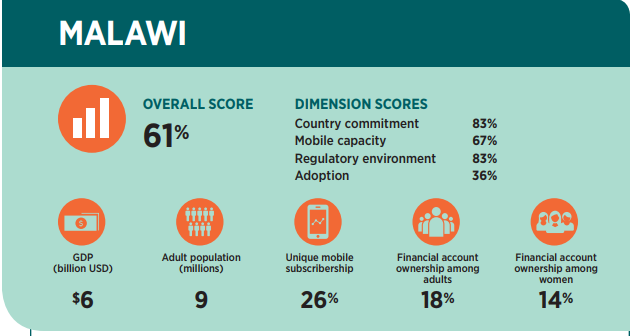

Malawi

Malawi has taken a number of concrete steps to improve financial access such as setting measurable financial inclusion goals and joining both the Maya Declaration and the Better Than Cash alliance in recent years. This progress on the regulatory and public policy side is reflected in its relatively high scores on country commitment and regulatory framework. Some of the key next steps identified for Malawi in the report include monitoring progress in achieving its inclusion goals, sharing best practices from recently implemented programs, and amplifying coordination of financial literacy initiatives to drive adoption.

Figure 2. Malawi snapshot

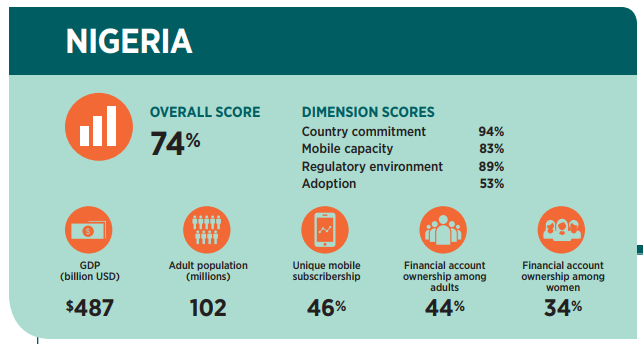

Nigeria

Between 2016 and 2017, Nigeria increased its score for mobile capacity and regulatory environment by 5 and 6 percentage points respectively, while its country commitment and adoption scores remained stagnant. The low adoption rates for mobile money services pose a challenge to its financial inclusion goals and the Central Bank of Nigeria has taken steps by launching a national cashless policy and developing a financial education curriculum to be launched soon, according to the report. In addition, the Nigerian postal service partnered with Paga to use its post office branches as financial service access points in May 2017.

Figure 3. Nigeria snapshot

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figures of the week: New findings in African financial and digital inclusion

September 8, 2017