Nigeria plans to raise 105 billion naira ($345 million) in naira-denominated bonds at auction next week as it seeks to bolster its finances by 250-340 billion naira in the fourth quarter of 2016 to fund a historic 2.2 trillion naira deficit. The bonds will be sold in three tranches of 35 billion naira each, maturing in five, 10, and 20 years respectively. The government is aiming to raise 900 billion naira from local debt markets by the end of the year.

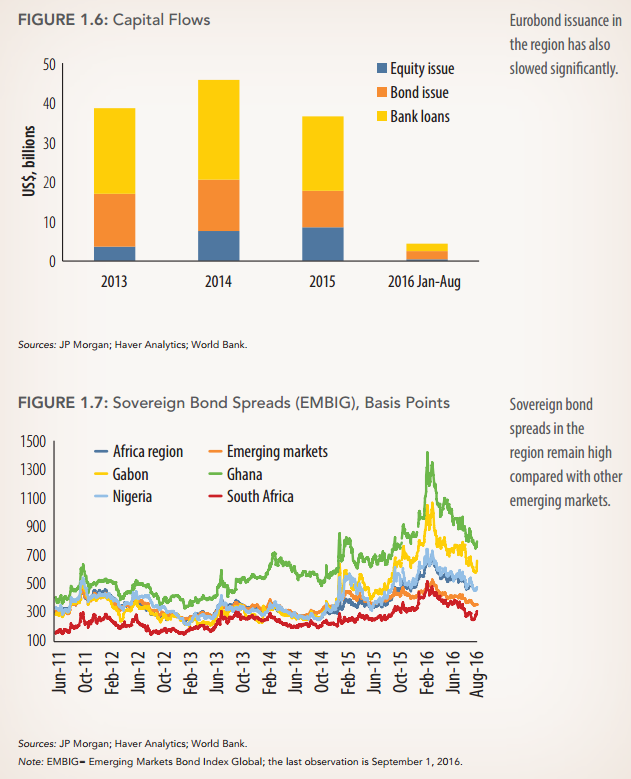

Nigerian Finance Minister Kemi Adeosun is currently on a roadshow across Europe and the United States to sell Nigerian bonds. Adeosun announced to bond investors in June that Nigeria was close to securing $3 billion from the World Bank and the African Development Bank. The Ministry of Finance has also just finalized plans to hold a $1 billion eurobond issuance next month. Despite the fact that foreign-currency bond sales, including eurobond issuances, have slowed throughout the continent in 2016 (see figures below)—due to U.S. policy tightening and concerns of higher borrowing costs—Nigeria still plans to tap into the eurobond market. The government is expected to raise about $5 billion from eurobond issuances, as well as multilateral and bilateral lenders over the next two years.

Source: World Bank, Africa’s Pulse.

Nigeria has turned to the international debt markets to fund President Muhammadu Buhari’s ambitious 6.1 trillion naira ($19.4 billion) plan to reinvigorate Nigeria’s slumping economy. The majority of the funds will be put towards capital expenditure, most particularly infrastructure investments. Last week, in his Medium-Term Expenditure Framework, he proposed a record 6.9 trillion naira in capital expenditure in 2017, an increase of 800 billion naira compared to the 2016 plan.

The Nigerian economy is in its deepest recession in decades following historically low oil prices. Meanwhile, foreign direct investment fell by 37 percent year on year while total capital inflows were down 75.7 percent, according to Nigeria’s National Bureau of Statistics. Boko Haram’s insurgency in the north and the insurgencies in the oil-rich Niger Delta region further contributed to the country’s woes. Subsequently, the Nigerian economy contracted 0.4 percent year-on-year in the first quarter and 2.06 percent in the second.

Due to the recession, international ratings agencies have downgraded Nigeria’s sovereign credit rating further. Moody’s downgraded Nigeria’s rating from BA3 (BB-) to B1 (B+). A BA3 rating is five levels below investment grade status. Both Standard and Poor’s and Fitch have also downwardly revised their ratings to B and BB+ respectively this year.

While investors may be unnerved by the stark warnings issued by the credit agencies, Nigeria’s Debt Management Office is confident that Nigeria will be able to service its debt. Nigeria enjoys relatively low debt-to-GDP ratio for the continent at 13 percent, and interest payments have also been low. More encouragingly, a recent agreement signed in Algiers by the Organization of Petroleum Exporting Countries last week seeks to slash 1 to 2 percent of the cartel’s 33.2 million barrels per day of production, the first time OPEC has limited output since 2008. As a response to the news, oil prices surged; U.S. crude broke $50 a barrel for the first time in months.

Junaid Belo-Osagie contributed to this post.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figure of the week: Nigerian bond auction aims to finance record budget

October 7, 2016