Since the publication of this blog, several government agencies have announced program extensions to promote housing stability and to prevent foreclosures. The CDC extended its eviction moratorium for a final month until July 31, 2021. The Biden-Harris Administration also extended the foreclosure moratorium for federally-backed mortgages by a final month, until July 31, 2021. HUD, VA, and USDA announced extensions to their COVID-19 forbearance programs for eligible homeowners. These programs were set to expire June 30, 2021, but will continue to accept new applications through September 30, 2021. Finally, COVID-impacted homeowners with mortgages backed by Fannie Mae and Freddie Mac will continue to be eligible for COVID-related forbearance.

Widespread vaccinations and relaxed CDC restrictions have stimulated a robust economic rebound. Since the start of the pandemic, the U.S. unemployment rate declined dramatically from a peak of 14.8% to roughly 5.8% at the time of this writing. Employers have added roughly 14.7 million jobs. Still, 9.3 million workers remain suspended in a state of joblessness and financial fragility, including low-to moderate-income-class families worried about preserving their homes.

For homeowners facing COVID-related hardships, the CARES Act’s mortgage forbearance protection has been a crucial lifeline: an unprecedented payment deferral program allowing struggling borrowers to delay or reduce their mortgage payments, creating an essential safe harbor that temporarily secured their claim to the American Dream. According to the Federal Reserve Bank of New York, forbearance plans disproportionately benefitted low-income borrowers, especially those holding FHA-insured loans or living in disadvantaged neighborhoods.

Despite evidence that many low-income borrowers remain in distress, this crucial policy shield will disappear on June 30 when the federal forbearance program is set to expire. This development has serious implications for the roughly 2.1 million borrowers still under the protective ambit of COVID forbearance programs. On the surface, steady increases in forbearance exits suggest that borrowers’ financial circumstances have improved. These national trends, however, mask significant financial weaknesses plaguing financially stressed households, and financial stress tends to be geographically and demographically concentrated among communities of color. The looming forbearance cliff threatens to expose millions of unemployed and underemployed homeowners to foreclosure, bankruptcy, or pressure to sell prematurely. These escape routes will undoubtedly exacerbate the racial wealth gap; each option represents a retreat from homeownership that communities of color are ill-prepared to absorb. Homeownership is integral to generational wealth creation, home equity is the largest component of asset-driven wealth for Black and Hispanic accounting for nearly 40% of their balance sheet on average

Policies aimed at stabilizing distressed communities should be informed by the well-being of COVID-impacted homeowners, not artificial deadlines. We partnered with SaverLife, a fintech non-profit, to explore the financial well-being of low- and moderate-income homeowners. Like Tenesha, who lives in Washington with two daughters. She has never missed a mortgage payment but worries about losing her home when her unemployment benefits end. This blog highlights the financial constraints and foreclosure fears among distressed borrowers and offers pointed recommendations to preserve their homes.

Upended households struggle to regain their footing

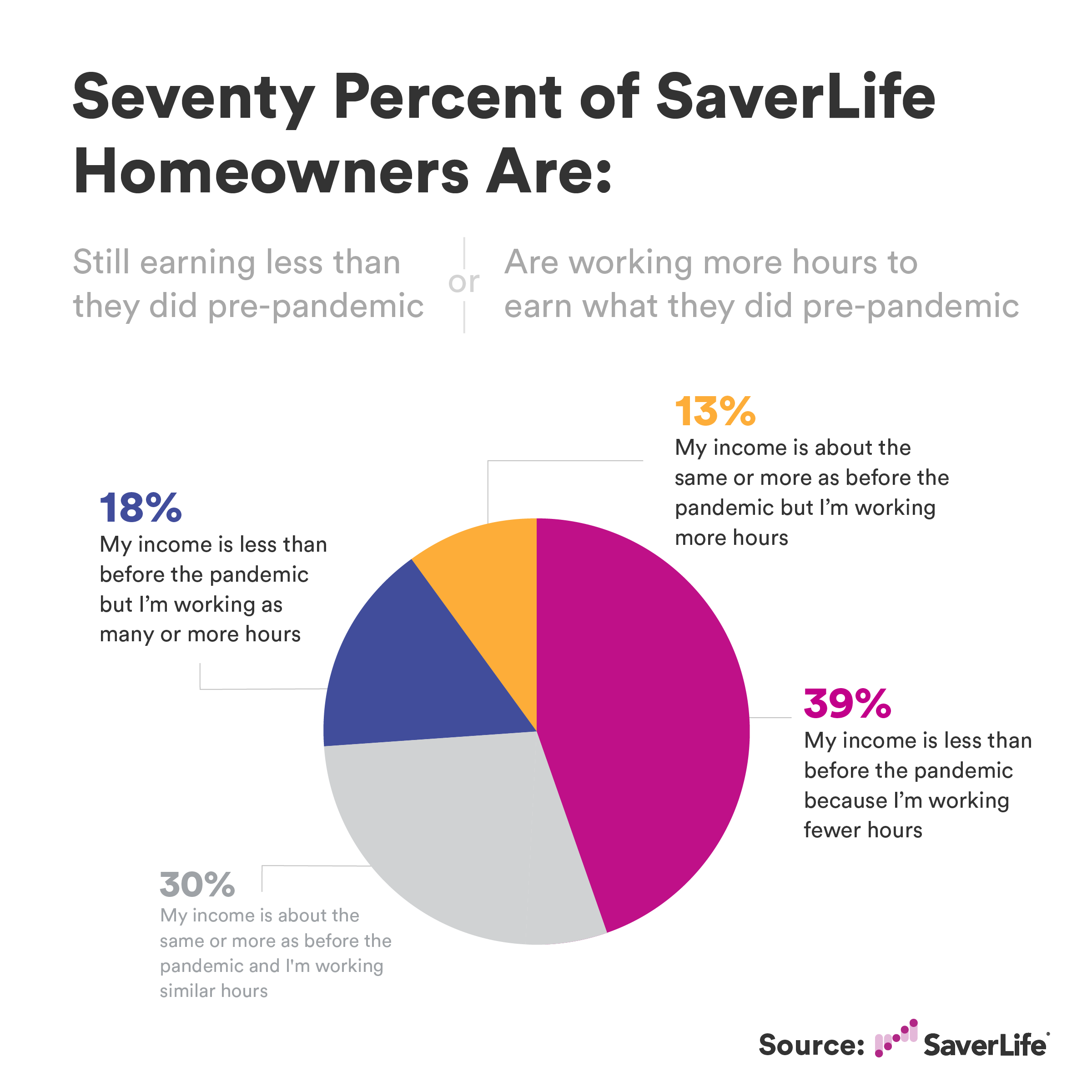

Homeowners hit hard by the pandemic are falling behind, with many struggling to find quality jobs that pay a living wage. Fifty-seven percent of respondents said their post-pandemic income declined. Of those who reported being employed, about 4 in 10 (39%) earned less income because they worked fewer hours. Another 18% reported working more hours but not earning enough to replace their pre-pandemic income. Notably, men were far more likely (23%) than women (11%) to report working more hours; this result is consistent with widespread reports on structural hurdles, such as disproportionate parental and elder care responsibilities, that continue to delay women’s return to the job market.

Tenesha lost her job as a server in March 2020 because her restaurant closed permanently. She’s still searching for work. The enormous financial burden facing this demographic is severe and possibly deeper than the barriers facing 37.5% of US adults, who, according to the Census Bureau’s Household Pulse Survey, experienced income declines.

The over-representation of minorities and women in SaverLife’s sample provides an important snapshot of the pronounced adversity facing homeowners of color. This real-time pulse check suggests that premature withdrawal of critical federal and state subsidies would exacerbate the hardships faced by communities of color and undermine recovery for other economically disadvantaged groups, including women and younger Americans.

Many homeowners were unaware of and missed the forbearance window

The CARES Act circumvented an epic housing instability crisis for both renters and homeowners. Since last spring, more than 6 million borrowers have sought payment relief through forbearance. Although forbearance provided millions of distressed borrowers with vital breathing room, a substantial share of COVID-impacted homeowners missed the chance to participate in a forbearance program.

Participation in forbearance plans was remarkably low—just 8% of respondents reported having received a forbearance plan. This rate is unexpectedly low given respondents’ reportedly high rate of income disruption and the trend of working longer hours to keep up. Michelle, a Wisconsin resident, heard that forbearance could have negative consequences down the road, and opted not to apply even though she struggles to pay her mortgage. Unlike Michelle, borrowers who opted into forbearance plans did so out of necessity; the majority of those who froze their mortgages (55%) experienced some form of income disruption. This finding is consistent with studies from JP Morgan and others showing that most borrowers did not engage in opportunistic moral hazard behaviors such as opting into forbearance plans even though there was no change in their financial circumstances.

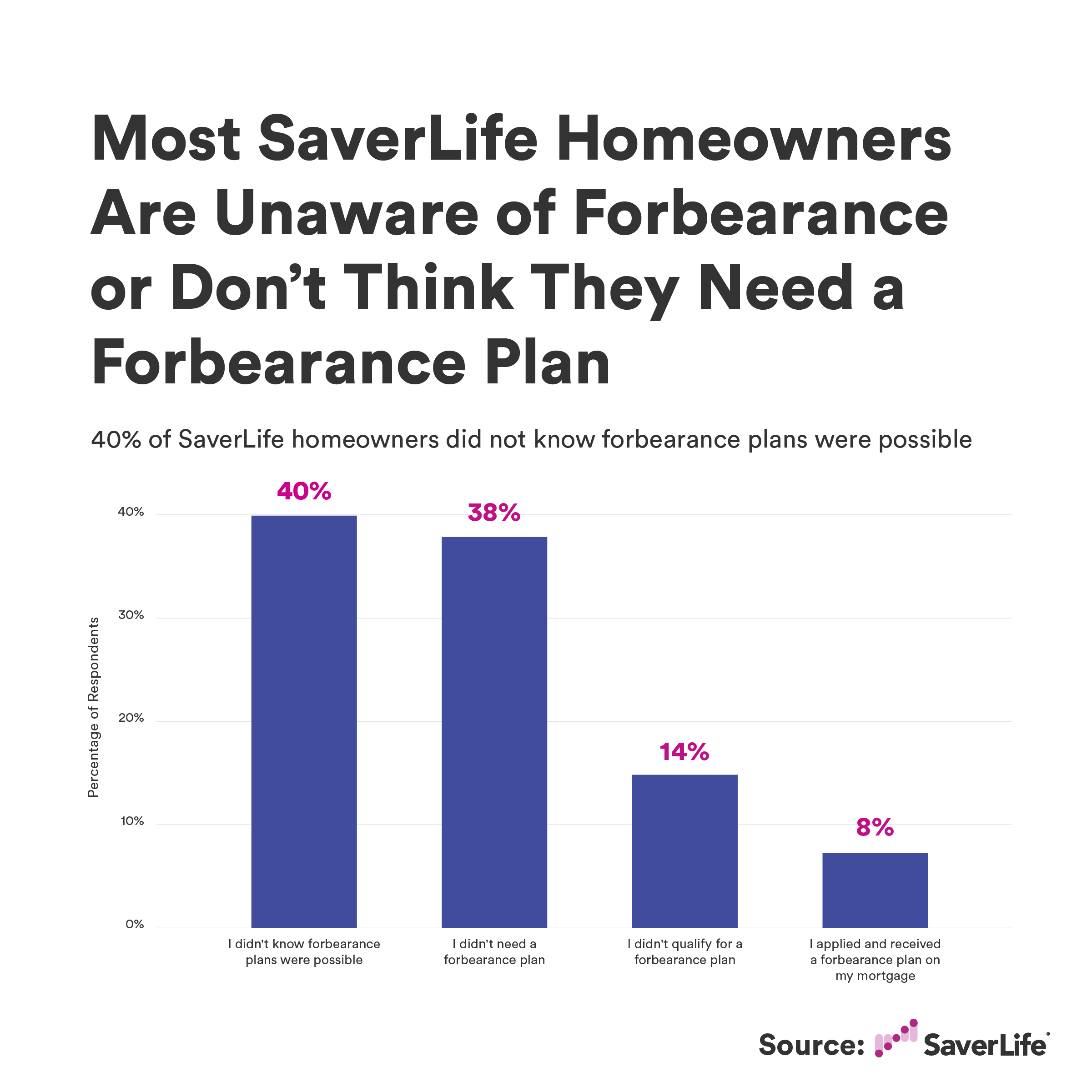

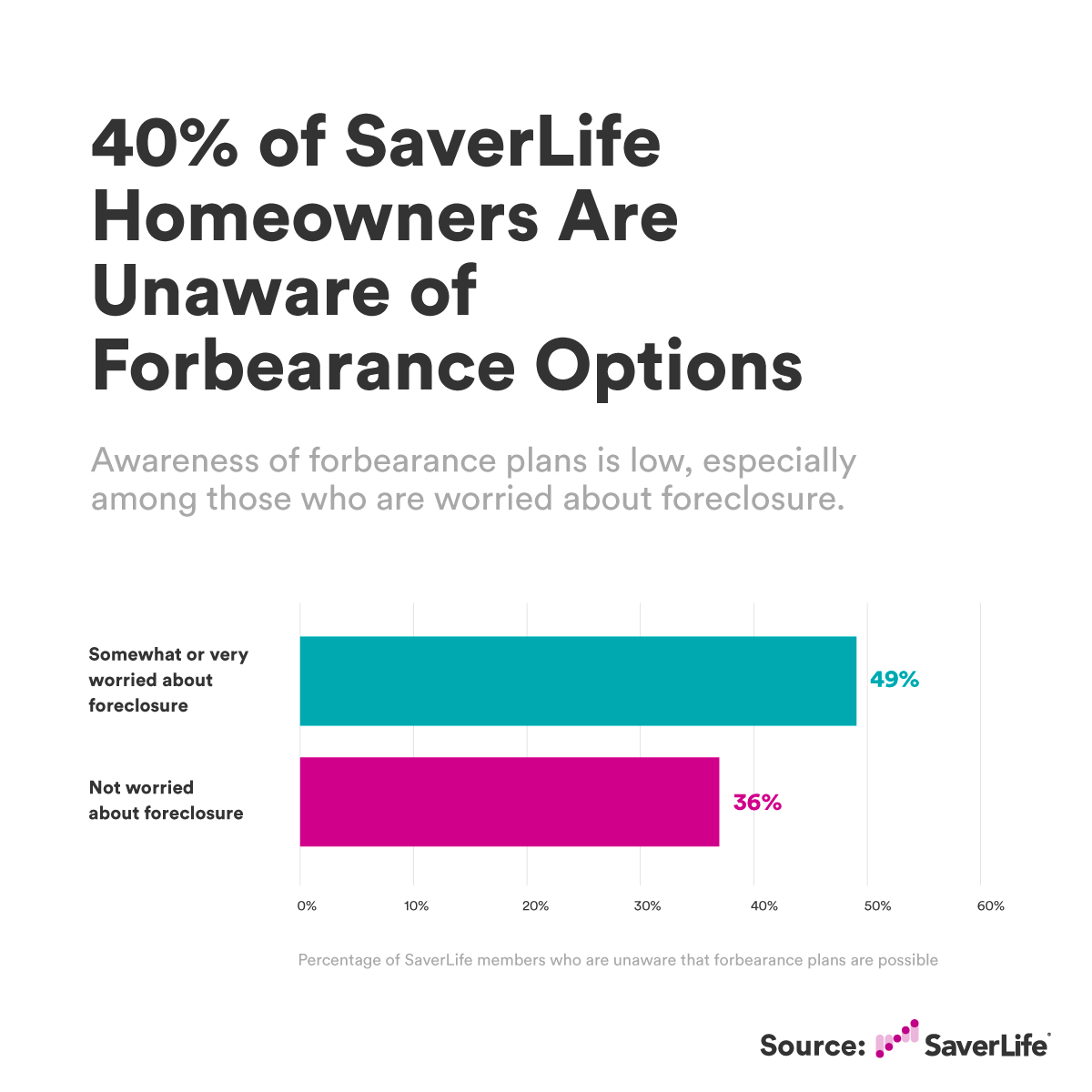

Despite reaching its target market, the CARES Act failed to protect many. Tenesha was unaware of forbearance relief and didn’t apply. A significant share of polled participants (40%) said they were unaware of forbearance as an option for mortgage relief. Nearly half of these respondents (49%) reported being worried about foreclosure. Additionally, 14% of survey participants believed they were ineligible for a COVID-payment deferral program. Among them, 8 out of 10 reported earning less than their pre-pandemic income—a key qualifying characteristic for the program.

Notable differences emerged across racial and ethnic groups as well. For instance, Hispanic homeowners were twice as likely as Black and white homeowners to receive a forbearance plan. However, on average, Hispanics reported being unaware of relief options at moderately higher rates (44%) than Blacks (38%) and whites (40%) who were unaware of forbearance plans.

Early on, Fannie Mae raised concerns that familiarity with forbearance relief was alarmingly low among homeowners with incomes below $50,000: 56% were unaware of payment deferrals. A confluence of factors, including widespread misinformation about eligibility, fees, credit score penalties, and lump sum repayment obligations, could explain this frustrating pattern. Unfortunately, these racial disparities transcend the survey sample: a corroborating study by the Federal Reserve Bank of Philadelphia found that non-whites and Hispanics were more likely than whites to cite these concerns as reasons for forgoing forbearance protections. Together, the evidence suggests that critical information asymmetries suppressed participation rates in many corners of hard-hit communities of color.

Homeowners are increasingly fearful of losing ground

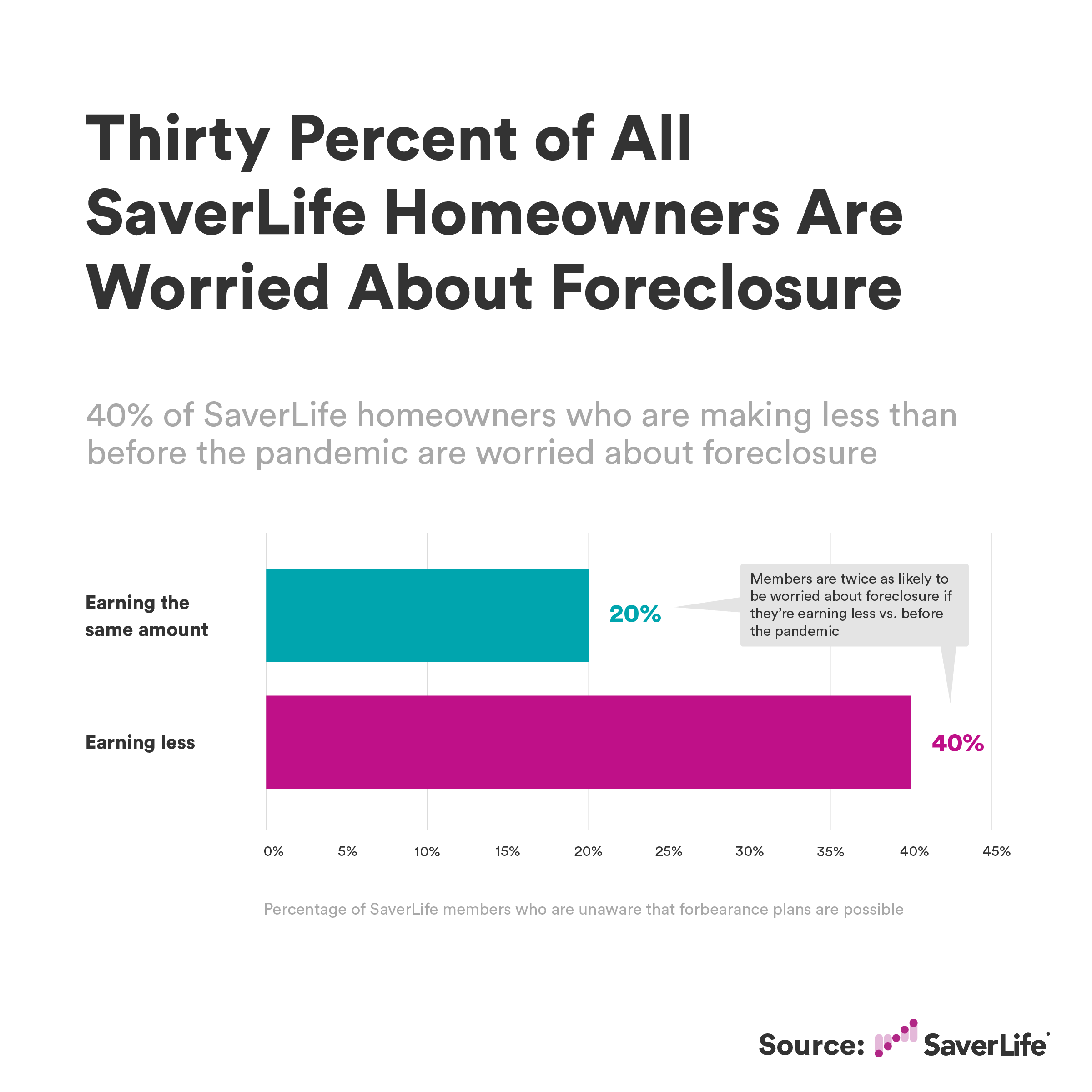

The protracted COVID recession has placed mounting pressure on stressed homeowners who are struggling to recover and are increasingly concerned about losing their homes. Nearly a third (30%) of respondents feared losing their homes to foreclosure, and individual financial circumstances were a key driver of this sentiment. The 40% of homeowners who reported earning less were twice as likely to be concerned about a possible foreclosure than the 20% of respondents whose financial conditions remained relatively stable.

The 24% of respondents who worked fewer hours were three times more likely to be extremely anxious about foreclosure than those who had experienced virtually no change in their employment situation (8%). Fear of foreclosure was particularly high among Hispanics with lower incomes: more than half (54%) of this homeowner segment stated they were worried about losing their homes to foreclosure. Despite racial disparities, white respondents were hardly immune to this dynamic: more than a third (37%) were equally worried about foreclosure. Such concerns were not unique to this particular segment; nationally, Freddie Mac estimates that 2 in 5 homeowners (41%) are concerned about their ability to make mortgage payments in the near future.

Some have argued that concern about foreclosure is irrational. However, SaverLife’s homeowners’ experiences contradict this claim and make one fact painfully obvious: many homeowners are currently employed but do not earn nearly enough to maintain mortgage payments alongside other monthly expenses. According to Upjohn Institute’s New Hires Quality Index, which tracks occupational-adjusted wages of new hires, Blacks and Hispanics are returning to the job market through lower-paying occupations with average hourly wages of $16.01 and $15.47, respectively. That’s just $32,740 per year—far short of the minimum annual salary necessary to pay basic living expenses, including a mortgage.

The data show that low-wage and part-time work, not irrationality, drives the foreclosure fears of financially strained homeowners. Shay’s forbearance application never made it through her mortgage servicer’s backlog; she relies on her unemployment benefits to continue making mortgage payments. Quelling Shay’s anxieties, and others like her, will largely depend on her ability to access jobs paying above subsistence wages, which is unlikely to materialize before the foreclosure moratorium expires.

It’s too early to pull the plug: Struggling homeowners need more support, not less

The extreme disruptive effects of the pandemic have begun to wane. Of course, policymakers are eager to normalize the economy, including withdrawing or reducing subsidies such as unemployment benefits. But it would be a mistake to pursue this strategy. Nearly 40% of workers with incomes below $50,000 reported losing their jobs or being laid off, according to the latest Survey of Household and Economic Decisionmaking (SHED) data—more, not less, support is needed to bolster their recovery.

There is an enormous opportunity to avert a foreclosure crisis if states strategically invest the $10 billion 2021 Homeowners Assistance Fund (HAF). The HAF provides states with a wide range of options to mitigate borrower hardships. While resolving backward-looking obligations (such as overdue utility and property tax bills) is a critical aspect of home preservation, the benefits will likely be too short-lived to have a measurable long-term impact. Instead, states should prioritize relief options that make mortgage payments affordable, including making refinancing more accessible. States should provide distressed borrowers with HAF grants to lower the costs of refinancing.

Importantly, these subsidies should cover any cash required to bring down interest rates to an affordable expense-to-income ratio or to ensure that replacement loans conform to loan-to-value overlays. Moreover, states should make corresponding investments in community-based organizations to educate impacted borrowers about available options. Closing information gaps is crucial to improving participation in mortgage relief schemes. Therefore, states must strengthen the capacity of counselors and navigators to empower distressed borrowers and launch public information campaigns that target platforms where those who would most benefit from relief options can be informed.

HAF is an exemplary racial equity paradigm that recognizes the singularity of homeownership in creating wealth for Blacks and Hispanics. HAF marks a commendable start to encouraging inclusive economic recovery, but it is not nearly enough to meet the needs of jobless individuals. Millions of low-income and minority homeowners remain unemployed. This is morally unacceptable. The Biden administration must extend the foreclosure moratorium and continue to make federal forbearance available to unemployed homeowners. Failure to expand these accommodations compromises the immense amount of equity minority families have invested in their pursuit of homeownership and undermines conscious efforts to close the racial wealth gap.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Low to moderate-income families are losing ground: How to save their homeownership dreams

Thursday, June 24, 2021