Since the pandemic, Americans have ranked the cost of living (often labeled “affordability”) as the top problem they want America’s leaders to address. The typical household budget has many different components, of course. Some of them, such as health care, have been pressuring families for several decades. Problems in other areas, such as housing, have become acute only in recent years. But the rapid rise in overall prices since the beginning of the pandemic has merged these areas into a broader public concern. Although average hourly wages have risen by 30.8% since then1, costs for many core elements of household budgets have risen even more, and most Americans feel that they are at best running in place.2 Because the rate of price increases remains well above the Federal Reserve Board’s target of 2%, this concern shows no sign of abating, and the effects of the war with Iran will make matters worse.

Health care

Between 1999 and 2024, health care rose from 13% to 18% as a share of GDP, an increase that has serious consequences for family budgets. While wages rose by 119% during this period, workers’ contributions to family health care insurance premiums surged by 308%, almost three times the pace of wages. This increase was not the result of employers shifting the burden of health insurance to workers; the overall cost of insurance premiums rose even faster, by 342%—more than five times as much as the economy-wide rate of inflation. Since the pandemic began, the burden on average families has accelerated: Out-of-pocket expenses per person rose by nearly one-third, from $1,239 to $1,652, in just five years.

Against this backdrop, it is not surprising that health care has risen to the top of Americans’ concerns about affordability. A recent survey found that 32% of respondents were “very worried” about health care costs, compared to 24% for food and groceries, 23% for rent or mortgage payments, 22% for utilities, and 17% for gas and other transportation.

Because the problems of health care in the U.S. are structural and deeply rooted, the prospects for quick relief are not bright.

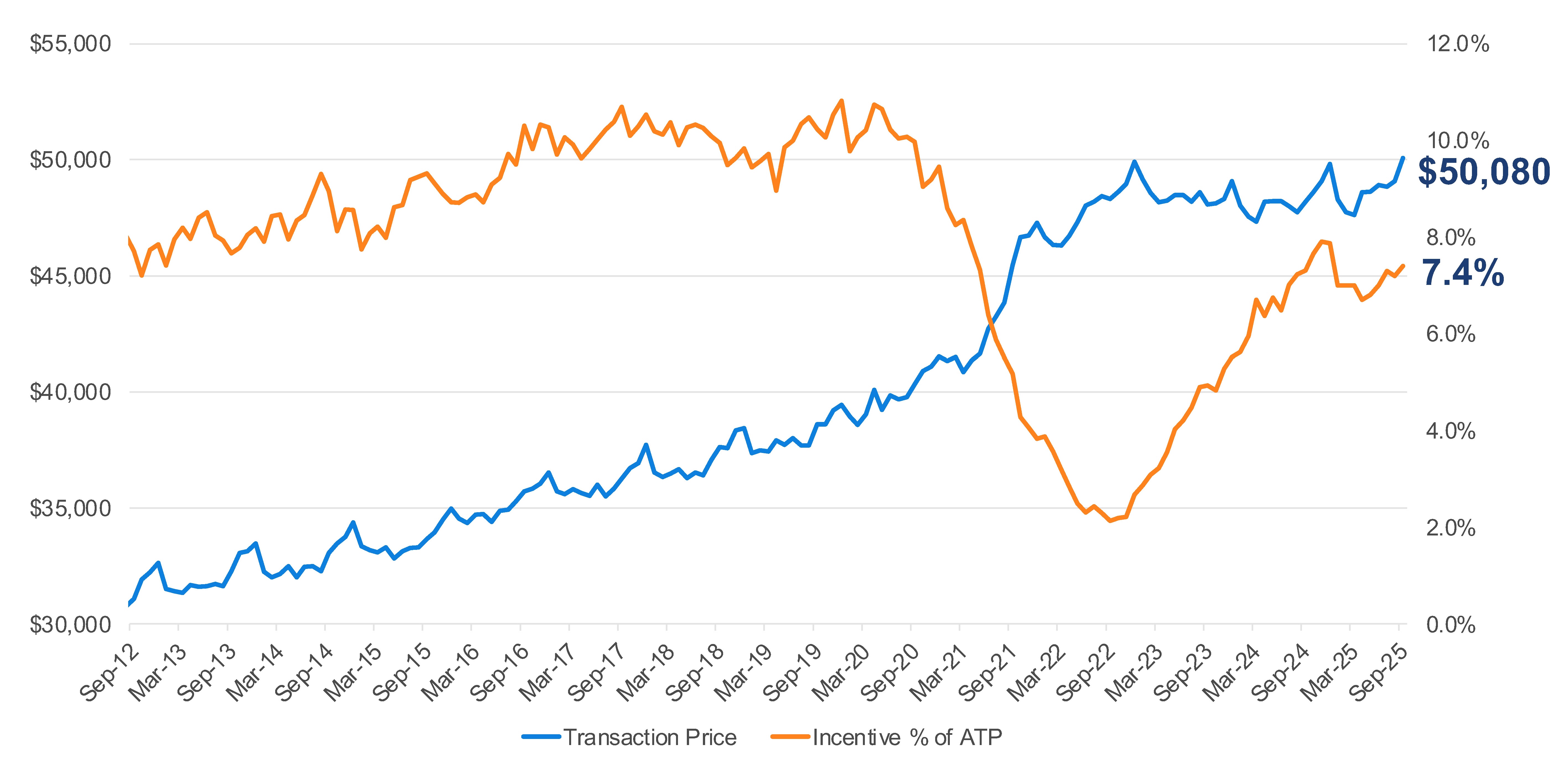

Housing

Unlike health care, the housing affordability crisis mostly began with the pandemic. Since early 2020, the cost of median-priced housing has risen by 28%, from $317,000 to $405,000, while mortgage interest rates surged from 3.45% to 6.11%.

These increases have disrupted the long-established balance between housing prices and household incomes. Until 2020, a median-income household could afford mortgages to buy median-priced homes. Now, households need incomes of $120,000 to qualify for such mortgages, but the median income stands at only $85,000. Otherwise put, families in the middle of the income distribution can afford houses that cost about $330,000, 20% below the sales price of the median home. The result: the majority of homes are now beyond the reach of average families.

This development has hurt young families trying to buy their first homes especially hard. For decades, the median age for first home purchases moved in a narrow range between 29 and 31 years—about when young adults were getting married and starting families. Today, the median age for first home purchases stands at 40 years. Families headed by young adults in their 30s are stuck in apartments that are too small, many in locations that no longer meet their changing needs.

Mounting evidence suggests that the receding prospect for homeownership has troubling ripple effects. Because home ownership is the most reliable source of wealth accumulation for average families, lower rates of homeownership will diminish the assets on which many families can draw as they move through the life cycle. Young adults who have given up on homeownership have no incentive to save for a down payment, reducing their savings rate and encouraging an outlook focused on the present, not the future. Some are plunging into sports betting, while others are turning to risky investments that are hard to distinguish from gambling. When traditional paths to economic mobility seem blocked, the calculus that leads working-class Americans to buy lottery tickets spreads to educated young people. Homeownership has positive externalities that will be hard to replace.

Groceries

For most Americans, trips to the grocery store provide the most regular and vivid indication of what is happening to prices. Since the beginning of the pandemic, the news has been mostly bad. Overall grocery prices have risen by 31% since February 2020, and for some high-profile items—ground beef, for example—the increase has been much steeper.

Even short-term changes are noticeable. The government’s inflation report for February 2026 showed grocery prices rising by 0.4% during the month, an annual pace of roughly 5%. There was bad news for salad-eaters: Lettuce prices rose by 12.2% during the month, and tomatoes, 6.4%. Coffee prices, which rose by 18.4% in 2025, increased by another 1.7% in February.

The surge in energy prices resulting from the war in Iran will probably ratchet grocery prices up another notch. Much of the food U.S. consumers buy is transported long distances from the point of production, and many of the factories that produce fertilizer for U.S. farmers are located in the Persian Gulf.

Other key elements of the affordability issue

Utilities

Household utility costs have risen by 41% in the five years after the beginning of the pandemic. Electricity is up 32%, water 43%, and natural gas 60%, and 17% of households have fallen behind on their monthly electricity bills. These figures help explain the political sensitivity of AI data centers, which consume large amounts of water and put upward pressure on household electricity rates.

Automobiles

Since the onset of the pandemic, the average price of a new car has risen from $38,000 to $50,000, an increase of 32%. Hard-pressed consumers who turned to used cars found little respite; used cars rose by 28% during this period. And auto purchasers have been hit by an array of rising fees, such as “destination charges” for moving purchased autos to the point of sale. Meanwhile, auto insurance premiums have risen by a stunning 55% since the pandemic began.

Child care

Between 2020 and 2024, the average cost of child care rose by 29%, 7 points more than the overall inflation of 22% during these years. Starting in mid-2024, the pace of child care inflation accelerated to twice the rate of overall inflation, a trend that persisted through 2025. Parents are increasingly likely to cite the costs of child-rearing as hard to manage and as a reason to have fewer children than they otherwise would have.

The politics of affordability

The political power of affordability became undeniable when Zohran Mamdani won an improbable victory last November in the contest for mayor of New York, while Mikie Sherrill and Abigail Spanberger won the governorships of New Jersey and Virginia by surprisingly wide margins. Since then, Democratic candidates have continued to press their Republican opponents on the issue, and the inflationary effects of the war in Iran may make the midterms even tougher for the GOP.

The affordability issue has affected President Trump’s standing as well. Most Americans believe that his priorities do not align with theirs, and they want him to focus more on the bread-and-butter challenges they face every day. Whatever the merits of the president’s claim that he inherited these challenges, Americans reject it by a margin of 2-to-1. It is Mr. Trump’s economy now, and Americans want him to do more to fix it than he has so far.

The electorate’s judgment matters because President Trump’s job approval affects his party’s prospects in the forthcoming midterm election. Right now, his dismal approval rating of 34% for his handling of inflation is endangering the survival of Republican House candidates in swing districts and is raising the odds (which are still low) that Democrats will take control of the Senate. With the war in Iran raising energy prices, which will flow through much of the economy, the time for the administration to turn this around is growing shorter.

Related Content

Author

-

Footnotes

- [Source: Author’s calculation, based on Average Hourly Earnings of All Employees, Total Private (CES0500000003) | FRED | St. Louis Fed.]

- [One reason for this disjunction: Although average hourly wages rose faster than inflation, these gains have not been reflected in overall household incomes. Corrected for inflation, median household income was no higher in 2024 than in 2019, right before the pandemic began. The figure for 2025 will not be released until September 2026.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

{kind=link}

Commentary

Why affordability will be a key issue in the 2026 midterm elections

March 25, 2026