President Biden’s proposal to spend another $1.9 trillion to shore up the COVID-ravaged U.S. economy is prompting a debate over how much fiscal stimulus is too much. One element of the debate compares the likely path of Gross Domestic Product (GDP) to estimates of potential GDP. So what is potential GDP? And why is it controversial now?

What is potential GDP?

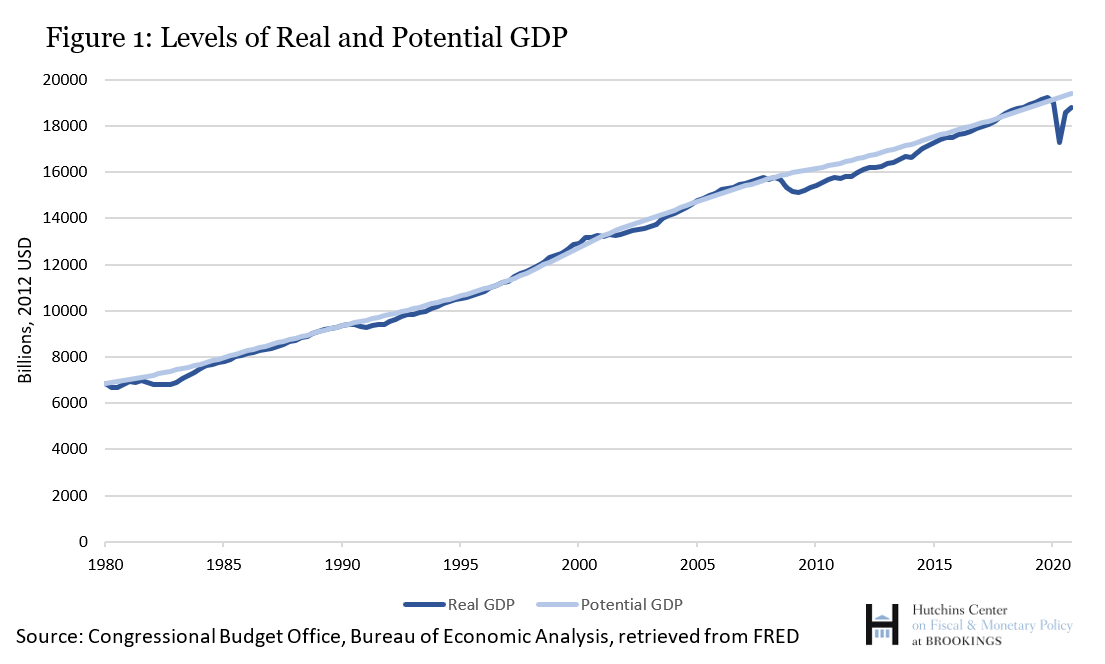

Gross Domestic Product is a measure of the value of all of the goods and services produced in the economy in a given period. It is calculated by the federal government’s Bureau of Economic Analysis each quarter. Potential GDP is a theoretical construct, an estimate of the value of the output that the economy would have produced if labor and capital had been employed at their maximum sustainable rates—that is, rates that are consistent with steady growth and stable inflation. Figure 1 compares the levels of real GDP and potential output over time. In general, the economy operates close to potential, but deep recessions are notable exceptions to the trend. In these episodes, GDP can lag behind potential, sometimes persistently.

Click figure to enlarge.

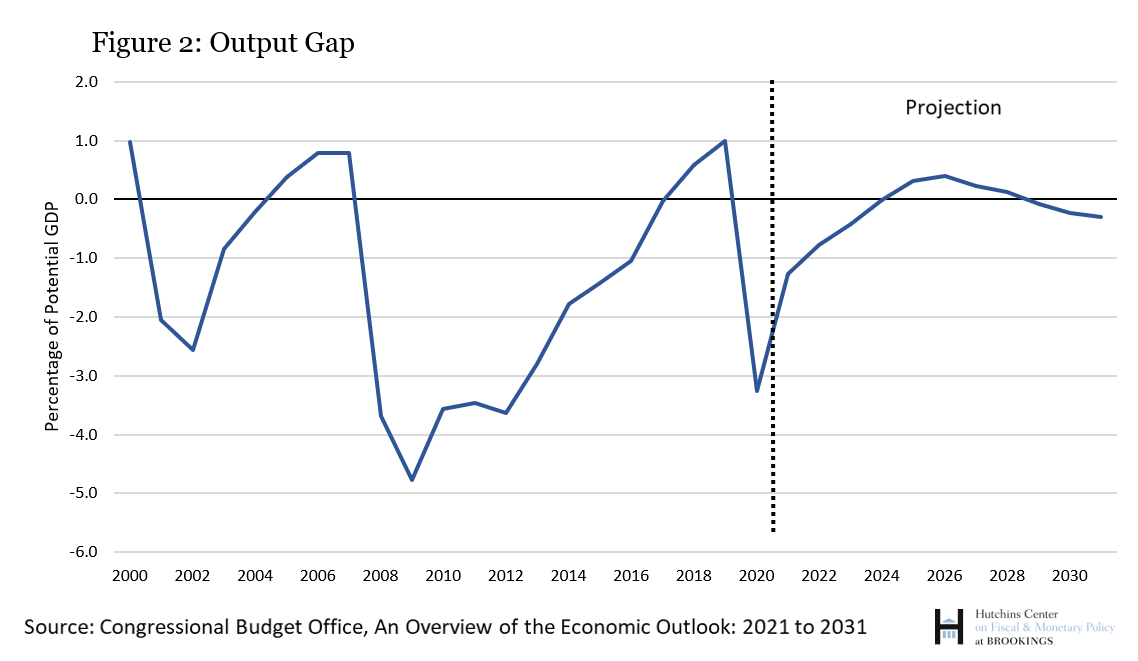

The difference between the level of real GDP and potential GDP is known as the output gap. When the output gap is positive—when GDP is higher than potential—the economy is operating above its sustainable capacity and is likely to generate inflation. When GDP falls short of potential, the output gap is negative. Figure 2 shows that recessions such as the Great Recession of 2007-2009 and the COVID-19 recession feature GDP well below potential.

Click figure to enlarge.

Why does it matter?

Over time, an economy can grow without unwelcome inflation only as fast as its potential GDP grows. Think of this as the safe speed limit for economic growth. Too much government spending can produce a surge in demand that exceeds the economy’s capacity to produce and triggers inflation.

Understanding potential GDP is important to Federal Reserve policymakers as they decide when and how to change interest rates or use their other tools to deliver on their mandate of price stability and maximum sustainable employment. Having good estimates of potential output allows them to calibrate their choices based, in part, on projections of the output gap. Similarly, Congress and the President will look to the output gap to contemplate whether the economy needs fiscal stimulus or restraint.

What determines potential GDP?

Potential GDP depends on the size of the labor force and the pace of productivity growth (output per hour of work), which itself is dependent on the amount of capital investment. That is, potential GDP growth can accelerate if more people enter the labor force, more capital is injected into the economy, or the existing labor force and capital stock become more productive.

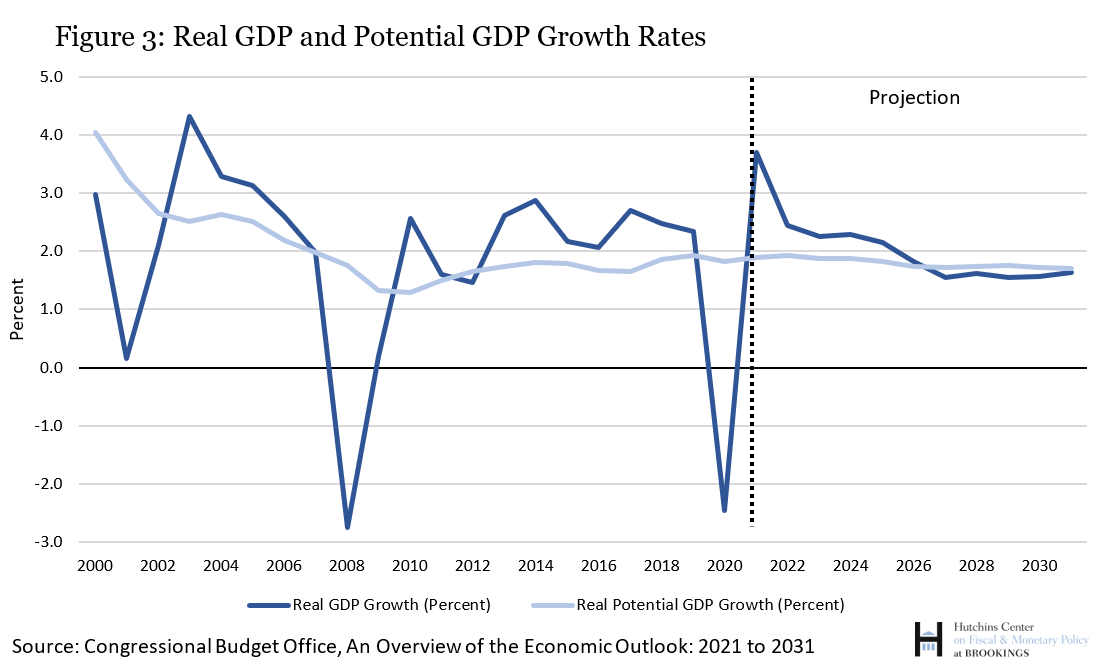

As shown in Figure 3, Congressional Budget Office (CBO) estimates of potential GDP growth fell in the early 2000s as labor force growth declined because of factors including population aging and slowing productivity growth. Their estimate of potential has been relatively stable since. Actual GDP growth, on the other hand, shows large cyclical patterns—falling sharply during recessions and increasing more modestly above potential during expansions.

Click figure to enlarge.

Why is potential GDP so hard to project?

The underlying components of potential GDP are not directly measurable. This makes the process of estimating it inherently difficult and reliant on model-based predictions. Different approaches to measuring potential GDP yield different estimates of how fast the economy can grow without leading to inflationary pressure.

Projecting potential GDP in the wake of the pandemic is particularly difficult because it is likely that potential GDP has itself been affected, at least temporarily. Many businesses have closed, workers have left the labor force, and employee-employer relationships have severed, so it may be some time before the productive capacity of the economy returns to where it would have been without the pandemic. In addition, declines in immigration and investment during the pandemic mean a smaller labor force and capital stock, both of which lower potential GDP.

Of course, based on the unprecedented nature of the pandemic, gauging the magnitude and persistence of these effects on the economy is difficult. The Congressional Budget Office estimates that potential GDP will grow at 1.85 percent in 2021, down from its estimate of 2.02 percent made in January 2020 before the pandemic began.

Why is potential GDP so controversial now?

As President Biden and Congress negotiate the next fiscal stimulus package to aid the COVID-19 economic recovery, they will implicitly be making assumptions about the output gap. Analysis by one of us (Louise Sheiner) and our Brookings colleague Wendy Edelberg suggests that Biden’s $1.9 trillion package would result in GDP reaching its pre-pandemic path by the end of 2021 and exceeding it in 2022. In other words, some of the economic activity lost during the pandemic would be made up after the virus subsides.

Based on the CBO’s recent estimate of potential GDP, though, this would leave a large positive output gap—peaking at 2.6 percent in the first quarter of 2022. Some critics—including former Treasury Secretary Lawrence Summers—argue that pushing output this far above potential could drive up inflation.

Others, including Nobel Laureate Paul Krugman, warn against putting too much emphasis on a projected output gap in determining the riskiness of a large fiscal stimulus. They note the significant uncertainty that surrounds any estimate of potential GDP. Indeed, by CBO’s estimates, the U.S. economy was operating above potential in 2019, yet inflation remained subdued and below the Fed’s 2 percent target. Moreover, there is little historical precedent to predict how the pandemic will affect potential output or consumer and business demand once the virus recedes.

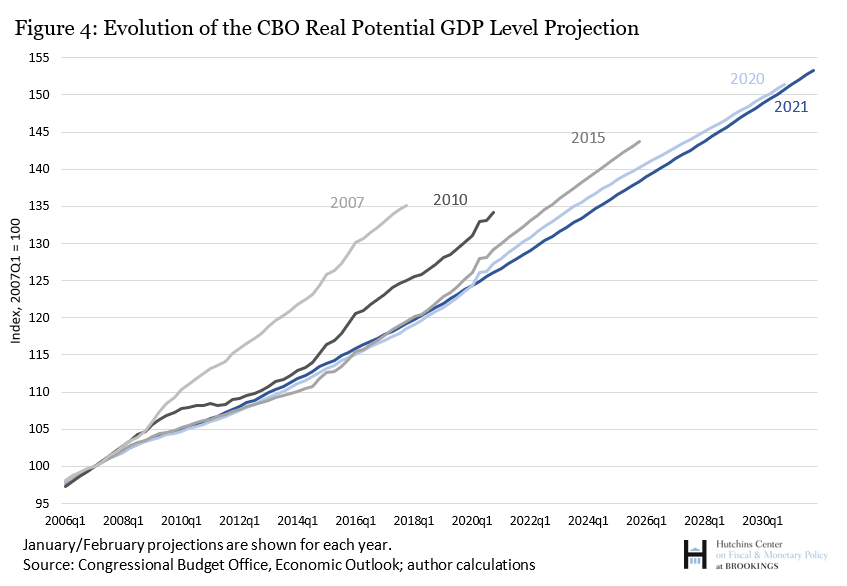

Click figure to enlarge.

Illustrating how hard it is to project potential output, Figure 4 shows that CBO consistently downgraded its estimates of potential GDP from early 2007 through February 2021 in the aftermath of the Great Recession and the subsequent recovery as well as the COVID-19 pandemic. At Goldman Sachs, economists Daan Struyven, Jan Hatzius, and Sid Bhushan argue that this trend offers evidence that potential GDP is higher than models such as the CBO’s suggest, meaning the economy has more slack. Assuming that the downward trend in the prime-age male employment/population ratio could be reversed by a strong economy, they estimate that the U.S. economy is 3 to 4 percentage points further below potential today than CBO estimates imply. Coupled with the uncertainty noted above, this result suggests that estimates of the output gap should not be taken as the sole indicator of the condition of the economy or as a foolproof indicator of impending inflation pressures.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

What is potential GDP, and why is it so controversial right now?

February 22, 2021