In the course of making monetary policy and issuing currency, the Federal Reserve accumulates a portfolio of Treasury and agency securities, which earn interest. Its liabilities consist primarily of currency outstanding, which of course pays no interest, deposits of the U.S. Treasury, which also pay no interest, and reserve deposits of banks and repo borrowing from money market funds and other lenders, both of which do pay interest. Normally, the interest the Fed earns on its securities greatly exceeds the interest it pays to banks and money funds, and the Fed meets its expenses from the surplus and remits the rest to the Treasury.

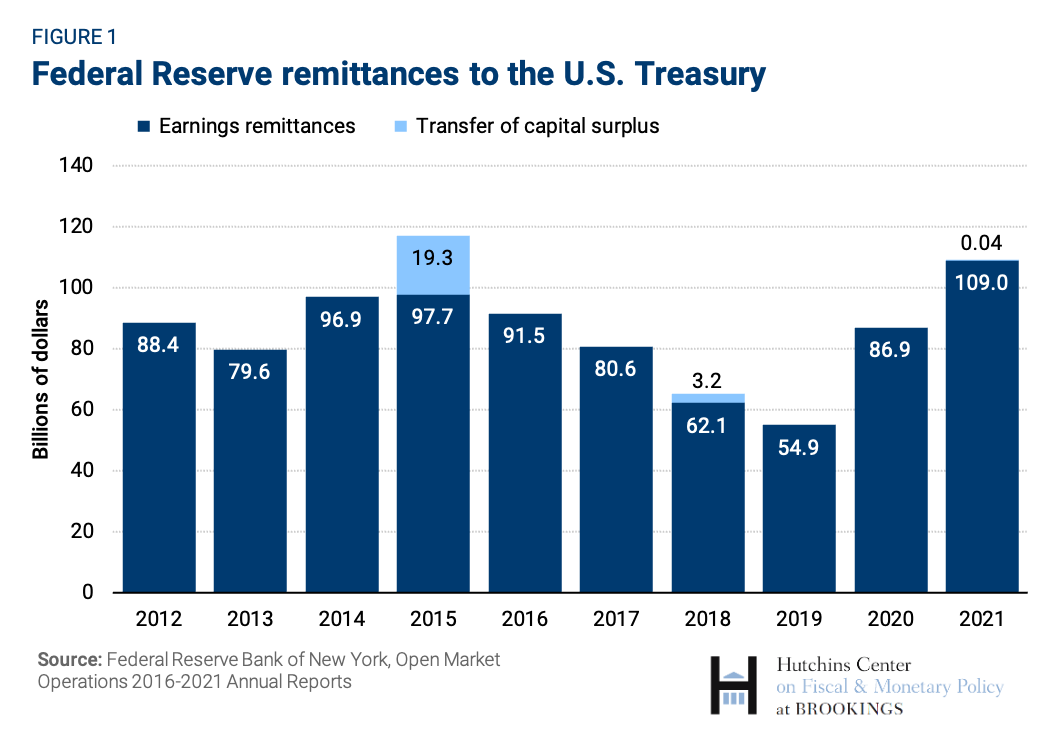

In response to the COVID pandemic, the Federal Reserve used quantitative easing (QE) – that is, large-scale purchases of Treasury securities and agency mortgage-backed securities – both to support market functioning and to ease financial conditions and strengthen the economic recovery. Its securities portfolio grew from less than $4 trillion to $8.5 trillion between March 2020 and March 2022.[1] Over the same period, currency expanded from $1.8 trillion to $2.3 trillion, and the Treasury’s account at the Fed rose from $0.4 trillion to $0.6 trillion. Despite the more modest growth in the Fed’s noninterest liabilities, the interest earnings on the Fed’s securities holdings increased much more than the interest paid on its liabilities, and the Fed’s remittances to the Treasury rose from $55 billion in 2019 to $87 billion in 2020 and $109 billion in 2021.

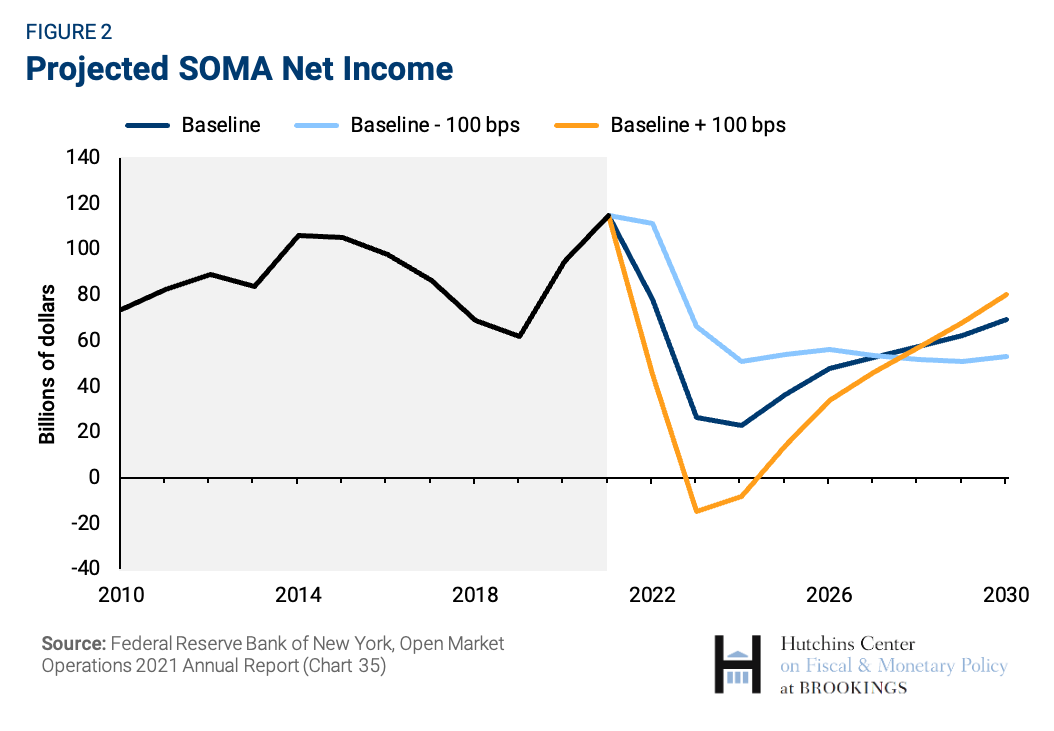

However, with the Fed now raising rates “expeditiously,” the Fed’s net interest income on its securities holdings will fall as the rate earned on the securities it holds remains relatively fixed while the interest rate it pays on its liabilities rises. The Fed has noted that if interest rates rise sufficiently high, it could end up paying more out in interest than it takes in, resulting in a loss for the Fed.

This post discusses whether such losses have significant implications for monetary policy, and the extent to which the Fed’s losses are a cost to the taxpayer and the broader U.S. economy.[2]

What would happen if the Fed had a loss?

If the Fed booked a loss in a given year, it would have no profits to remit to the Treasury. Under the Fed’s accounting rules, it would then accumulate a “deferred asset” equal to its cumulative losses. Once the Fed returned to profitability, it would retain profits to pay down the deferred asset. Only once the deferred asset had been reduced to zero – that is, once the Fed had retained earnings offsetting its earlier losses – would the Fed resume remitting profits to the Treasury. (For details, see Carpenter et al (2015)).

Would those losses have any implication for the Fed’s ability to make monetary policy?

No. Despite any plausible losses, the Fed could continue to operate normally and implement monetary policy. In particular, the Fed could still raise and lower its target range for the federal funds rate and adjust the size of its portfolio to influence financial conditions as appropriate given economic conditions.

Should the Fed worry about possible losses in setting monetary policy?

The Fed is not a profit maximizing institution. It is not a bank or a hedge fund. It is, rather, a public institution with public objectives. The Fed’s monetary policy objectives, as set by Congress, are maximum employment and stable prices. And Congress has given the Fed tools to use to foster those objectives, including the ability to control short-term interest rates and the authority to purchase Treasury and agency securities. While purchases of longer-term securities can, in some circumstances, lead to losses for the Fed, the Fed’s mandate is neither to make profits or to avoid losses. The Fed should use its tools to achieve its mandate.

Are Fed losses a problem for the Treasury and the taxpayer?

Although unexpected increases in interest rates can lead to Fed losses and lower-than-expected remittances to the Treasury, there are a number of reasons why losses for the Fed are not equivalent to losses for the taxpayer or for the country as a whole.

First, even if QE leads to Fed losses in some periods, it will likely also boost Fed profits in other periods.[3] Thus, the losses in a given year may simply offset a portion of the profits in other years, leaving the overall effect on Fed income positive.

Second, the Fed does QE to put downward pressure on longer-term interest rates. Thus, if the policy is effective, QE will reduce the interest that the Treasury pays on its long-term debt. So even if the Fed has losses over time on its holdings, there may be no net loss for the Treasury and thus for the taxpayer.

Third, the easier financial conditions caused by the QE help boost output and employment – indeed, that is the point of conducting QE when the Fed’s short-term policy rate is constrained by its lower bound. But higher output and employment increase tax revenues and reduce government expenditures on safety net programs. Thus, the net effect of QE on the budget can be positive even if the Fed has losses for a time.

One way to summarize the effects of QE on overall costs to the taxpayer is to look at the cumulative effect of the QE on the ratio of federal debt to GDP over time. In a memorandum to the FOMC, Clouse et al (2013) used the FRB/US model to evaluate these different effects. Their analysis indicates that, even in cases where interest rates rise considerably faster and further than expected and the Fed posts significant losses, the total effect of QE can be to reduce the debt-to-GDP ratio. That is, despite the Fed’s losses, the taxpayer can be significantly better off with the QE.

And, of course, the effects on Treasury finance are not a full measure of the welfare effects of the QE. Since output and employment will be higher as a result of QE, many workers and their families will be better off, regardless of the effects on the federal budget. In short, when considering the desirability of QE, policymakers need to assess the full set of its effects and should not focus on the Fed’s income statement.

But couldn’t Fed losses lead it to default in some way, causing a financial crisis or high inflation?

The Fed can’t default because it can always create reserves to pay its bills. Moreover, the banking sector must hold the reserves created by the Fed, so the Fed cannot suffer from a run on its funding. That said, if the Fed had large enough losses for a long enough time, it would have to create such a large amount of interest-bearing liabilities to cover its expenses that it wouldn’t be able to implement monetary policy appropriately. (In terms of the Fed’s accounting, its losses could outstrip all its future profits.) In that extreme case, the Fed would need to get fiscal support from the Treasury. At times, some foreign central banks have had losses in excess of their capital and nonetheless continued to operate effectively (Chaboud and Leahy, 2013).

Happily, the Fed’s future profits are likely to be substantial, since more than $2 trillion of its securities holdings are financed by currency, on which the Fed pays no interest. Given the low level of real interest rates in recent years and the likely growth of currency along with the economy, the present discounted value of future Fed profits is very large – in the trillions of dollars – and so it would take truly colossal and highly improbable losses before the Fed might be unable to implement monetary policy effectively. (Hall and Reis (2015) examine this issue.)

Even if the Fed can’t default, couldn’t losses undermine the Fed’s independence?

Even if Fed losses don’t constrain monetary policy or necessarily impose a cost on taxpayers, the Fed’s actions often are controversial. Substantial losses could trigger criticism on Capitol Hill, particularly if rising interest rates become a political issue. Even short of losses on the Fed’s books, rising interest rates increase the cost of financing the national debt. Eliminating Fed remittances for a few years as a result of losses would make the budget situation even more challenging. However, like monetary policymakers, politicians and the public should take account of the full range of effects of QE and not focus undue attention on Fed income. The Fed can help foster such a balanced assessment by using its communication and outreach to ensure that the public and the Congress understand the benefits of QE and how it can help the Fed achieve its policy objectives, as well as the potential risks. In order to allay any concerns, the Fed should emphasize now that losses will not constrain its ability to continue to implement monetary policy in the pursuit of its maximum employment and price stability objectives.

[1] Indeed, Fed remittances to the Treasury have averaged $72 billion per year since the first QE program was introduced in late 2008, nearly three times the $26 billion per year averaged over the previous decade.

[2] The Fed values its securities on an amortized cost basis—hence if it does not sell its securities, the net earnings on its portfolio reflect only net interest income. However, the Fed does publish the unrealized capital gains and losses on its holdings on a quarterly basis. Unanticipated economic developments can lead to changes in the expected path of short-term interest rates, which will result in changes in both expected Fed income and the market value of the Fed’s securities holdings. However, the value of the Fed’s portfolio can also change as a result of expected movements in short-term interest rates that do not have implications for expected Fed income.

[3] The Fed’s portfolio was as large as it was in 2020 in part because the Fed had moved to an “ample reserves” policy implementation framework.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

What if the Federal Reserve books losses because of its quantitative easing?

June 1, 2022