Two billion adults in the world are excluded from credit. The situation is especially bad for small farmers in rural areas who are unable to access loans to invest in their farms, trapped in a vicious circle of low productivity, low yields, and poor income. The Initiative for Smallholder Finance estimates that smallholders globally access just $50 billion of the $200 billion of lending that they require to grow their operations and improve their lives.

The global growth of microfinance banks has created new opportunities for financial inclusion, with outstanding lending of $100 billion to around 200 million clients. Yet the majority of lending from microfinance institutions has been to urban populations and not to the rural poor or small farmers.

Farmers with access to finance can invest in fertilizers and seeds to increase their yields and incomes potentially by more than 25 percent.

There are well known reasons that make lending money to farmers so hard. Farmers are spread out across large thinly populated areas making them costly to reach and serve; they have few realizable assets to pledge as collateral against loans; and they generally have no financial history, which is needed for credit scoring. And on top of all that, agriculture is regarded as a risky business, often at the mercy of the weather. Yet farmers with access to finance can invest in fertilizers and seeds to increase their yields and incomes potentially by more than 25 percent.

New technologies have the potential to give farmers access to the financial tools necessary for such growth.

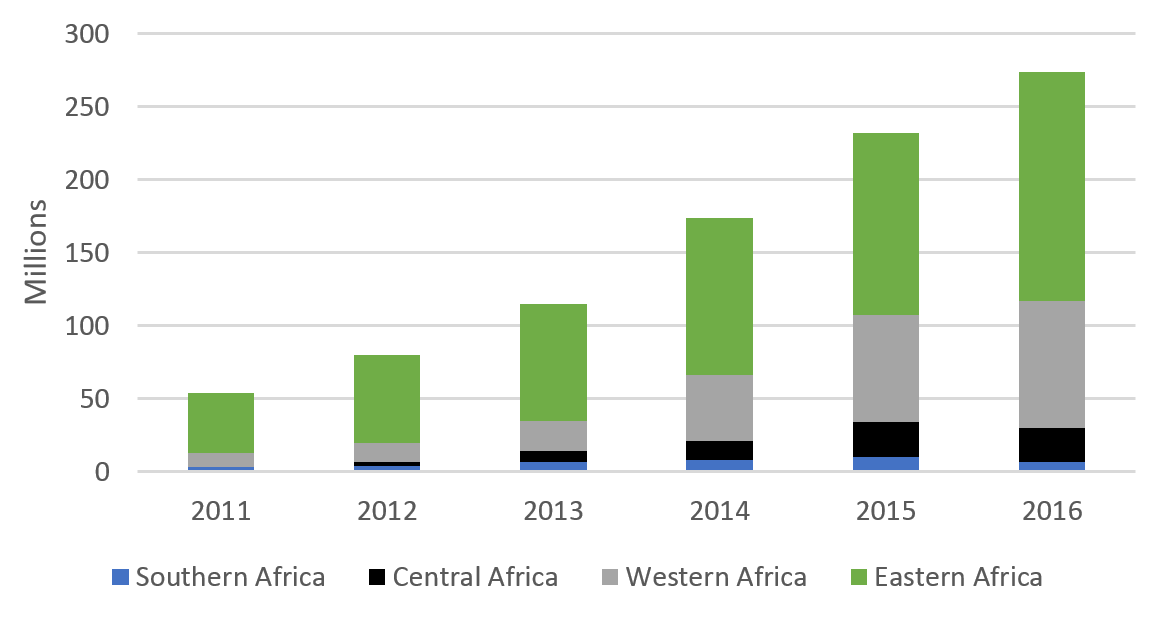

The rise of mobile phones in rural areas has been dramatic with over 90 percent of Africans able to access cellphone services, and many farmers now use cellphones to make calls, send text messages, and access data and informational services. The adoption of mobile money services has mirrored cellphone growth, allowing users to send and receive funds using a network of local agents.

Figure 1: The rapid rise of mobile money in Africa

Source: Chart adapted from “The Mobile Economy Sub-Saharan Africa 2017”

Big data analytics for credit risk assessment has been on the rise across urban areas of developing countries over the past years. Several startups offer loans to previously un-bankable customers using cellphone data (call data records, mobile money data, and social media data). This data is processed by algorithms, generating a predictive score of a person’s likelihood to repay a loan.

Crop suitability mapping enables lenders to understand how risky a farmers production is, based on where they are located (using geo-mapping techniques, lenders are able to ensure that they only lend to a farmer growing a suitable crop in a suitable location).

Can this new technology really make farmers bankable?

Imagine a poor farmer in Ghana that has been growing beans to sell into the local market. After providing for her family, she doesn’t have enough money left over to purchase high quality seeds or fertilizers, even though such inputs would increase the amount of beans she will grow. She tried borrowing from the local microfinance bank, but since she had never saved with them before, they are not willing to grant her a loan. Suddenly she receives a text message asking if she’d like to apply for a loan to pay for inputs. She clicks “yes,” and receives an automated message saying she has received the loan. The loan automatically goes into her mobile money account, and she visits the supply store to purchase seeds and fertilizers. Next harvest she produces 30 percent more beans than usual. After selling her crops she visits the local mobile money agent to repay the loan and interest. As a result, she is left with more money than normal, so she joins the local microfinance bank to open a savings account with the surplus funds. Now, she is an individual with a bank account opening further opportunities for her and her family.

The story above is not yet happening but is a distinct possibility and illustrates how technology can transform a farmer into a profitable borrower. While cellphone-based lending is starting to happen in Africa, with products such as MShwari in Kenya, this type of lending so far has been mainly for small, short-term loans for urban customers. Farmers who are less tech-savvy and need larger, longer-term loans repayable at the end of the season cannot benefit from existing mobile loan services. Yet by transforming the application process into a simple automated cellphone-based application, transaction costs plummet and remote farmers can access the service. By using cellphone records for credit scores, previously “un-scorable” customers are now ratable. Using agronomic geospatial data ensures that lending is only given to farmers growing the right crops in the right location. Migrating cash management to mobile money platforms dramatically reduces money disbursement and recovery costs. The mix of these technologies could grant access to seasonal lending to smallholder farmers.

Perhaps the nearest example of this technological convergence to date is Safaricom’s DigiFarm and Connected Farmer model in Kenya. The platform offers a range of services to farmers including e-vouchers for quality inputs at discounted prices; access to agriculture advice services via a training module; and advice on how to appropriately use inputs like seed and fertilizer. Digifarm also offers farmers the opportunity to apply, via their cellphones, for a loan to be used to purchase agricultural inputs, although data on total lending and repayment rates is not yet available. The loan module appears to build upon their proven success with the M-Shwari mobile microloan available to Sarfaricom customers.

If Digifarm and other similar services achieve success, we are likely to see many other mobile companies, banks, and startups replicate their models. Most exciting of all is the impact that this will have on farmers who will have increased opportunities to invest in their endeavors.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Using big data to link poor farmers to finance

May 3, 2018