Since the first iteration of the Global Findex survey in 2011, the share of adults in developing economies with a financial account has risen to 71%—an increase of more than 50 percentage points. While that growth is worth celebrating, the total numbers hide significant differences in how and why adults today in developing economies are accessing and using financial services.

From 2011 to 2017, financial inclusion efforts were driven by “scale,” as governments in large-population economies like India and China enacted policies specifically to increase account access. Between 2017 and 2021, however, global trends shifted toward broader “scope,” such that 34 developing economies of different sizes increased their share of adults with a financial account by more than 10 percentage points. Both scale and scope expansion of financial inclusion have been enabled by customer-facing digital technology—but the kind of technology making an impact and how it’s delivering results may not be what you think.

How does Findex assess the role of “digital technology” in financial inclusion?

A great deal of focus and excitement has pointed toward the digital-only services offered by non-bank financial entities such as mobile money providers or other financial technology firms (fintechs). Mobile money is a financial service offered by a telecom or a fintech firm that partners with mobile network operators, independent of the traditional banking network (this is different from traditional banking services accessed through a mobile phone). Mobile money services are typically enhanced by local mobile agents, where customers can conveniently deposit even small amounts of cash to make payments, pay bills, send remittances, or store money outside of the home. These actors are centrally important in the economies of sub-Saharan Africa, as well as in places like Bangladesh and Paraguay. Yet contrary to the amount of attention they get, they are not the only source driving growth in digital inclusion. They aren’t even the largest source.

The Global Findex captures the demand-side perspective on financial services digitalization in two ways. First, we ask adults about the accounts people have (whether they are with a traditional financial institution like a bank, or, as we’ve asked since 2014, with a mobile money provider). Then we ask about the services and transactions respondents use, distinguishing cash-based transactions from those executed through a computer, mobile device, or card-based payment network without cash changing hands. That holistic view allows us to highlight the relative impact of digital accounts as well as digital transactions, such as direct digital payments.

Mobile money accounts play a critical role in Sub-Saharan Africa and other countries

Ten percent of adults worldwide had a mobile money account in 2021, up from 4% in 2017. That rises to 13% of adults when we look only at mobile money account ownership in developing economies. A minority of those mobile money account holders (about one in four) only have a mobile money account. The rest have accounts with both a mobile money provider and a bank or similar financial institution, suggesting that the marginal impact of mobile money on access to financial services—while significant in certain economies—is minimal at global scale.

Mobile money provides a critical service in some economies. Regionally, Sub-Saharan Africa is the world leader in mobile money accounts, with 33% of adults in the region having one—just six percentage points fewer than the 39% of adults in the region with an account at a bank or similar financial institution. Mobile money adoption grew by 13 percentage points since 2017, a rate that mirrors the 13 percentage points of growth in regional ownership of any kind of financial account. In certain economies, such as in Benin, Cameroon, Ghana, and Malawi, adults even appear to be replacing their financial institution accounts with mobile money accounts: the share of adults with accounts of any kind rose in these economies between 2017 and 2021 as the percentage share represented by traditional brick and mortar accounts declined.

Outside of Sub-Saharan Africa, a few developing economies also have around 30% or higher mobile money account ownership. They include Argentina, Bangladesh, Brazil, Malaysia, Mongolia, Myanmar, Paraguay, the Russian Federation, Thailand, and Venezuela. But on average, less than 5% of adults in these countries have a mobile money account without also having an account at a bank or similar institution (the data does not allow us to ascertain how adults with both types of accounts differentially use them).

So, if mobile money has had a relatively small overall impact on financial access in developing economies, where is technology playing a larger role? With payments.

Globally, payments are the most-used financial service

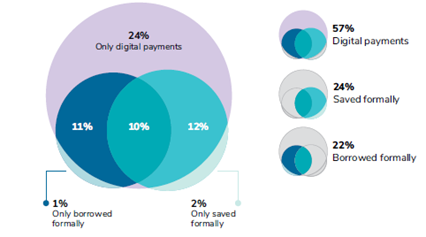

Figure 1: Adults using an account for financial services in developing economies (%), 2021

Thirty-nine percent of adults in developing economies opened their first financial account at a bank or similar financial institution (excluding mobile money accounts) for the express purpose of receiving a direct government payment (such as a wage, pension, or benefits payment) or a direct wage payment from a private-sector employer. In the large-population economies of China and India—the governments of which launched programs between 2014 and 2017 to drive financial inclusion—the share of first account opening to receive a direct payment is well above the average, at 49% and 54%, respectively.

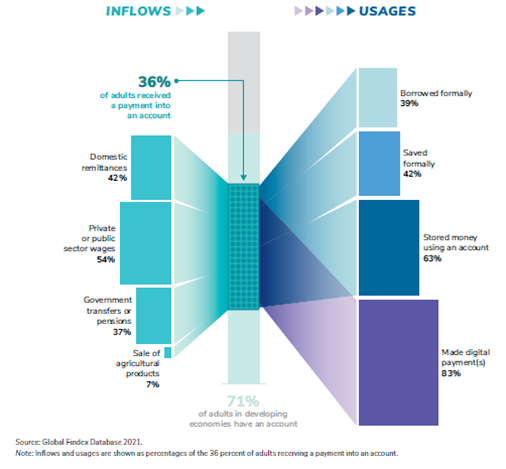

Moreover, 36% of adults in developing economies received at least one payment into their account in the 12 months prior to the Global Findex 2021 survey. Among them, 54% reported receiving a wage payment directly into their account, while 36% received a government support payment. In addition, 42% received a domestic remittance payment into their account, a better option than cash and money transfer operators because recipients can leave money in the account for safe-keeping or for savings. Digital payments made directly from a mobile phone are also often a cheaper and more convenient option for the urban poor to send money home to rural areas.

Direct payments from a government or employer are the biggest documented driver of account access—and are associated with more use of digital transactions

Receiving a direct payment is only part of the story. Another key part is making digital payments directly from an account using a card or phone. While previous iterations of the Global Findex found that payment recipients tended to simply cash out when they wanted to access their money, the 2021 survey finds that 83% of account-owning payment recipients now also make payments directly as well. Many of these payment products are offered by bank-fintech partnerships.

Together, these findings point to payment digitalization in developing economies as a major technological enabler of both financial access and usage. The benefits flow both ways: recipients get a more secure and convenient way to store and save their money, reduce transaction costs, and build up a financial history, and payers benefit by having an end-to-end digital payment trail that decreases costs and leakage.

Figure 2: In developing economies, adults who receive a payment into an account are more likely than the general population to also make digital payments and to save, store, and borrow money (%), 2021

Direct digital payments—whether by a traditional bank or a fintech—require a robust payments infrastructure

An overall message from the data is that payments sent directly into accounts are a driving force for expanding financial inclusion in developing economies.

But the successful digitalization of payments requires an enabling financial infrastructure that facilitates direct deposits and digital payments by all financial providers. This infrastructure includes interoperable payment networks, telecommunications infrastructure, and network security. It also includes data privacy and consumer protection regulations. These are the key enablers on which banks and fintechs will depend to expand their reach to increase financial access and usage in developing economies.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Technology’s impact on financial inclusion is not what you think

December 16, 2022