COVID-19 puts higher-ed finances at risk. For some universities, revenue shortfalls are going to be a pain—for other universities the shortfall may be a disaster. Public universities face three major sources of revenue risk: hospital revenues, tuition (both from overall enrollment and with special attention to enrollment of out-of-state students), and state funding. The bottom line here is going to be that the exposure of different schools to these risks is extremely variable. When it comes to the financial consequences of COVID-19, there’s no one-size-fits-all impact.

To get a picture of the financial landscape, I use publicly available IPEDS data that gives a snapshot of finances for most American universities. This has two implications: First, you can grab a useful report about any school you are interested in; second, the data is not nearly as good as the information institutions have internally. Because of the latter, we’ll look at overall patterns across universities—but not name names. Note that I am leaving out two-year schools, which have different patterns than four-year schools, and private schools, which use an entirely different set of accounting standards. Public institutions grant two-thirds of all bachelor’s degrees; my data covers institutions with about two-thirds of public university undergraduates.

In what follows, we look at the variability in university exposure to specific financial risks.

Hospital revenue risk

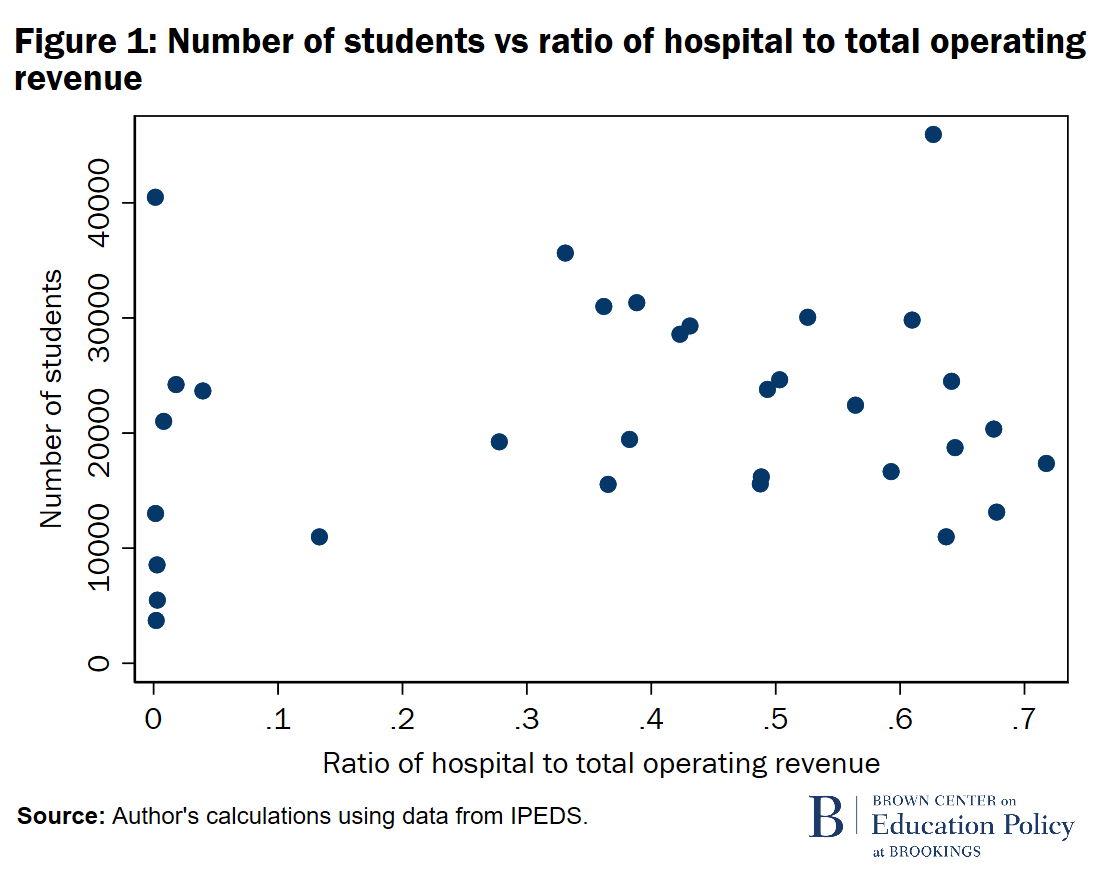

Hospital revenues fell dramatically as elective procedures ground to a halt. This matters for higher-ed finances because many of the country’s top hospitals are affiliated with universities. Hospitals churn through huge amounts of money; that doesn’t mean that they make a profit, but it does mean that hospitals are sometimes the big financial gorilla on campus. (In some universities, medical center finances are tied into overall finances; at other schools, the medical side finances are kept pretty segregated.) In aggregate, hospital revenues are about 15% of total college revenues. However, what’s really going on is that major medical centers are an enormous fraction of the budget at a few schools, while most public universities don’t have a hospital at all. Only 35 of the 491 schools for which I have data have hospitals, but the schools with hospitals are also relatively large—accounting for 10% of the students.

The graph below shows the number of students in those schools that do operate hospitals against the ratio of hospital to total operating revenue. On this graph—and on the graphs that follow—universities on the left are at relatively low risk while universities on the right are at high risk. From the horizontal axis, it’s clear that a major fraction of revenues comes from hospitals at these schools, generally over 40%. From the vertical axis, we learn that the schools with hospitals are large, generally with over 10,000 students. The bottom line is that hospital revenues are a concern only at a handful of schools—but those are big schools facing a potentially big problem.

Enrollment revenue risk

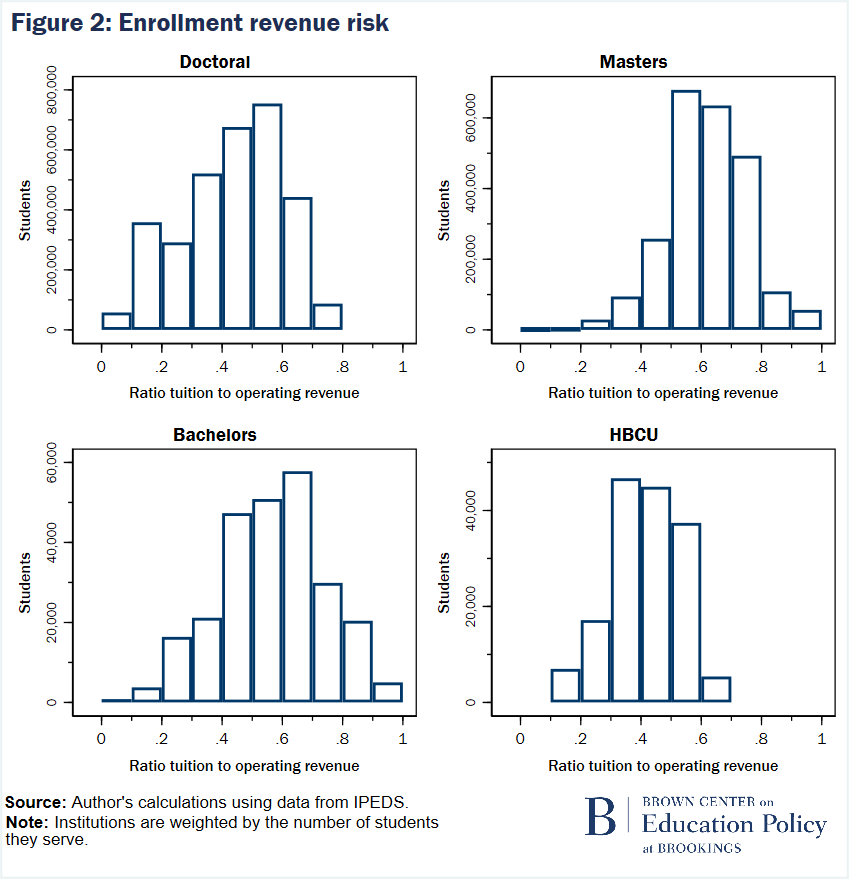

Right now, every university is worried about enrollment, both how many students decide to enroll now and whether there will be unusual “bleed” over the summer. How much of total operating revenue comes from tuition? It’s all over the map. Different kinds of universities face different risk profiles. To see this, we’ll separate universities according to the highest degree they offer (doctorate, master’s, bachelor’s). Because they are of special interest, I also look at historically Black colleges and universities (HBCUs).

At the big-picture level, tuition revenue is a very large chunk of total operating revenue; thus, a significant drop in enrollment would be quite bad. Bachelor’s-level and master’s-level universities are noticeably more exposed to enrollment risk than are doctoral-level universities. HBCUs are somewhat less exposed than bachelor’s- and master’s-level universities in general.

The real news, though, is that there is great heterogeneity in exposure within every category. There are doctoral-level universities with hardly any revenue from tuition (the ones underlying the bars to the left)—so they face little risk from enrollment fluctuations—and there are doctoral universities where operating revenue mostly comes from tuition dollars (the ones underlying the bars to the right). The same high level of heterogeneity is true for the other three university categories.

What the graph doesn’t show (because the federal government doesn’t collect the data) is the incredible heterogeneity within universities. For example, there are master’s programs in STEM and business that rely almost entirely on tuition revenue from international students. If international students don’t enroll—visa offices are still closed and the appeal of online courses under current circumstances is unknown—such programs may be at great risk. There are going to be some very interesting internal discussions inside universities about who’s subsidizing whom.

Out-of-state student enrollment revenue risk

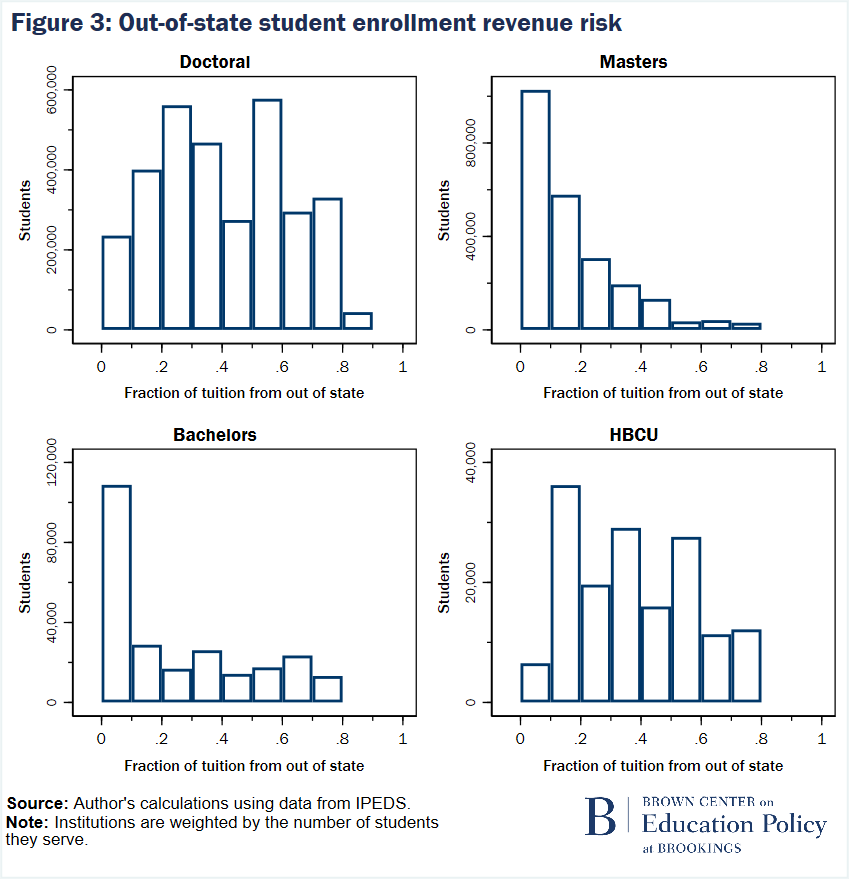

On top of worries about enrollments in general, many public universities are really, really worried about a drop-off in out-of-state students. There are two, maybe three, issues here. First, out-of-state tuition is generally higher (a lot higher) than in-state tuition. Out-of-state students subsidize in-state students; if they don’t come, there’s a special financial hit. Classes at many universities will remain online (at least partially) through the fall. For example, the largest state-university system, California State University, has said nearly all classes will be online. So, the second issue is that no one knows whether out-of-state students will be willing to pay premium tuition for online classes. Maybe they will, but no one knows. Finally, it’s starting to look like international students who are not already in the U.S. won’t be able to get here by fall. This might—or might not—mean a huge drop in the number of high-tuition-paying international students attending American universities.

The following chart gives the fraction of tuition that comes from out-of-state students, based on undergraduate tuition only. (And with a few behind-the-scenes assumptions, because the data isn’t perfect.)

Here too, there is enormous heterogeneity. Most of the students at bachelor’s-level institutions are at schools that are at most modestly dependent on out-of-state tuition. In contrast, many doctoral-level schools are very dependent on out-of-state tuition. (At some doctoral-level schools, the majority of students are from out of state.) Master’s-level schools are somewhere between bachelor’s- and doctoral-level schools in this respect. The HBCUs are rather like the doctoral-level schools. I suspect this reflects the fact that many doctoral schools and HBCUs are national draws, while others are less so.

State support risk

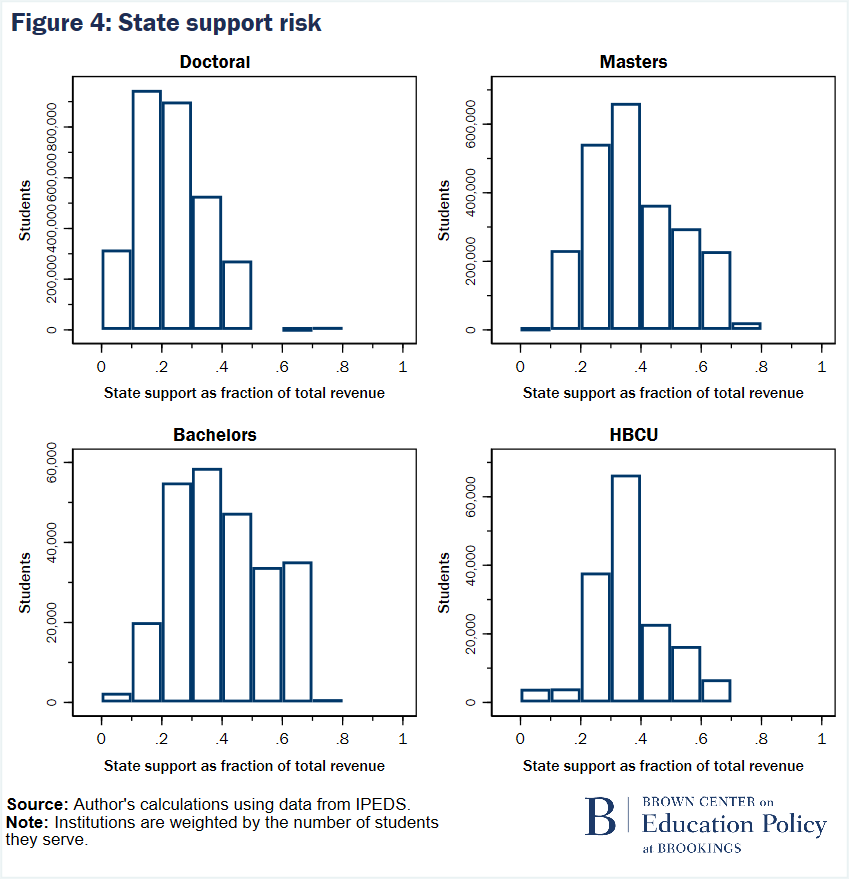

One reason some public universities rely so heavily on out-of-state students is that states made deep higher-education funding cuts in the wake of the Great Recession. Whether there will be even further cuts depends in part on what happens in the future with federal stimulus money, but universities are certainly anticipating there will be further serious cuts in state support. The next chart shows state support as a fraction of total revenues. (I’ve used total rather than operating revenues because states provide support for costs other than operations.)

When it comes to state support, doctoral universities are somewhat less vulnerable than other schools on average; although “somewhat less” is somewhat less than reassuring, since state support is still pretty important. And again, we see great heterogeneity within each class of school. Some schools can manage even with significant cuts in state support. Others will be out of business—literally.

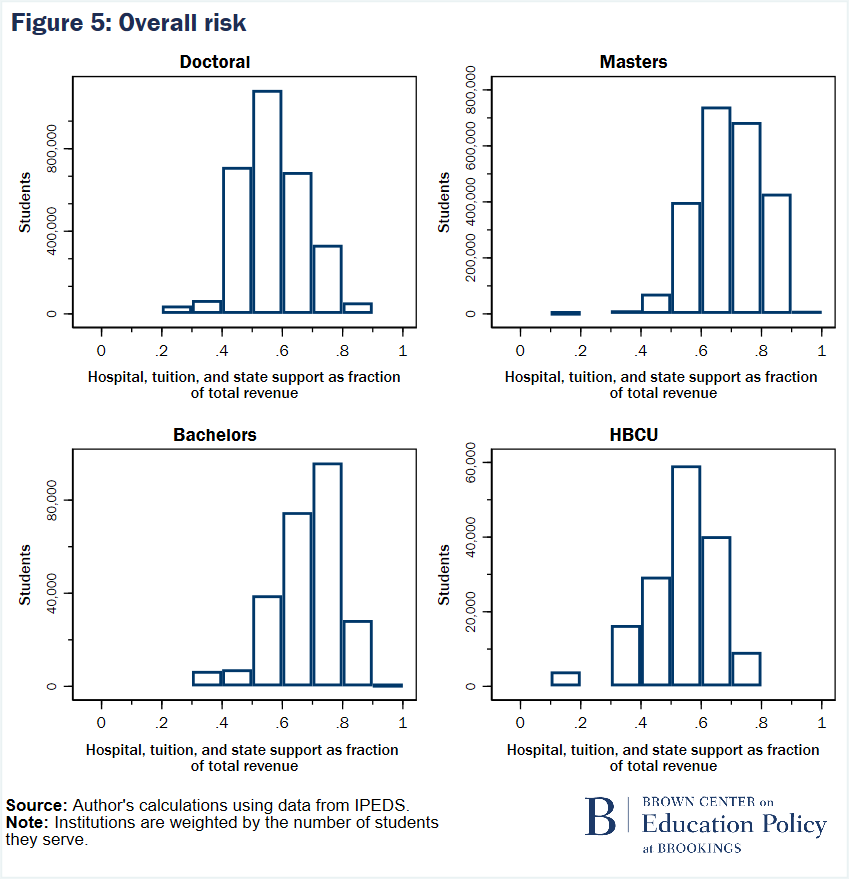

Risks overall

Are there universities where hospital revenue, tuition revenue, and state support—even taken together—don’t make up a large enough fraction of total revenue to put the institution at much risk? As the next chart shows, unfortunately no.

The overall picture suggests there are very few students whose universities do not face significant financial risk. Universities in the bachelor’s and master’s categories are even worse off than doctoral universities and the HBCUs. As the charts above show, the sources of risk do vary across categories: For example, bachelor’s- and master’s-level institutions are typically less vulnerable to drop offs in out-of-state students than are doctoral institutions and HBCUs, but bachelor’s and master’s-level universities face greater risk from overall enrollment declines and are somewhat greater risk from state budget cuts.

What’s the bottom line? In one sense, we don’t know. We don’t know the future course of the pandemic. We don’t know how adjusting instruction in the face of the pandemic will affect student enrollment. We don’t know where state budgets will land.

But there are two things we do know. First, nearly every school is at least at some risk of significant financial losses. Second, the risks are incredibly different at different schools. Many schools face difficulties. If things turn out really bad, some schools face closures.

I am grateful to UCSB undergraduate and Gretler Fellow Dylan Schmerer for research assistance and to my accounting colleague, Susan Grover, for explaining the intricacies of university financial reports.

Related Content

2020

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).