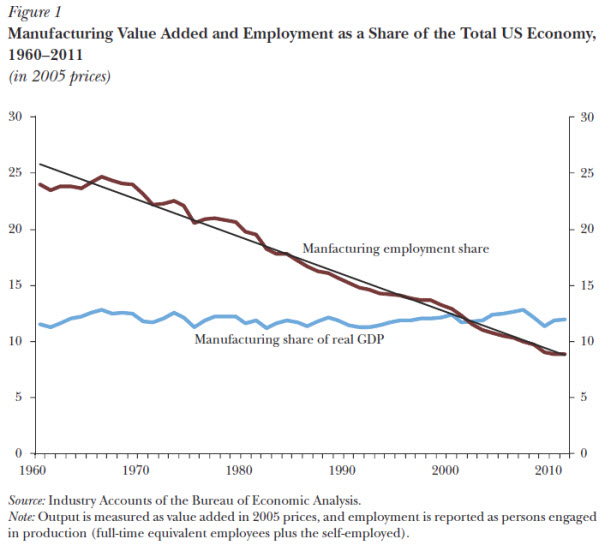

The development of the U.S. manufacturing sector over the last half-century displays two striking and somewhat contradictory features: 1) the growth of real output in the U.S. manufacturing sector, measured by real value added, has equaled or exceeded that of total GDP, keeping the manufacturing share of the economy constant in price-adjusted terms; and 2) there is a long-standing decline in the share of total employment attributable to manufacturing. These trends, going back several decades, are highlighted in Figure 1. Their persistence seems inconsistent with stories of a recent or sudden crisis in the U.S. manufacturing sector. After all, as recently as 2010, the United States had the world’s largest manufacturing sector measured by its valued-added and, while it has now been surpassed by China, the United States remains a very large manufacturer.

On the other hand, there are some potential causes for concern. First, though manufacturing’s output share of GDP has remained stable over 50 years, and manufacturing retains a reputation as a sector of rapid productivity improvements, this is largely due to the spectacular performance of one subsector of manufacturing: computers and electronics. Meanwhile, the 90 percent of manufacturing that lies outside the computer and electronics industry has seen its share of real GDP fall substantially, while its productivity growth has been fairly slow. Complicating the matter, the data on output and purchased inputs suffers special measurement issues, raising questions about whether real output and productivity growth are overstated.

Second, although manufacturing’s share of total US employment has declined steadily over the last 50 years (see Figure 1), recently there has been a large drop in the absolute level of manufacturing employment that many find alarming. After holding steady at about 17 million jobs through the 1990s, manufacturing payroll employment dropped by 5.7 million between 2000 and 2010. In large measure, the explanation lies with the equally striking decline of employment in the economy as a whole during the Great Recession and its aftermath, but the size of the absolute job loss deserves further examination.

Third, the U.S. manufacturing sector runs an enormous trade deficit that had already reached $316 billion by 2000, hit $542 billion in 2005, and remains very high despite the recession, equaling $460 billion in 2012; the manufacturing defifi cit is also very concentrated in trade with Asia, which represented over three-quarters of the defifi cit in 2000 and more than 100 percent in 2012. In 2000, only about one-third of the large defifi cit with Asia was accounted for by trade with China, but since then China has greatly increased its share, rising to 72 percent by 2012. The fall in manufacturing employment post-2000 has coincided with much of the growth in the bilateral trade imbalance with China, which suggests to some a causal link in which China trade is the reason for the loss of U.S. manufacturing jobs. (And it may cause a feeling of déjà vu for those who remember the debate over trade with Japan in the 1980s and 1990s.) However, economists also recognize that trade imbalances are largely a macroeconomic phenomenon, reflecting the gap between national saving and domestic investment, so linking the trade imbalance to the problems of U.S. manufacturing is more complex than blaming other countries.

In what follows, we examine each of these issues in greater depth and conclude with a discussion of the outlook for the future evolution of the manufacturing sector and its importance for the U.S. economy. While U.S. manufacturing remains an area of significant technological innovation, many of the largest U.S. corporations continue to shift their production facilities overseas. It is important to understand why the United States is not perceived to be an attractive base for their production.

Related Content

Related Books

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).