Spending, Taxes, and Deficits: A Book of Charts contains 132 pages of conventional-wisdom-defying insight into federal spending, taxes, budget deficits, and debt in 2026. This is the third in a series highlighting key myth-busting charts.

A deeper dive into basic government data from the Congressional Budget Office, Office of Management and Budget, and the Treasury Department reveals several uncomfortable truths.

One such truth: The federal debt path is likely much more perilous than is commonly reported.

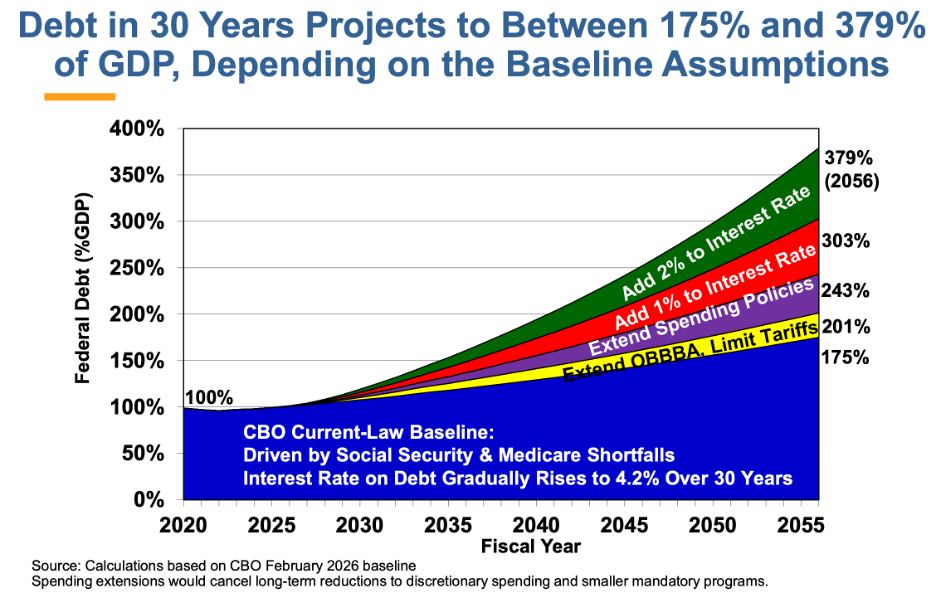

To be sure, the existence of rising government debt is widely acknowledged. Federal debt held by the public averaged around 40% of gross domestic product (GDP) from the end of World War II through 2008 but has since swelled to nearly 100%. The Congressional Budget Office (CBO) projects that debt will continue climbing to 175% of GDP over the next 30 years.

Such an exorbitant debt burden has been rarely seen among advanced economies and would surely strain the financial markets that would be expected to lend $138 trillion more to the federal government over three decades. At a 4% interest rate, that debt load would generate annual interest costs of roughly 7% of GDP, making interest the single largest federal expenditure. But this dire projection likely understates the true fiscal picture.

The CBO baseline rests on several current-law assumptions that are unlikely to hold

The CBO baseline includes tax changes and spending reductions that Congress has shown no appetite for:

- It assumes Congress will allow all temporary tax cuts to expire, including the new $40,000 cap on the state and local tax deduction.

- It projects that discretionary spending—which has not fallen below 6% of GDP since the 1940s—will drop all the way to 4.6% of GDP.

- It assumes that smaller mandatory programs such as the Supplemental Nutrition Assistance Program (SNAP), unemployment insurance, and student loans will shrink by nearly one-quarter as a share of the economy.

- It assumes that President Trump’s controversial tariffs will be renewed by every subsequent administration.

- And it assumes the government can borrow $138 trillion over 30 years without pushing interest rates above 4.2%.

This is a very optimistic scenario, one in which the likely largest government borrowing binge in world history leaves financial markets and interest rates mostly undisturbed.

More likely: future presidents and Congresses broadly maintain current policies (except Trump tariffs)

And then, the fiscal picture worsens considerably. As chart 59 shows, assuming that temporary tax cuts are made permanent—but that President Trump’s tariffs are not extended by the next administration—raises the debt projection from 175% to 201% of GDP by 2056.

If Congress also holds discretionary spending at 6% of GDP and does not allow smaller mandatory programs to significantly fall as a share of the economy, the projection climbs to 243% of GDP. This current-policy scenario (plus the Trump tariffs ending) is far more likely to materialize than the CBO current-law baseline.

Another variable worth adjusting: the interest rate on the debt

The federal government will be unlikely to maintain the CBO-projected payment of 4.2% interest on the debt as it rises to 175% of GDP since the resulting strain on financial markets would be untenable. Maintaining that 4.2% interest rate on a debt heading to 243% of GDP is even less likely.

A broad swath of economic research—most notably by Thomas Laubach of the Federal Reserve—suggests that each percentage point increase in the debt-to-GDP ratio raises long-term interest rates by roughly three basis points. Apply that rule of thumb to a 143-percentage point increase in the debt ratio—from roughly 100% today—and interest rates could rise by approximately 4.3 percentage points above the current 3.4%. Other factors may partially offset this upward pressure on rates, but the likely trajectory remains upward.

With debt levels set to soar, even modest interest rate movements carry enormous fiscal consequences. Each one percentage point increase in the rate paid on the federal debt would add roughly $57 trillion in interest costs over 30 years —approximately the cost of adding an entire additional Defense Department. In our current-policy projection, an interest rate topping out at 5.2% rather than 4.2% pushes the 30-year debt estimate from 243% to 303% of GDP. Adding another percentage point pushes it to 379% of GDP by 2056.

The resulting interest costs would be staggering. Pairing the 243% of GDP debt projection with CBO’s 4.2% interest rate assumption produces interest costs of 10% of GDP—which would consume 56% of all federal tax revenues annually by 2056. Pairing a 5.2% interest rate with the resulting 303% of GDP debt level produces interest costs of 15.8% of GDP, or nearly 90% of projected tax revenues.

At some point these projections become so extreme as to be economically unrealistic. Indeed, a 2023 analysis by the University of Pennsylvania’s Wharton School could not even model a functioning economy under the current debt trajectory—their models simply crashed.

Something has to give before that point. But the longer policymakers defer the debt reckoning, the more painful it is likely to be, exacerbated by the threat of sharply higher inflation and interest rates, a weakened economy, financial market instability, and ultimately, higher taxes and lower federal benefits for Americans. Better to start now with fiscal reforms and ultimately minimize the resulting economic pain.

For more insights into federal spending, taxes, deficits, and debt, check out Jessica Riedl’s 2026 federal budget chartbook.

Author

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The federal debt path is worse than reported

Federal debt projections may significantly understate the long-term fiscal risks facing the United States.

June 3, 2026