On June 22, 2020, President Trump issued an executive order (EO) restricting the entry of individuals seeking to enter the country on a nonimmigrant work visa. As part of this EO, the President proclaimed, “I have determined that the entry, through December 31, 2020, of certain aliens as immigrants and nonimmigrants would be detrimental to the interests of the United States.” Our ongoing research provides evidence to the contrary and documents that the EO negatively affected the market valuation of the largest U.S. firms.

According to estimates, this EO barred the entrance of nearly 200,000 foreign workers and their dependents. The nonimmigrant visas (such as the H-1B and L-1 visas) that were targeted are used by companies to hire or transfer high-skilled immigrants. There is overwhelming evidence documenting that skilled immigration improves firm outcomes such as profits, productivity, production expansion, innovation, and investment (see here and here for an overview of this evidence). Thus, it is plausible that the Trump administration’s measures significantly restraining immigration will have lasting negative impacts on American firms, and with it, slow down the post-COVID-19 economic recovery.

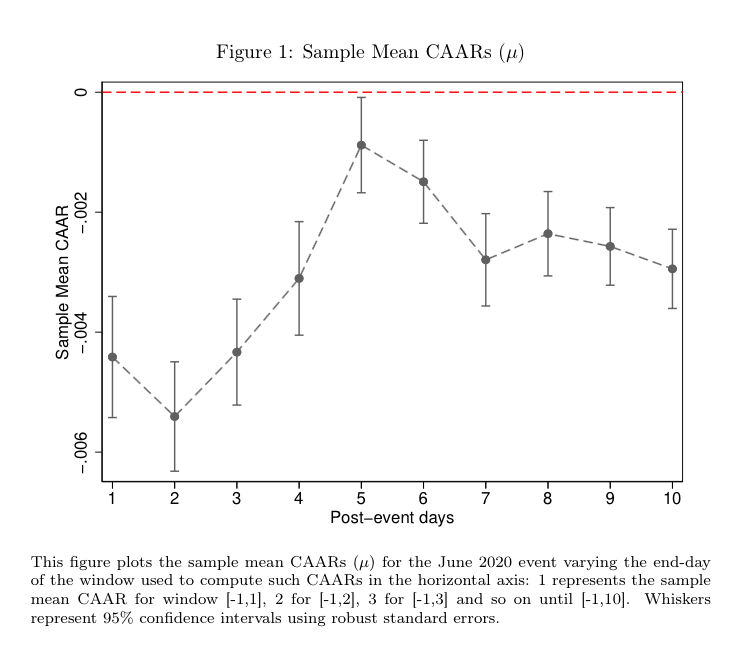

But we do not have to go very far into the future to assess the negative impacts of this policy. In fact, the largest U.S. firms have already taken a big hit, as we document in our most recent study. We estimate the cumulative average abnormal stock returns for Fortune 500 firms after the June 22 EO that restricted the skilled immigration visas on which Fortune 500 firms especially rely. This approach allows us to estimate the immediate economic impact of the aforementioned EO on the largest U.S. firms. We find that in the aftermath of the EO, the market valuation of the Fortune 500 companies in our sample dropped by about 0.45 percent, a loss to the economy as a whole that we estimate at around $100 billion based on the market valuation of the same firms a day before the EO. We further find that this negative shock was much more pronounced for firms that had maintained or increased their reliance on foreign workers during the years prior to the EO, as measured by growth in each firm’s Labor Condition Application requests (which proxies demand for H-1B visas).

Figure 1 summarizes said result. In the days after June 22, when the EO was announced, the abnormal stock returns for the firms in our sample dropped and remained down for 10 days after the announcement, which suggests this was a persistent effect.

Figure 1. Firms’ cumulative average abnormal returns (CAARs) after executive order announcement

The sizable negative effect on the economy reflects the fact that investors—and markets more generally—understand that many of these firms will not be able to perform as well without the ability to hire top foreign talent, directly affecting the firms’ overall valuation, which in turn affects the recovery prospects of the economy as a whole. If the EO—and other recent policies that curtail visas for skilled foreign workers—stays in place, there is robust evidence suggesting that in the next few years, these firms, instead of hiring US-born workers as the policies intended, will likely offshore many of their activities to other nations. In other words, in the short run, the EO caused a loss of $100 billion in market valuation. In the long run, it could cause even more damage to the U.S. economy as firms react to these constraints by shifting employment and investment abroad.

We hope our study can inform the policy debate on the importance of designing policies that allow the U.S. economy to continue to grow by complementing American workers with talent from abroad, a formula that has always been an engine of growth for the economy. Our results are yet another piece of evidence that policies restricting immigration to the U.S. (from refugees and fundamental workers to students to highly qualified individuals) are harmful to the country and are the opposite of what is needed to achieve a full economic recovery in the aftermath of the global pandemic.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The day that America lost $100 billion because of an immigration visa ban

October 20, 2020