The economic activity of the U.S. has plummeted in the wake of the coronavirus pandemic and unemployment has soared—largely the result of social distancing policies designed to slow the spread of the virus. The depth and speed of the decline will rival that of the Great Depression. But will the aftermath be as painful? Or will the economy swiftly recover once the pandemic has passed? And when will that be?

Analysts are using shorthand when discussing the shape of the recovery: Z-shaped, V-shaped, U-shaped, W-shaped, L-shaped, and even the Nike Swoosh. We explain what these mean, and which one of these appears most likely. But first, let’s talk about the downturn itself.

What are the immediate effects of the virus on economic activity?

According to the most recent Bureau of Economic Analysis estimate, the level of real (inflation-adjusted) GDP in the first quarter was 1.2 percent below the fourth-quarter level, and analysts expect GDP to drop another 8.5 percent to 11 percent in the second quarter. At annualized rates—the way changes in GDP are reported—these translate into a decline of 4.8 percent in the first quarter and 30 percent to 40 percent in the second quarter. (Annualized rates show what would happen to the level of GDP if the quarterly rate of growth persisted over an entire year.) To put these numbers in context, the largest quarterly GDP decline observed during the Great Recession was 8.4 percent at an annual rate in the fourth quarter of 2008.

What could the recovery look like?

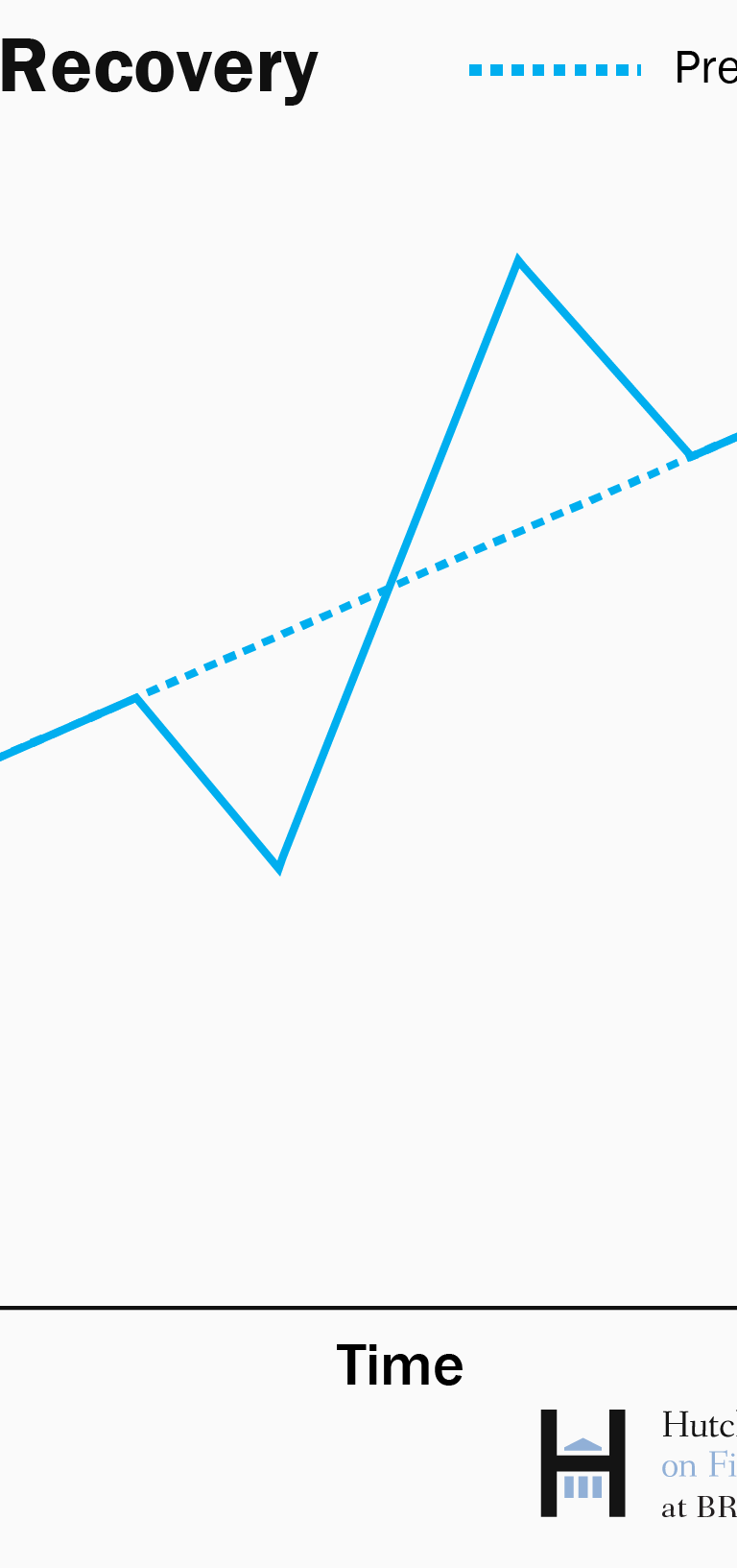

Most optimistic: The Z

The economy suffers a downturn during the pandemic, but then bounces back up above the level it would have been in a pre-pandemic baseline, as pent-up demand creates a temporary boom. In this scenario, a good part of the GDP foregone during lockdowns—the shopping we didn’t do, the restaurant meals we didn’t enjoy, trips we didn’t take—was simply delayed, and is made up once the risk from the pandemic passes.

Still very optimistic: The V

The economy permanently loses the production that would have occurred absent the pandemic, but very quickly returns to its pre-pandemic baseline once social distancing is lifted. Trips not taken, restaurant meals not purchased, and concerts not attended are forgone, rather than delayed, but once life returns to normal, everything is just as it would have been before.

Somewhat pessimistic, and probably more likely: The U or the Nike Swoosh

The effects of the pandemic on economic activity last well beyond the end of the social distancing, and GDP recovers slowly. Even after the health risks recede, the economy still doesn’t quickly go back to where it would have been, though it does get there eventually.

This basic story has many possible shapes. In the U-shape, the level of GDP stays low for a while (perhaps because social distancing norms last a long time), but then recovers back to baseline slowly.

In the Swoosh, borrowed from Nike’s logo, the economy starts to bounce back sharply, as restrictions are lifted and economic activity increases, but consumers, businesses, and state and local governments are still hesitant to spend, and it takes a long while for the economy to get back to pre-pandemic trajectory.

Also possible: The W

If the response to the pandemic is a first round of openings that is followed by a surge in COVID-19 cases and another round of closures in the fall, the recovery could be W-shaped.

But then the question will be, what does the recovery from the second (or third, if we do that multiple times) downturn look like?

Most pessimistic: The L

The pandemic has a permanent effect on GDP. Lost investment during the crisis, a rethinking of global value chains, a permanent change to fiscal policy, and a slowdown in productivity growth all have the potential to cause the trajectory of GDP to be lower than it otherwise would. This is basically what the recovery from the Great Recession looked like. (Despite the fiscal stimulus of the American Recovery and Reinvestment Act of 2009 and all the efforts of the Federal Reserve, it took six years for per capita GDP to return to 2007 levels, and real GDP is still well below pre-recession projections.)

What will determine the shape of the recovery?

At the beginning of the pandemic, few understood how long it would be before life returned to normal, and many analysts talked of V-shaped recoveries. Many analysts now believe that, barring major improvements in COVID treatment (which would make the disease less dangerous), only a vaccine can allow economic activity to return to the pre-pandemic baseline. Even once the economy starts to reopen, measures will likely be put in place that curtail economic activity to some degree—travel will be less common, businesses will have to space workers and customers further apart, restaurants will be serving fewer customers at a time, and sporting events, concerts, and other activities involving large crowds probably will remain off limits for a long time. And even if the rules allow, many people may be reluctant to return to life as it was before the pandemic.

So, there will likely be no quick recovery. A key question is whether damage to the economy’s capacity to produce goods and services will be long lasting.

That damage comes in four broad categories:

Household ability and willingness to spend: When workers lose their jobs, they are likely to drain savings and increase borrowing. They may delay payments on mortgages and credit cards, and their credit ratings may decline. And they may become more fearful about the future. That means that—even once the economy opens up again—they may be unable or unwilling to spend as readily as they did before the virus appeared.

State and local government finances: State and local governments generally have to balance their budgets each year. As income and sales tax revenues plummet, and demand for Medicaid and other programs increases, these governments will have to cut spending—mostly by cutting employment—or raise taxes. It took 10 years for state and local employment to rebound to pre-recession levels after the Great Recession.

Businesses—bankruptcies and lower investment: It takes a lot of work to open a new business. You have to arrange financing, find a location and suppliers, hire workers, etc. If a business declares bankruptcy and shuts down during the pandemic, that whole process will have to begin anew. That will take time and money, and make the recovery slower. In addition, even once the economy reopens, firms may be fearful that it will close again—either from a resurgence of corona or from a new virus—and may be less likely to invest in equipment or research and development. This decline in investment could make the firms less productive than they would have been, also holding down GDP.

Lost human capital: The relationship between workers and firms is valuable. Employers and workers typically spend a lot of time in finding a good “match,” and workers then acquire firm-specific skills and knowledge. If businesses lay off their workers during the lockdowns, those workers might start looking for other jobs, or they may leave the labor market altogether. That means that all that human capital will be lost. Once firms can reopen, they may have to start the process of finding and training workers again. This will also slow the recovery.

What can policy do?

The goal of public policy in the pandemic should be first to protect public health—investing in personal protective equipment for health care workers, greatly ramping up testing and tracing, and doing everything possible to speed up the development and production of vaccines. Not only will this save lives, but it will also create the conditions that will allow the recovery to begin.

Apart from these measures, the government can do a lot to ensure that the recovery is as “Z-shaped” as possible. Many measures have already been taken, including $660 billion in forgivable loans to small businesses, $300 billion in recovery rebate checks to households ($1200 a person for most adults, and $500 for most children), and $268 billion in increased and expanded unemployment insurance ($600 extra per week, and expansion of eligibility to gig workers and the self-employed). These measures will help keep finances of many—though not all—households and businesses in reasonably good shape.

As of the beginning of May 2020, there are two steps Congress has yet to take.

First, the federal government hasn’t provided nearly enough money to state and local governments to offset the lost revenues and added spending that are the result of the coronavirus. Such assistance would prevent them from cutting public services to balance their budgets and also would increase the odds of a robust recovery—more U-shaped than L-shaped.

Second, measures taken thus far to aid individuals were temporary. The $1200 per adult checks were just one-time, the $600 per week increase in unemployment benefits expires at the end of July, and the forgivable loans to small businesses are designed to cover eight weeks of payrolls. If, as seems likely, the economy is not back to normal by the late summer, more relief will be necessary to reduce the odds that the recovery will be L-shaped.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

The ABCs of the post-COVID economic recovery

May 4, 2020