This paper is part of the fall 2020 edition of the Brookings Papers on Economic Activity, the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. Research findings are presented in a clear and accessible style to maximize their impact on economic understanding and policymaking. The editors are Brookings Nonresident Senior Fellow and Northwestern University Professor of Economics Janice Eberly and Brookings Nonresident Senior Fellow and Harvard University Professor of Economics James Stock. Read summaries of all the papers from the journal here.

An economic model that incorporates the outsized role of temporary furloughs in the COVID-19 recession predicts a faster job market recovery than many other projections, according to a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on September 24.

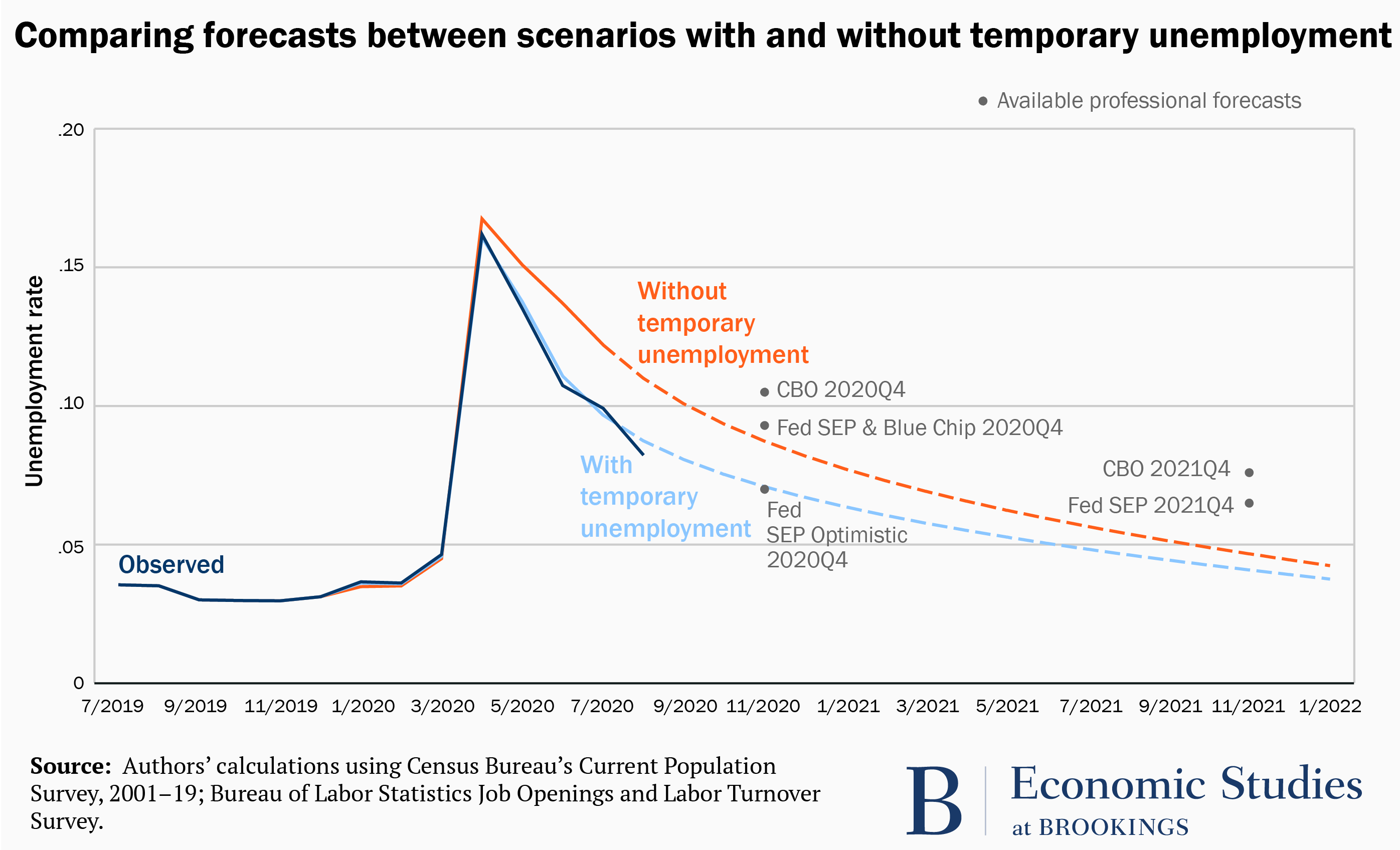

The paper—by Jessica Gallant and Kory Kroft of the University of Toronto, Fabian Lange of McGill University, and Matthew J. Notowidigdo of the University of Chicago Booth School of Business—suggests the unemployment rate will average 7.1 percent during the last three months of this year, down from 8.4 percent in August. That is still much higher than the 50-year low of 3.5 percent in February but much lower than the record high 14.7 percent in April.

In contrast, economists surveyed by the Wall Street Journal forecast an 8.1 percent rate in December 2020 and the median projection of Federal Reserve policymakers for the fourth quarter is 7.6 percent.

The authors, in Temporary unemployment and labor market dynamics during the COVID-19 recession, argue that labor market congestion—the difficulty or ease that actively searching unemployed workers experience in finding new jobs—wasn’t as bad earlier this year as suggested by headline unemployment rates alone.

They used their model to adjust the Beveridge curve (the relationship between the unemployment rate and job vacancies) for the fact that a much higher proportion of unemployment is temporary than in past recessions and found it to be similar to the curve in 2015, when the labor market was thought to be tight.

“The temporary unemployed who are waiting to be recalled do not affect the tightness of the labor market in the same way as those who have been permanently separated and are actively searching for work,” they write.

“The temporary unemployed who are waiting to be recalled do not affect the tightness of the labor market in the same way as those who have been permanently separated and are actively searching for work,” they write.

Most unemployed workers early in the pandemic believed their layoffs would be temporary (nearly 80 percent in April compared with 20 percent typically). By July, around 60 percent of the unemployed still believed their layoffs were temporary.

“According to our model, jobs are not ‘scarce’ for the relatively small share of unemployed workers who are actually searching for a job,” the authors write. For instance, only 24 percent of workers surveyed by the Conference Board in June reported that jobs were “hard to get.”

The authors say their model, combined with standard labor market measures, provides a relatively complete picture of the labor market’s health and should be useful to policymakers as they debate stimulus policies such as the Paycheck Protection Program (PPP) and the $600 a week unemployment insurance supplement.

Notowidigdo, in an interview with Brookings, said the PPP, which provided forgivable loans until it ended August 8, helped small businesses remain open and retain or recall employees. Supplemental unemployment insurance benefits, which ended after July, likely allowed many of the unemployed to wait to return to their old jobs rather than search for new ones, he said.

David Skidmore authored the summary language for this paper. Becca Portman assisted with data visualization.

CITATION

Gallant, Jessica, Kory Kroft, Fabian Lange, and Matthew J. Notowidigdo. 2020. “Temporary Unemployment and Labor Market Dynamics During the COVID-19 Recession.” Brookings Papers on Economic Activity, Fall, 167-226.

CONFLICT OF INTEREST DISCLOSURE

The authors did not receive financial support from any firm or person for this article or from any firm or person with a financial or political interest in this paper. They are currently not officers, directors, or board members of any organization with an interest in this paper.

Authors

Discussants

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).