Recent federal legislation—namely, the Infrastructure Investment and Jobs Act, CHIPS and Science Act, and Inflation Reduction Act—was enacted to incentivize investments in several sectors deemed important for America’s future economic growth and national security. Coinciding with the passage of this legislation, the United States is experiencing a $525 billion private investment surge in “strategic sectors,” which we define as clean energy, semiconductors and electronics, biomanufacturing, and other advanced industries.

One notable aspect of the many programs these laws fund is their inclusion of special incentives targeted to local economies that can benefit most from new industries, jobs, and economic opportunity. However, there has not yet been a full analysis of the geographic distribution of private sector investment to understand the extent to which distressed communities are benefiting from this place-based industrial strategy.

To fill this gap, this report compares the flow of strategic sector investments in distressed counties to their share of national economic activity, population, and overall private investment levels. We find that economically distressed counties are receiving a disproportionate share of private sector investment in these strategic sectors relative to their economic output and population. We also find that strategic sector investment patterns are distinctive: When compared to private investment writ large, these investments are more likely to go to distressed communities. This pattern of strategic sector investment marks a notable departure from economic growth and private investment trends in the 2010-2020 period.

Finally, we analyze commonalities across distressed communities receiving strategic sector investment, with the aim of informing how policymakers and practitioners can improve economic development outcomes in the implementation of these policies.

Employment-distressed counties have secured a disproportionate share of strategic sector investments

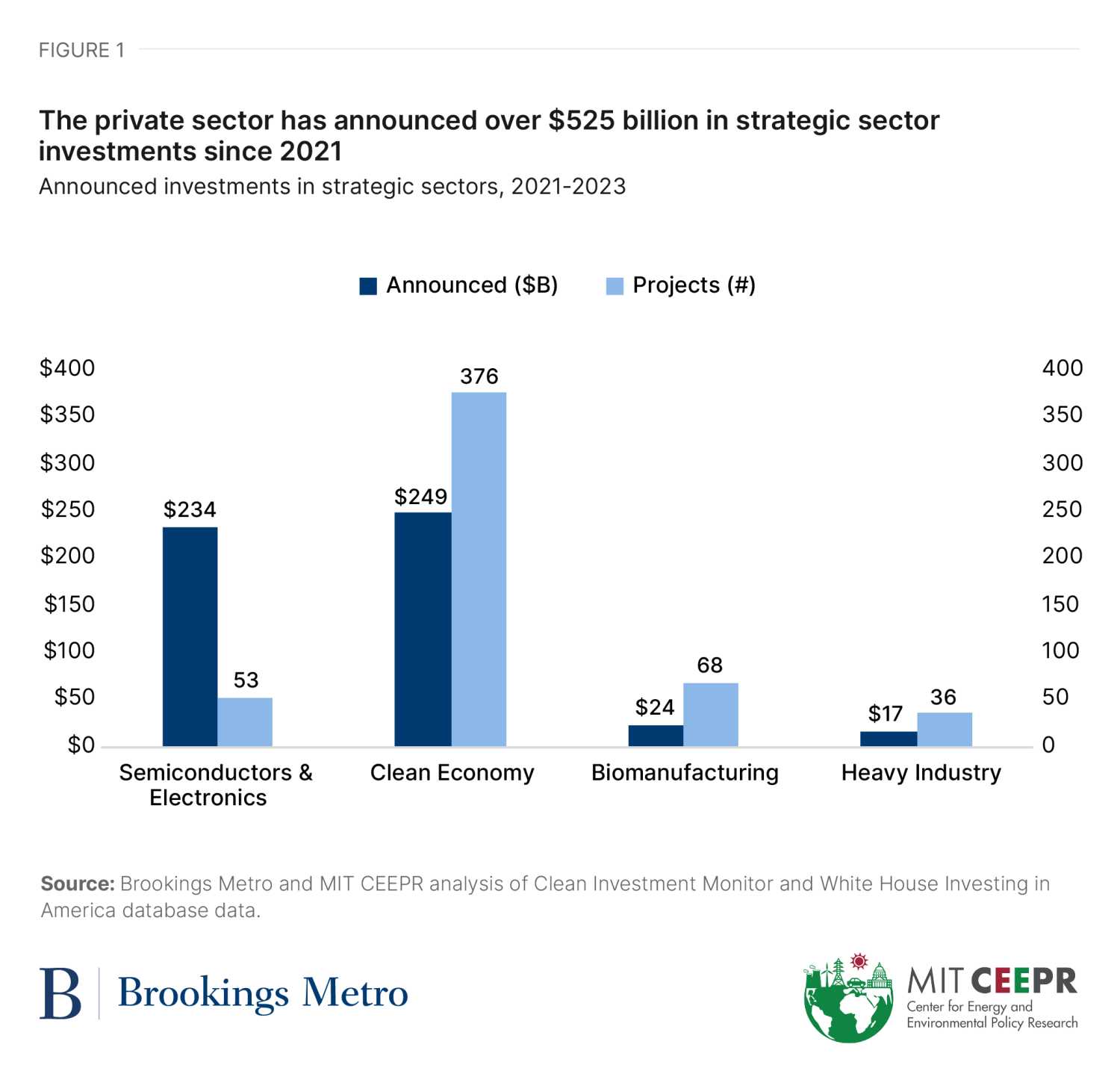

The United States is experiencing a surge in private investment in “strategic sectors,” which we define as clean technology, semiconductors and electronics, biomanufacturing, and other advanced industries. Since 2021, private investors have announced $525 billion in strategic sector investments, as tracked by two sources: 1) the MIT-Rhodium Group’s Clean Investment Monitor for clean technology investment; and 2) the White House’s Investing in America inventory for microelectronics and advanced manufacturing investments. For more on our data sources and methods, see the appendix.

How and where these capital investments land in local communities will largely determine whether strategic sectors can deliver economic benefits to a broad swath of the country. And indeed, many of the public incentives and investments within the three pieces of industrial strategy legislation seek to push private investment into local areas that are economically distressed. For example, Inflation Reduction Act (IRA) tax credits include bonuses of at least 10% when the investment is located in a low-income or energy community. The IRA Environmental and Climate Justice Block Grants program’s $3 billion in funding is only available for grant recipients who are or partner with a community-based organization. And the Department of Energy’s new Energy Infrastructure Reinvestment Financing program particularly benefits energy communities with loan guarantees to projects that repurpose or replace energy infrastructure that has ceased operations, as well as projects that reduce the greenhouse gas emissions of energy infrastructure in operation.

There are several ways to define economic distress. Following the definition used by the Economic Development Administration for its Recompete Pilot Program, we classify counties as “distressed” if they have a prime-age employment gap1 above 5% and a median household income below $75,000.2

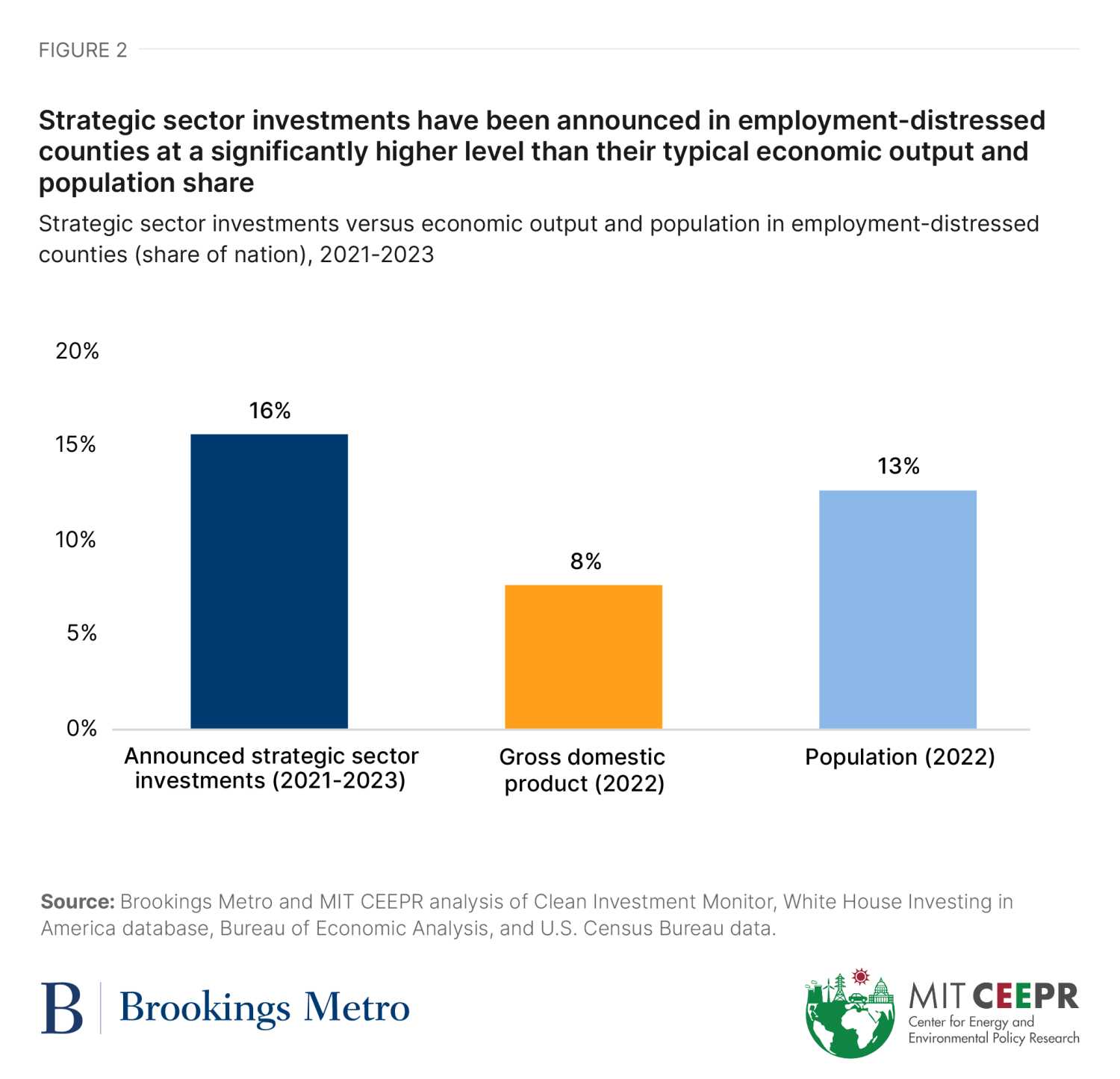

As of 2022, the nation’s 1,071 employment-distressed counties represented 8% of national GDP and 13% of the U.S. population. Since 2021, these counties received nearly $82 billion (or 16%) of announced strategic sector investments—double that of their GDP share and 1.2 times their population share.

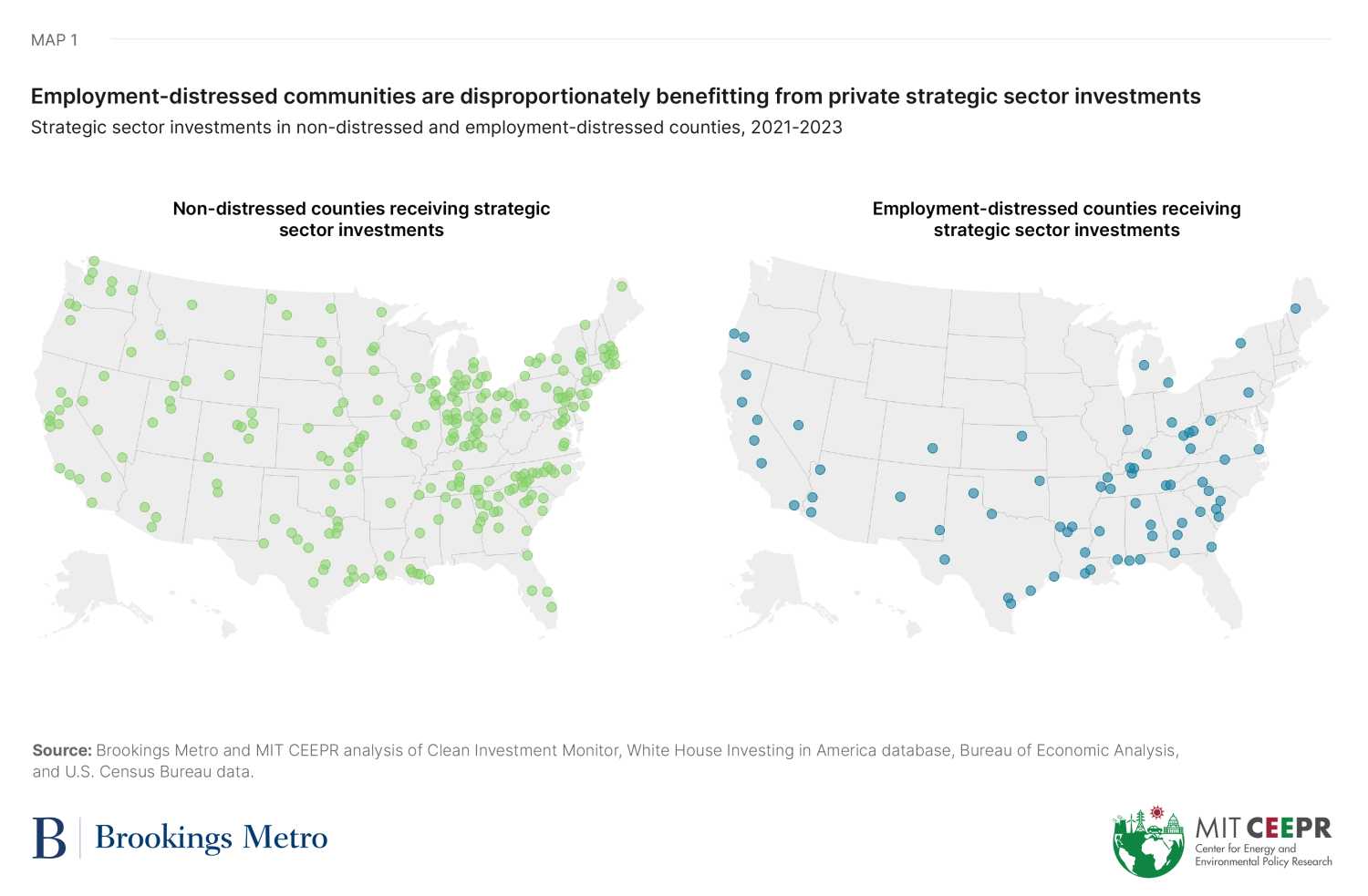

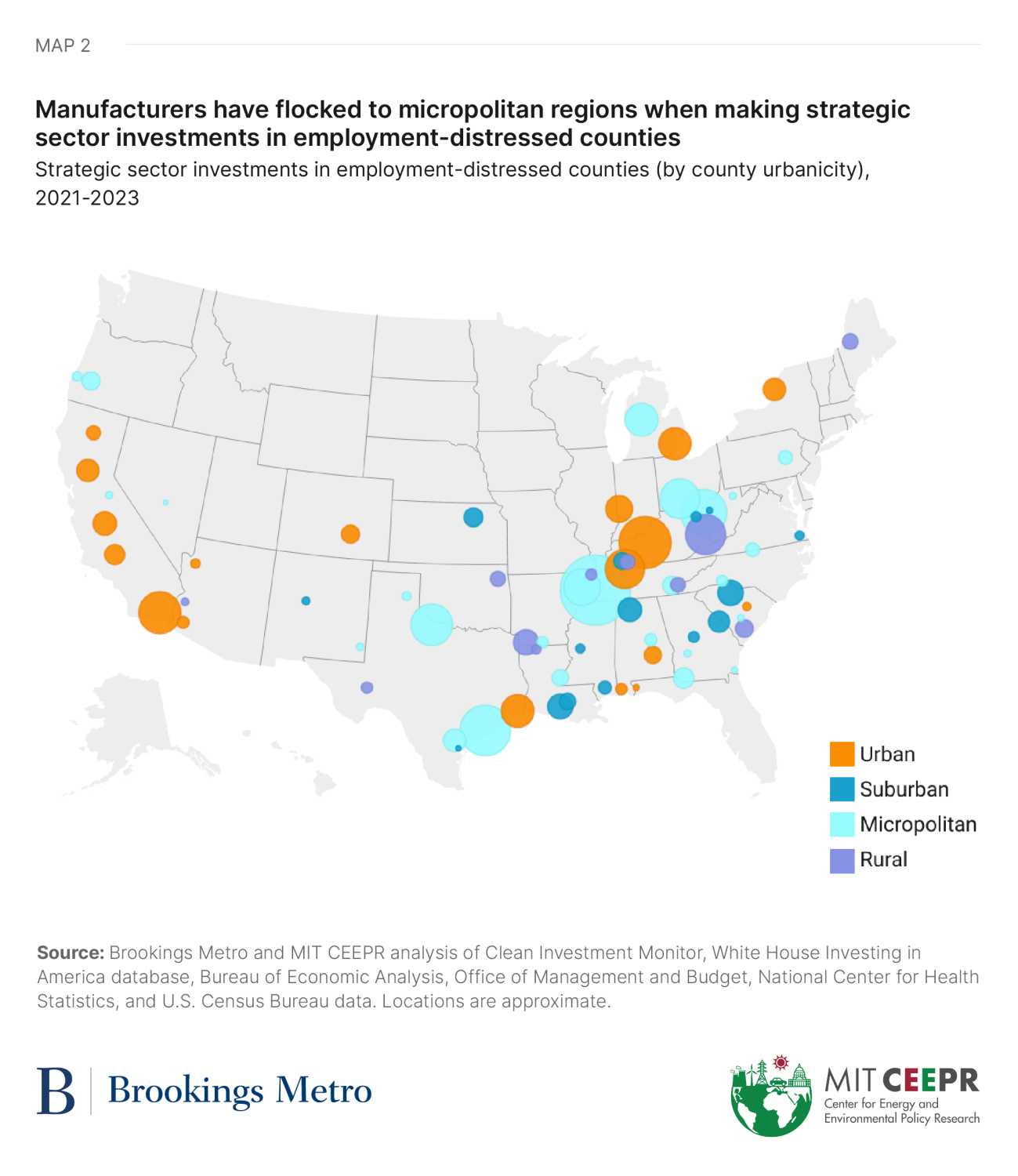

These announced strategic sector investments have flowed to 70 employment-distressed counties in 27 states and across over 100 projects. As Figure 3 shows, the employment-distressed counties receiving strategic sector investments are disproportionately concentrated in southern states, though they extend to the West, Northeast, and Midwest as well. The projects include AES and Air Products’ plans to invest over $4 billion in Wilbarger County, Texas to build a new mega-scale green hydrogen plant anticipated to create 115 permanent jobs and more than 1,300 construction jobs. Similarly, Chester County, S.C. is the chosen location for Albemarle’s $1.3 billion investment to build a “mega-flex” lithium processing facility, which is expected to create at least 300 new jobs.

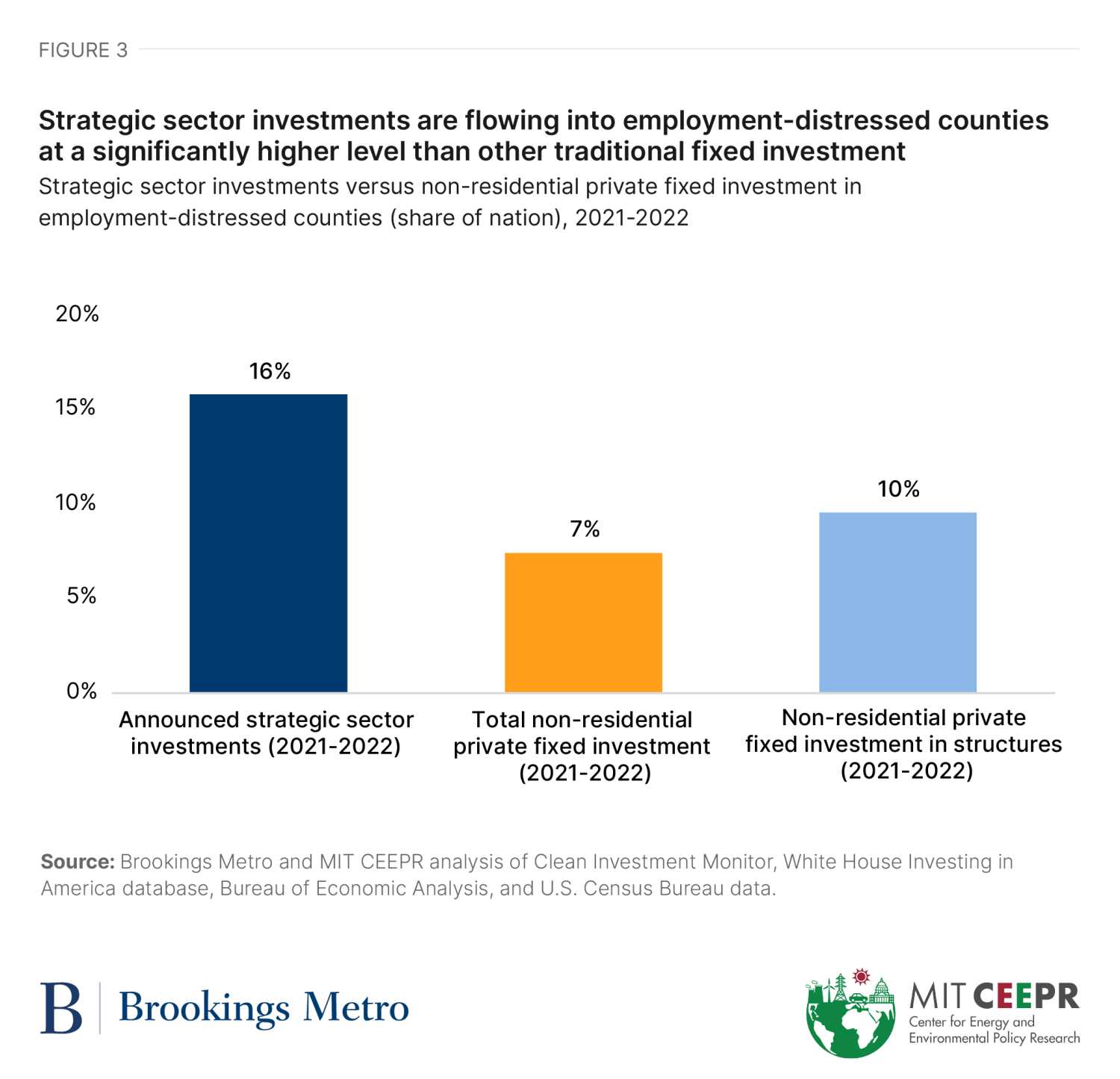

Comparing strategic sector investments with overall investment patterns suggests this distribution is distinct from private investment writ large. Employment-distressed communities have received a far greater share of strategic investment dollars than overall non-residential private fixed investment (PFI). Due to larger year-to-year differences in PFI, we compare 2021-2022 strategic sector investments against 2021-2022 total non-residential PFI and PFI in structures (e.g., newly constructed facilities, commercial properties, and other supportive infrastructure) to provide a direct comparison.

Employment-distressed counties represented 7% of total non-residential PFI and 10% of PFI in structures in 2021-2022, and received 16% of strategic sector investments in that time frame. This means strategic sector investments are flowing to employment-distressed counties at levels 2.1 and 1.7 times that of total non-residential PFI and PFI in structures, respectively.

This trend also represents a departure from the geographic pattern of PFI during the decade between the Great Recession and the COVID-19 recession. On average, distressed counties received 8% of total non-residential PFI and 12% of PFI in structures while producing 7% of national GDP during the previous recovery (2010 to 2020).3 During the COVID-19 economic recovery (2021 to 2022), these counties received 16% of strategic sector investments—two and 1.3 times the previous recovery’s share of non-residential PFI and PFI in structures, respectively, and 2.3 times their level of GDP.

Employment-distressed communities received an even higher share of actual investment in clean technology

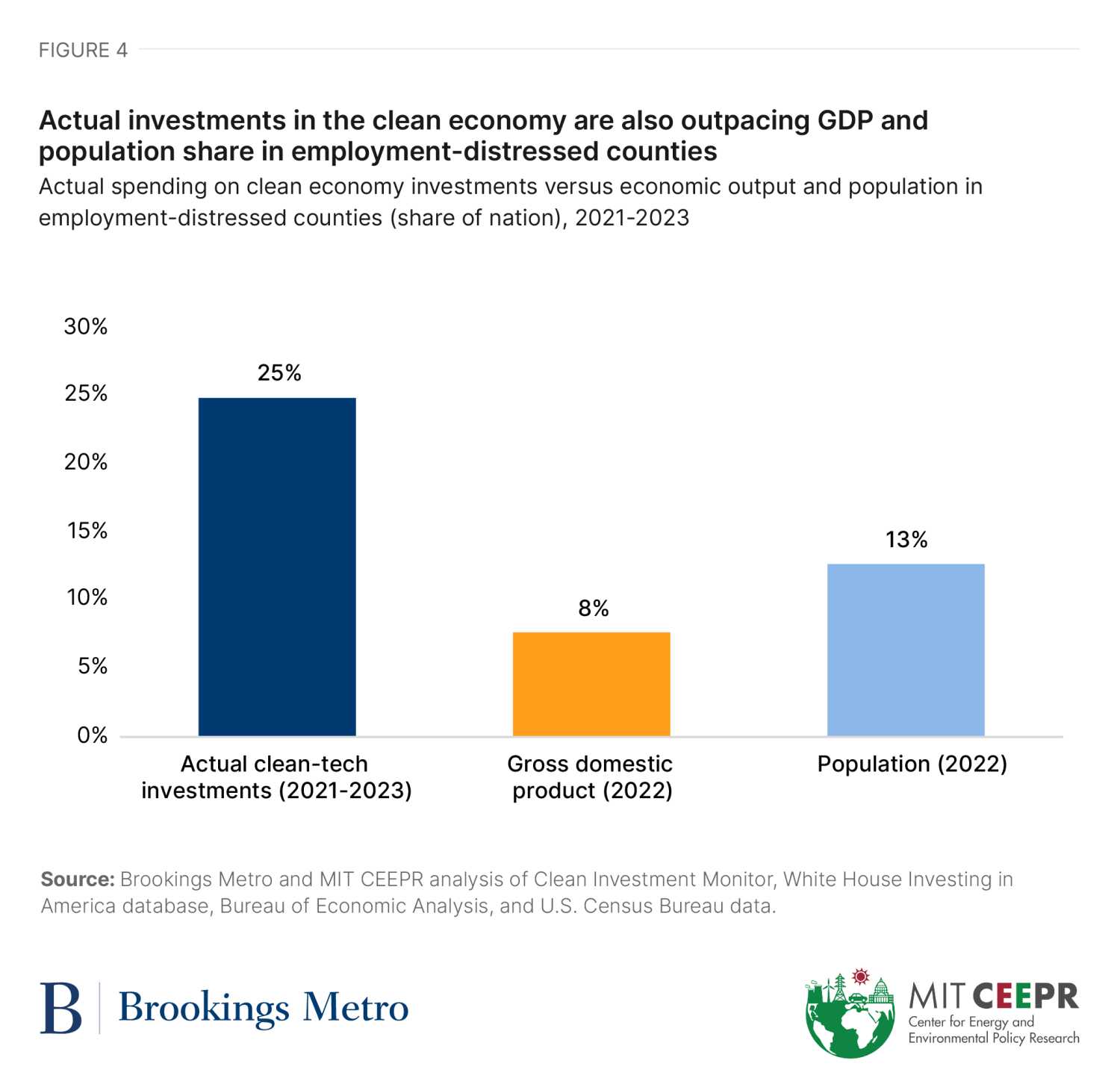

The previous finding tracks announced investments, which serves as a useful leading indicator, but is subject to the risk that actual investments do not materialize. Data from the Clean Investment Monitor reveals that actual clean technology investments extend the trends of announced investments across strategic sectors, with employment-distressed communities receiving an even greater share of actual clean-tech investments made thus far.

Since 2021, $26.6 billion of clean-tech investments have translated into real spending. One in four of these dollars ($6.6 billion) has reached employment-distressed communities, compared to 16% of overall strategic sector investments. Employment-distressed communities received actual clean-tech investment at 3.2 and two times their GDP and population levels, respectively.

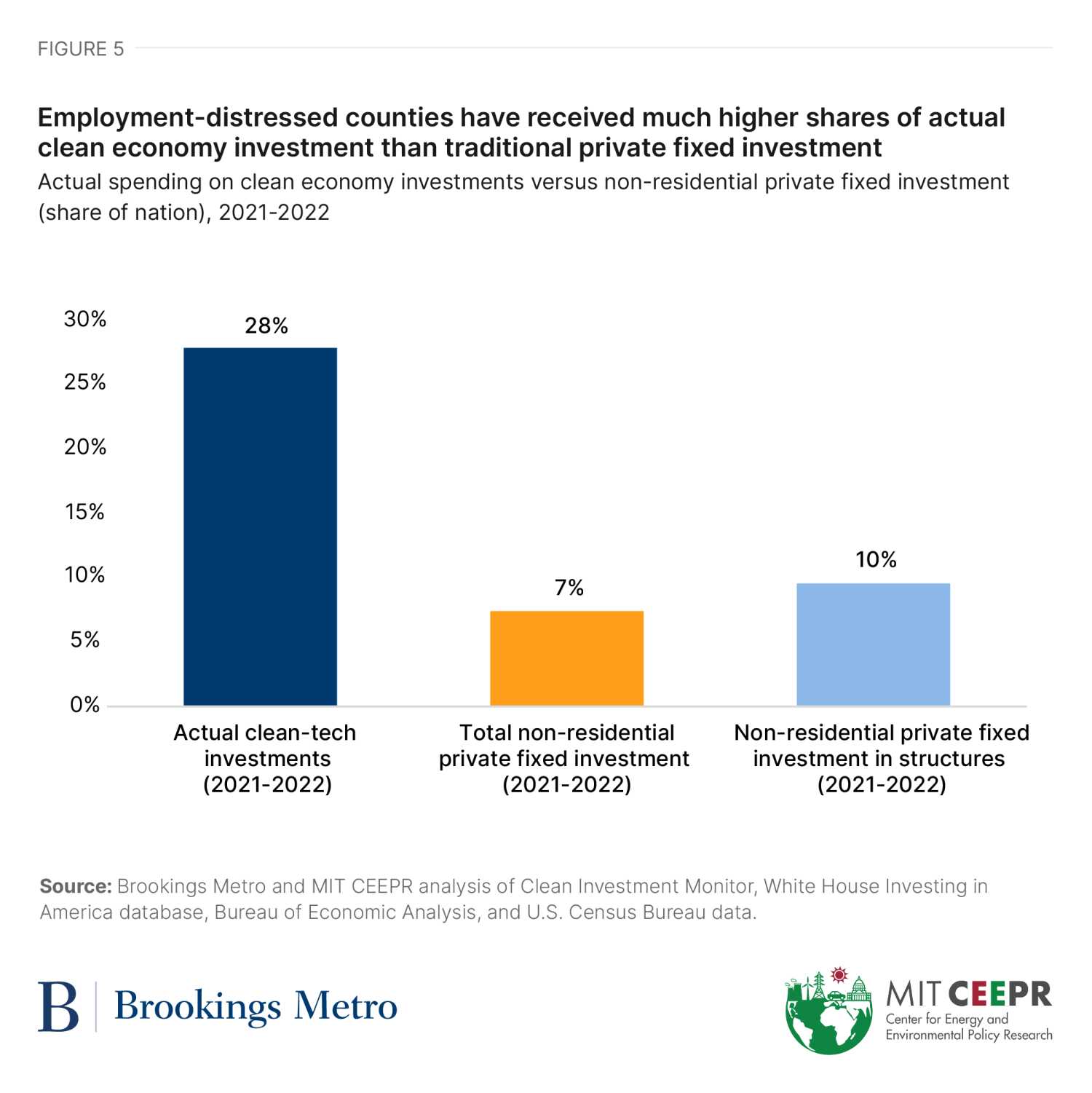

A significantly higher share of actual clean-tech investment went to employment-distressed communities compared to private investment writ large. Actual clean-tech investment in employment-distressed communities was nearly four times total PFI to those communities, and 2.9 times structures investment specifically.

Employment-distressed counties that received a strategic sector investment have higher advanced industry employment shares than non-recipient distressed counties

Prior Brookings Metro research identified a set of “advanced industries” that are critical to U.S. innovation, productivity, and prosperity. These industries—which include auto manufacturing, pharmaceuticals, clean energy generation, and digital services—are “advanced” because they invest heavily in research and development and employ large numbers of STEM workers.

Together, these high-value, export-intensive industries account for 90% of the nation’s private sector R&D spending; saw their wages grow 1.7 times faster than non-advanced sectors between 2001 and 2020; and in 2022 accounted for 7 million decent-paying jobs that typically did not require a bachelor’s degree.

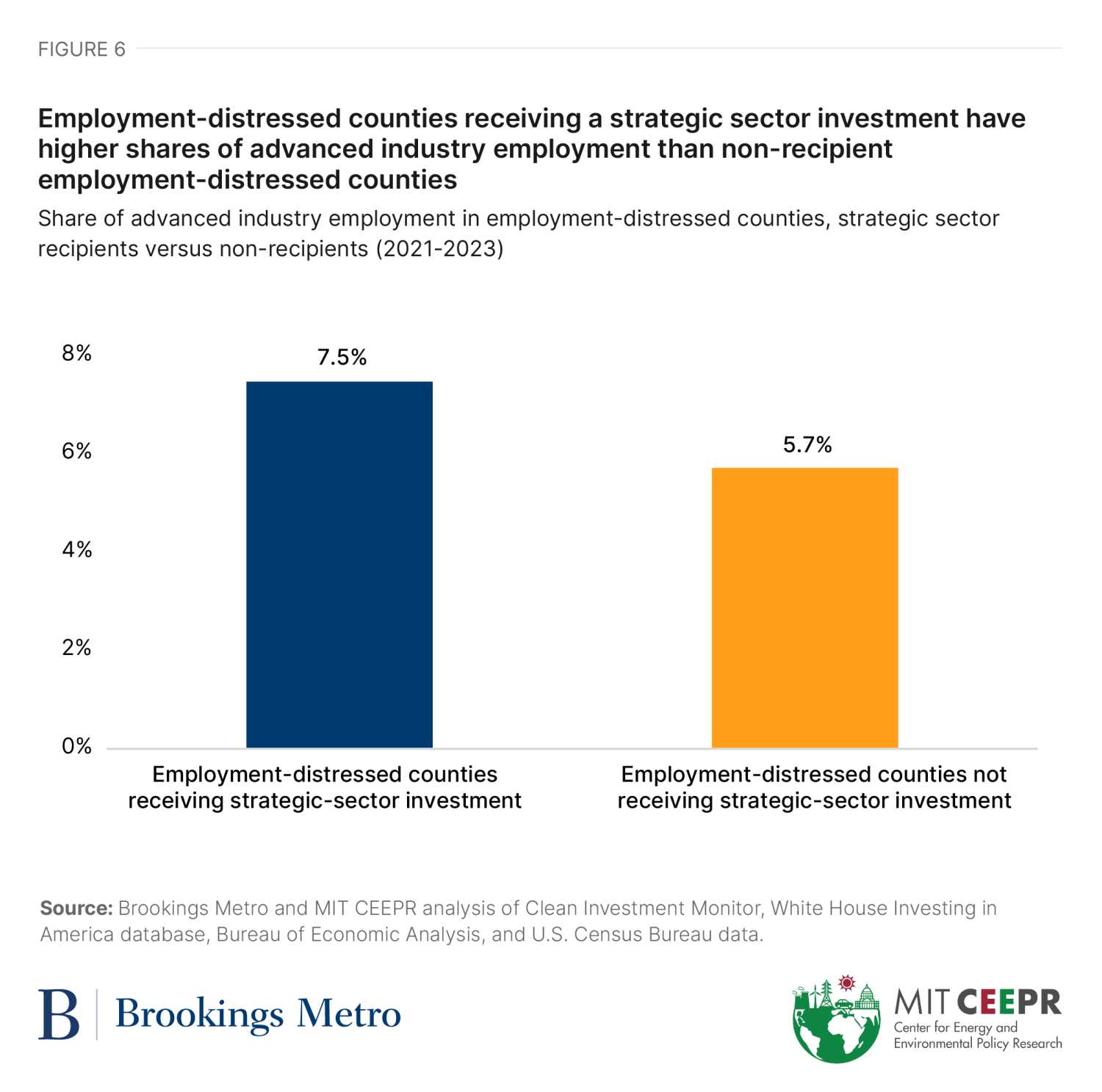

The presence of these industries in a local economy often signals unique capabilities for advanced production. It is not surprising, then, that employment-distressed counties that have received a strategic sector investment have a share of local employment in advanced industries that is on average 31% higher than non-recipient distressed counties. Among the 70 recipient employment-distressed counties, the local share of advanced industries employment is 7.5%, compared to 5.7% in non-recipient distressed counties.

Notably, there are about 250 employment-distressed counties with at least 7.5% of their local employment in advanced industries which have not yet received a strategic sector investment. Thus, the presence of advanced industries is by no means the only factor that motivates investment decisions, but this marker may reveal a much broader set of distressed counties with the necessary conditions to support a strategic sector investment in the coming years.

For example, Putnam County, Ind. and Gila County, Ariz. are employment-distressed counties that have not yet received a private strategic sector investment, but have a similar share of advanced industry employment as those that have. And like many others, these employment-distressed counties share a regional talent pool with other planned private investments—better preparing them to build and expand their activity in advanced industry supply chains. So, while about 7% of employment-distressed counties have received a strategic sector investment since 2021, an additional 24% of employment-distressed counties may be attractive to investors according to this predictive indicator.

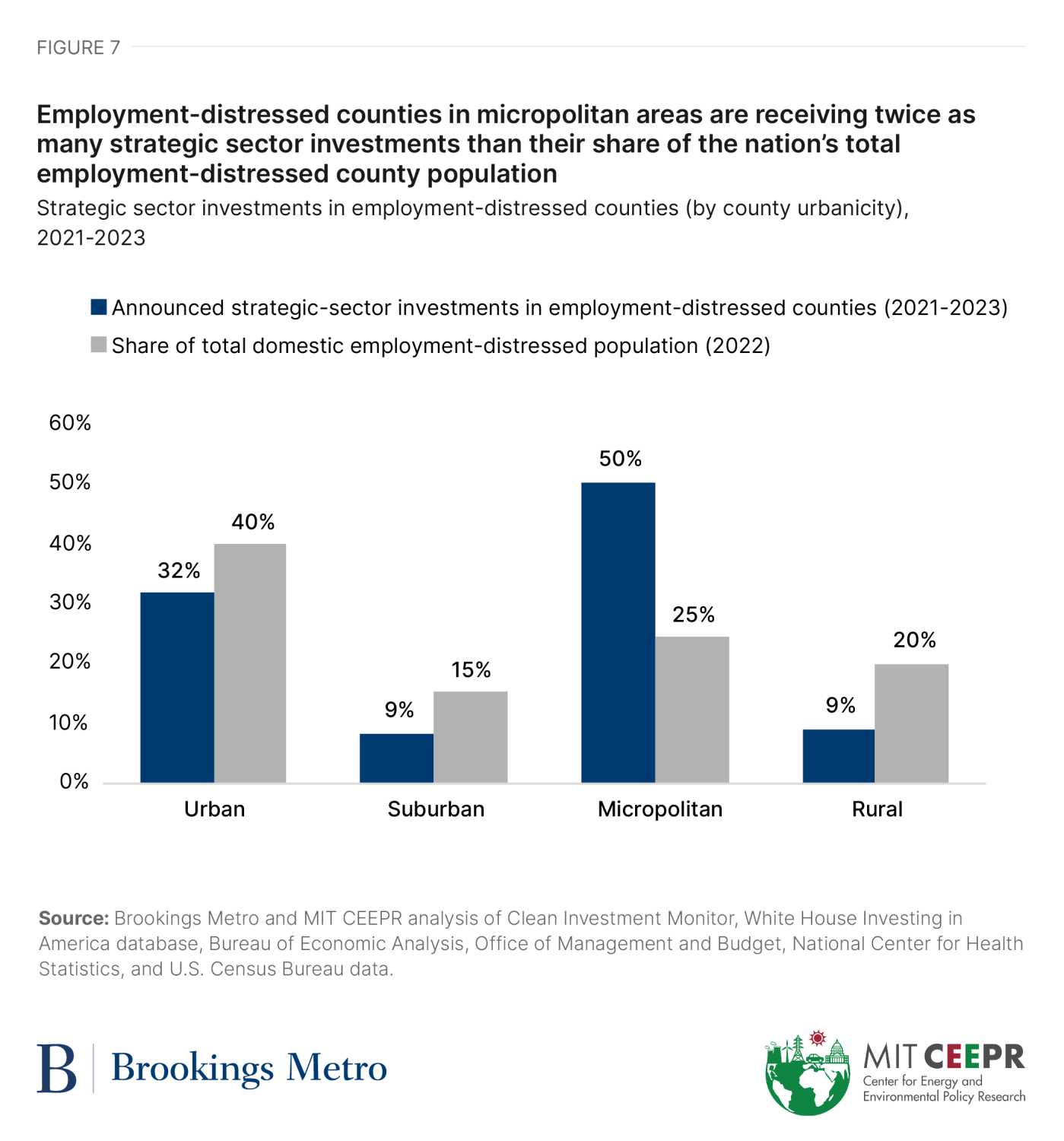

Strategic sector investments in employment-distressed counties have disproportionately flowed to smaller population centers

Regions that have at least one urban area with a population of 50,000 or higher are defined as “metropolitan statistical areas,” while regions that have at least one urban area with a population between 10,000 and 50,000 are defined as “micropolitan statistical areas.” Across employment-distressed areas, counties located in micropolitan statistical areas have proven especially attractive to investors and manufacturers. Micropolitan areas account for approximately 25% of the nation’s total employment-distressed population, but these areas have received 50% of all announced strategic sector investments in employment-distressed counties since 2021.

The trend toward micropolitan areas is important for both understanding investor priorities around site selection and for identifying other employment-distressed counties that may be prime candidates for future investment. The tremendous scale required to manufacture electric vehicles, batteries, and semiconductors likely means that companies are seeking the plentiful land and build-ready sites available in many micropolitan regions, with the assumption that they can draw on a larger workforce living in nearby metropolitan areas. One example is Haywood County, Tenn.—an employment-distressed micropolitan county adjacent to the Jackson, Tenn. metro area that has a high share of advanced industry employment, and where Ford and SK On have partnered to build a new electric vehicle manufacturing plant on a 2.3-square-mile plot of land. Similarly, in Matagorda County, Texas—a micropolitan county on the outskirts of Houston—HIF Global is investing over $6 billion to build the world’s largest e-fuels facility, which will capture over 2 million tons of carbon dioxide per year when fully operational.

Strategic sector investments are charting a different geographic course, but intentional strategies are still needed

The previous three years of data indicate that after decades of economic divergence, strategic sector investment patterns are including more places that have historically been left out of economic growth. Employment-distressed communities are receiving an outsized share of strategic sector investments compared to their share of economic activity, population, and overall private investment from the last few years and investment in the last decade. And the map is not yet finished: There are hundreds of distressed counties with assets similar to those that have attracted investment and have not yet been targeted.

This suggests that the benefits of a national industrial strategy can reach people and communities that have historically been excluded from economic opportunity—a trend that bodes well for the entire country. Economist Timothy J. Bartik’s research has shown that there are disproportionate benefits to the national economy when jobs are created in communities with low employment rates.

Acknowledging this early progress, the path from private investment into broadly shared and inclusive economic opportunity is not automatic—it requires intentional strategies to connect local workers and businesses to these new investments. Policies that create these “local linkages”—in the language of economic development—are crucial to ensuring that residents benefit from the investment surge. Absent intentionality and inclusion, the benefits of these strategic sector investments may not extend to local workers and communities.

Federal place-based policies—such as the Regional Technology and Innovation Hubs program and the Recomplete Pilot Program—offer the kinds of flexible support for government, education, and community institutions to partner with the private sector to drive inclusive economic growth at the local level. But while these programs are carefully designed and grounded in hard evidence about what works, Congress has not yet adequately funded them. In the shorthand of lawmaking, they have been “authorized”—a big step forward, but with limited funds “appropriated” to them relative to their clear potential for economic revitalization and innovation in communities that have long struggled.

In the absence of adequate federal funding, local, state, and philanthropic investors can also provide support to local communities. Indeed, all levels of our federalist system will need to align resources, capacity, and political will to make the most of this strategic sector investment surge.

Authors

-

Footnotes

- A region’s prime-age employment rate (PAER) represents the share of that region’s population age 25 to 54 that is currently employed. Each region’s prime-age employment gap (PAEG) is defined as the difference between the national five-year PAER and the region’s five-year PAER.

- Recompete uses this criteria only for counties that: 1) do not cover the entire area of their local labor market; and 2) exist within a local labor market with a PAEG below 2.5%. Counties with five or more contiguous census tracts that each have a PAEG above 5% and a median household income below $75,000 may also be eligible for Recompete funding even if the county itself does not meet these thresholds, as long as the organization applying for funding is located within these census tracts.

- While the COVID-19 recession officially lasted from February 2020 through April 2020, this report defines 2020 as a pre-recovery year to account for the unusually severe magnitude of the recession’s impact on 2020’s total gross domestic product and employment indicators.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).