This March, the White House released an interactive map displaying the over $470 billion in private industrial investments announced since January 2021. These investments in semiconductors, clean energy, electric vehicles, and batteries are the result of a renewed economic and national security vision, as National Security Advisory Jake Sullivan argued in an April speech at the Brookings Institution. Sullivan called for a “new Washington consensus” that deploys robust public investments in critical advanced industries and technologies. Those investments, he said, will aim to rebuild America’s industrial economy, strengthen national security, enhance climate resilience, and address rising geographic inequality. Sullivan’s remarks spoke to what The Economist called “the Biden doctrine,” which has stirred significant debate, with supporters crediting the approach for a widespread manufacturing boom and critics attacking it as far too protectionist abroad and unlikely to put a dent in inequality here at home.

On the latter challenge, how and where these capital investments land in local communities will largely determine whether this new industrial strategy can deliver economic benefits to a broad swath of the country. In this piece, we analyze the geography of the $470 billion in private sector investments across five key segments: semiconductors and electronics; clean energy; electric vehicles and batteries; biomanufacturing; and heavy industry such as chemicals, metals, and appliances.

Nearly half of the private investment announced so far is in the semiconductor industry

As of May 2023, the White House’s “Investing in America” interactive map included over 270 projects spread across the five key segments mentioned above, sourced from public press releases, industry associations, and news articles. (Note: Prior to the completion of this piece, the White House removed the heavy industry category and updated the investment total to $479 billion. The analysis presented here reflects the earlier version of the interactive map data.)

Semiconductors and electronics represent nearly half (46%) of the committed investments, largely due to the costly nature of fabrication plant construction. Of the 10 largest investments announced since 2021, semiconductors account for nine. Semiconductor executives have been among the most explicit in crediting recent legislation—namely, the CHIPS and Science Act of 2022—for influencing their investment decisions.

While the majority of the announced investments are committed to semiconductors, energy technologies also loom large. Roughly 48% of new investment announcements are energy-related, with $140 billion in new private capital committed to electric vehicle and battery manufacturing and $82 billion committed to clean energy production. Electric vehicles and batteries account for the largest number of projects (101). Though biomanufacturing and heavy industry investments account for a relatively low share of investment dollars, they still represent a quarter of all investment projects.

Capital investments allocated to the South are well above the region’s national population and GDP share

Southern U.S. states house 38% of the nation’s population and generate 34% of its GDP. But this region accounts for 42% of the announced industrial investments—a substantially higher share than any other region. New production facilities focused on clean energy technologies and electric vehicle/battery manufacturing together account for 62% share of investment in southern states—a larger proportion than across the nation overall (48%). This regional industrial expansion has garnered significant media attention over the past year. Georgia Governor Brian Kemp has touted his state’s rise as “the battery belt,” while some observers have noted that the long-term shift of manufacturing to the South is due to its comparatively lower wage rates, anti-labor political climate, and right-to-work laws that discourage unionization.

In contrast, the Northeast is slated to receive only 13% of new private investments, despite the region housing 17% of the U.S. population and generating 20% of its GDP. Meanwhile, the West and the Midwest are attracting investments in line with their respective shares of economic output.

An economically, geographically, and politically diverse set of counties are receiving advanced industry investment

In rebuilding America’s industrial capacity, the Biden administration aims to stimulate growth and prosperity across a wide range of places. Figure 4 categorizes U.S. counties into four equal groups based on their employment rate (the percentage of individuals ages 18 to 64 that are currently employed).

There are several notable patterns. First, only 4% of new capital investments are being directed to counties with the nation’s lowest employment rates, aligning with these counties’ share of national GDP (3%). At the other end of the spectrum, counties with the highest employment rates have attracted 44% of the new investments—the largest share among county categories, although still below their share of national GDP (61%). Together, the two “middle” categories of counties in terms of employment rate account for 36% of GDP but have secured 52% of new private investment; thus, relative to their share of the nation’s economic output, these two categories of counties are receiving the most investment.

This data suggests that the capital investment boom is neither flowing to the most distressed places in America nor to those counties that already have the strongest labor markets. Rather, manufacturers are disproportionately investing capital in “middle” places that are neither too distressed nor too dynamic. These counties are home to a large share of the nation’s population and workers, yet have room for further growth and hiring.

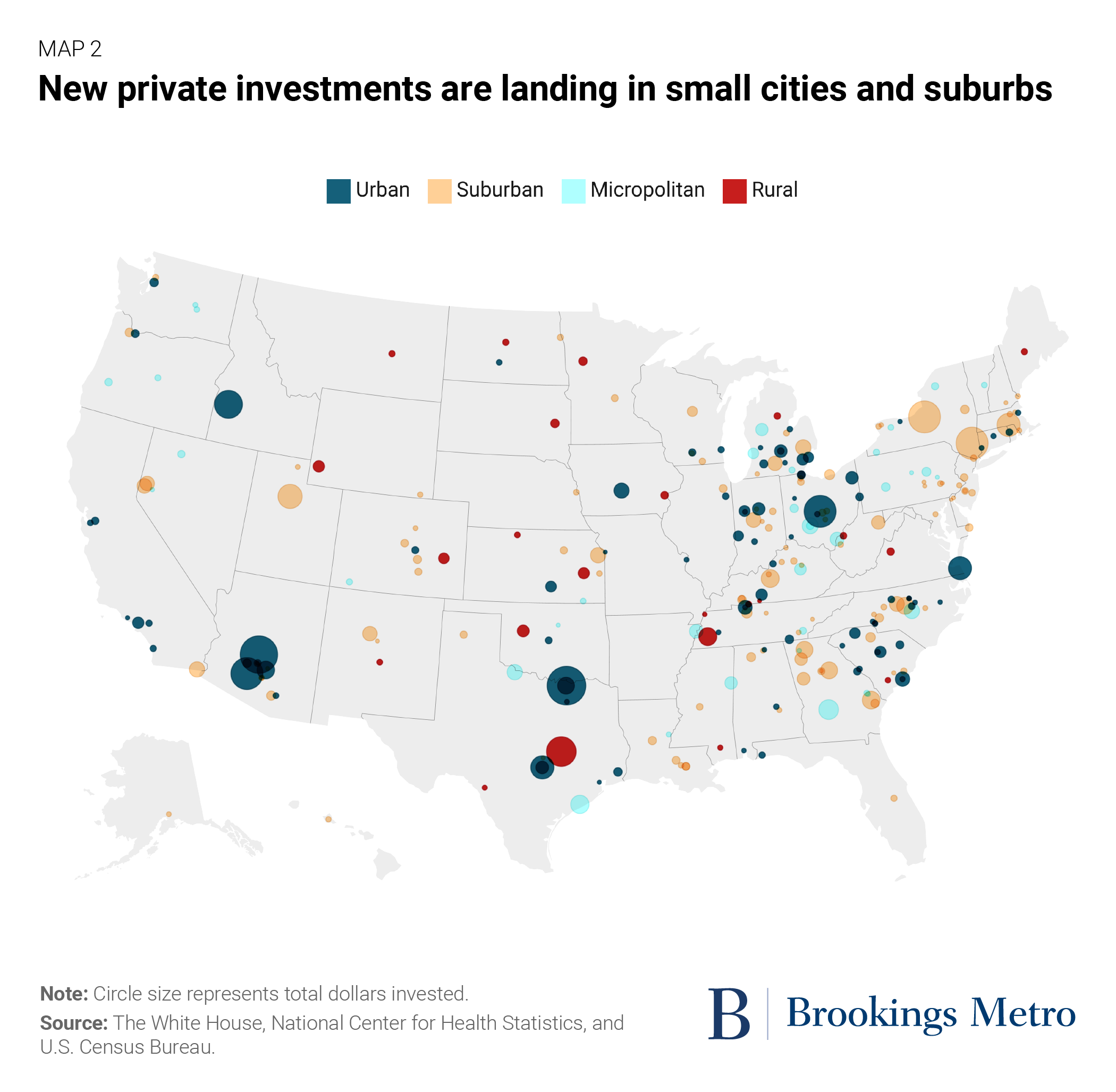

The geographic and economic distribution of communities receiving investment comes as advanced industries continue to decentralize out of densely populated urban centers—a process that has been unfolding for over a century. While the private sector has overwhelmingly opted to locate investments within metropolitan areas, a sizeable share of total investments are in small cities and suburban communities (48%), rather than urban cores (44%).1

This geographic distribution underscores that advanced manufacturers are engaged in a balancing act. On one hand, proximity to large cities remains a high priority. Successfully scaling advanced industry clusters, particularly in regions where a given sector is still nascent, typically requires access to the innovation capital of research universities, most of which are located near larger urban regions. Yet expansion into smaller cities and suburban communities provides investors (and their employees) access to valuable factors that are becoming scarcer in denser urban cores, such as land and affordable housing. Straddling the urban-rural divide, therefore, provides manufacturers with the benefits of both geographies.

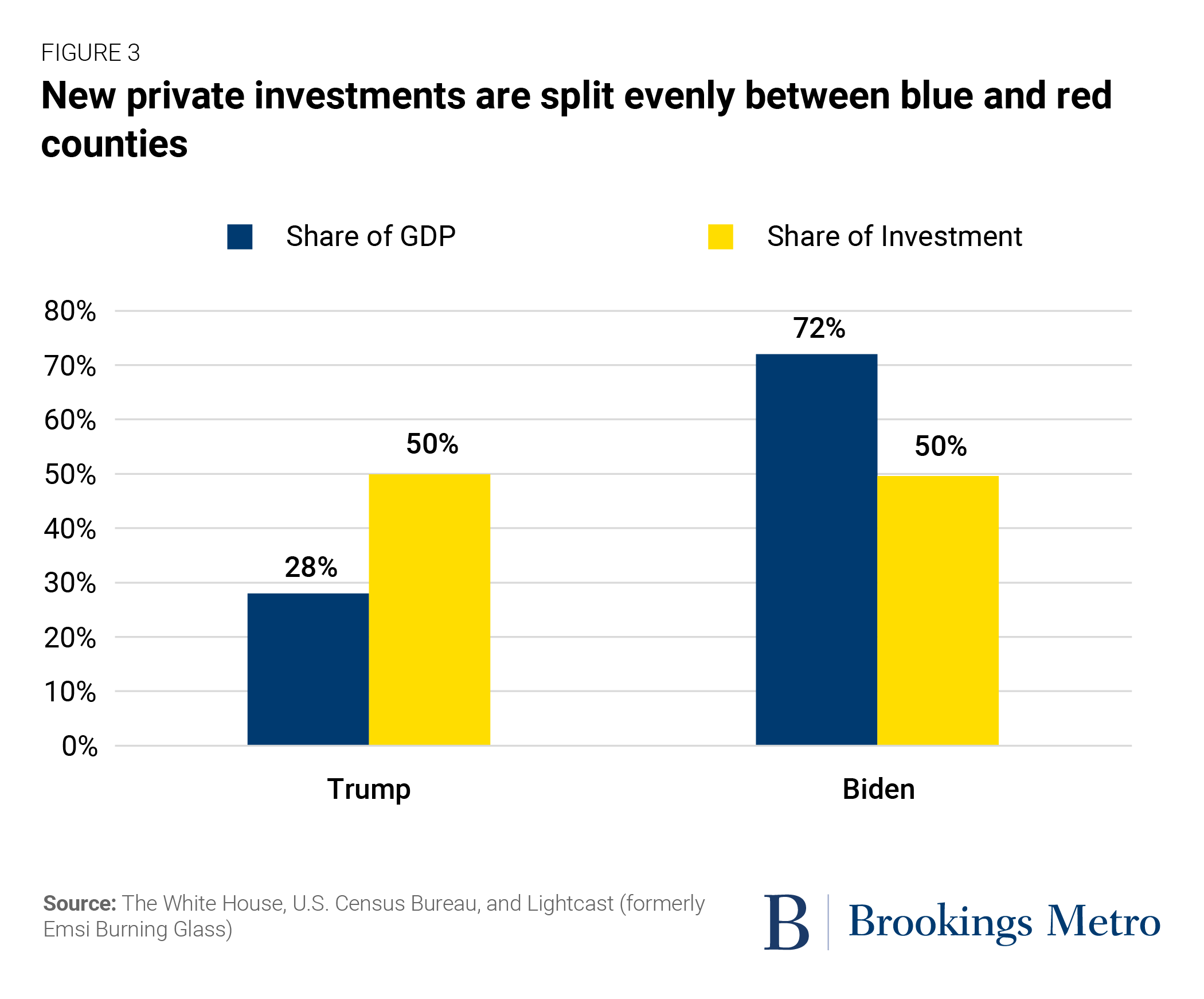

In addition, this dispersion of investment across suburbs and small towns means that politically conservative counties have received a higher share of private investment than would be expected given the size of their economies. In total, about half ($233 billion) of the new private investments announced since President Joe Biden took office are for developments in counties won by former President Donald Trump in the 2020 presidential election. These counties produce roughly a quarter (28%) of national GDP.

Despite historic investment, challenges remain in building an economy that works for all

Brookings Metro has previously noted that a key step in building an economy that works for all is place-based rejuvenation of the U.S. advanced industries sector. While the Biden administration’s new industrial strategy appears to be fostering the type of cooperation between business and government that’s critical for this rejuvenation, continued alignment is not guaranteed. There will inevitably be tensions between the interests of global companies and shareholders on one hand, and what policymakers and voters may deem in the public interest on the other. For example, TSMC—a Taiwan-based semiconductor manufacturer that has committed to invest over $28 billion into new factories in Arizona—has referred to the CHIPS Incentives Program’s profit-sharing provision as “unacceptable,” while Commerce Secretary Gina Raimondo has insisted the federal government will “not write blank checks to any company that asks.”

Despite these challenges, the opportunity to reverse multiple decades of decline in America’s advanced industries is also unprecedented, and there are emergent approaches—including more transparent and enforceable community investment frameworks and community benefits agreements—that can help business leaders and communities navigate both the shared interests and tensions. By deploying these new tools, federal policymakers, industry leaders, and their community partners have a generational opportunity to advance equitable economic growth that benefits more people in more places.

Authors

-

Footnotes

- Brookings Metro defines “urban” counties as counties that are classified as “large central metro counties” by the NCHS Urban-Rural Classification Scheme for Counties, and counties in a metropolitan statistical area of any size that contain one or more of the metro area’s principal cities, regardless of population. Counties in metropolitan statistical areas that do not contain a principal city are defined as “suburban.” Counties in micropolitan statistical areas are defined as “small cities.”

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Spurred by federal legislation, new industrial investments are reaching a wide swath of the country

June 13, 2023