This viewpoint is part of Chapter 1 of Foresight Africa 2026, a report on how Africa can navigate the challenges of 2026 and chart a path toward inclusive, resilient, and self-determined growth. Read the full chapter on mobilizing Africa’s resources for development.

Africa must invest more if it is to grow. Investment delayed could be development denied.

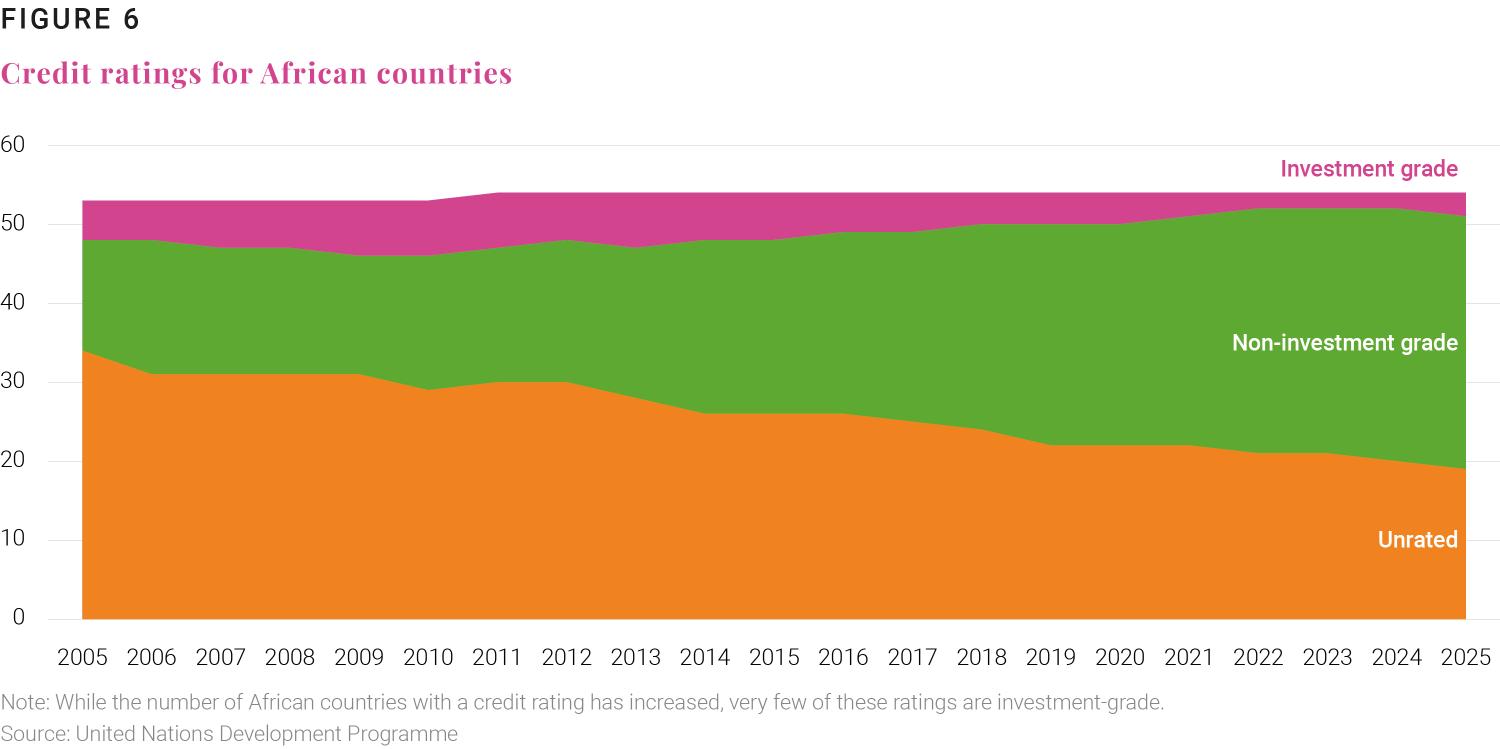

After stabilizing their macro indicators by the turn of the century, many African countries sought external financing for critical investments in infrastructure and technology that were necessary for growth and vital to the attainment of their development aspirations. Unfortunately, their access to global financial markets was stymied: At that time, only one African country, South Africa, had a sovereign credit rating.1 To address this, UNDP partnered with S&P in 2003 to support credit ratings for viable African countries. Since then, 34 African countries have been rated and 21 countries have raised $155 billion Eurobonds.2

The effects of access to global capital markets

In the early 2000s, some observers were concerned that providing African countries with credit ratings would signal “market readiness.” They opined that access to global capital markets could result in excessive borrowing that would undo debt relief efforts under the IMF and World Bank’s HIPC and MDRI frameworks.3 Thus, in the present day one may ask: Has Africa’s access to more non-concessional lending via ratings precipitated or worsened Africa’s debt crises?

First, it is important to note, as documented in previous Brookings research,4 that African countries need to borrow for a number of reasons. For instance, they do not earn enough from their exports and their capital investment needs exceed potential revenue streams (even when we assume zero corruption). Moreover, unlike in 2000 when 70% of the continent was categorized as low-income, thereby enabling them to access concessional development financing, in 2025, half of the continent is middle-income and must rely more heavily on commercial sources to finance its development.5 Additionally, aid flows to African countries have dipped in recent years, declining by 15% between 2020-23.6 Against this backdrop, credit ratings play a uniquely important role in determining Africa’s access to affordable financing.

Unlike other regions that have multiple data points to assess risk, the dearth of relevant and reliable data in Africa means that credit ratings play an outsized role in determining risk perceptions.7 UNDP estimated that 16 African countries pay more in debt servicing costs than they should because credit ratings are lower than they could be. The total estimated resulting loss is over $74 billion,8 exacerbating Africa’s debt service stress. While credit ratings are not the only reason Africa’s borrowing costs are so high, there is no doubt that they play a central role as a benchmark signaling indicator.

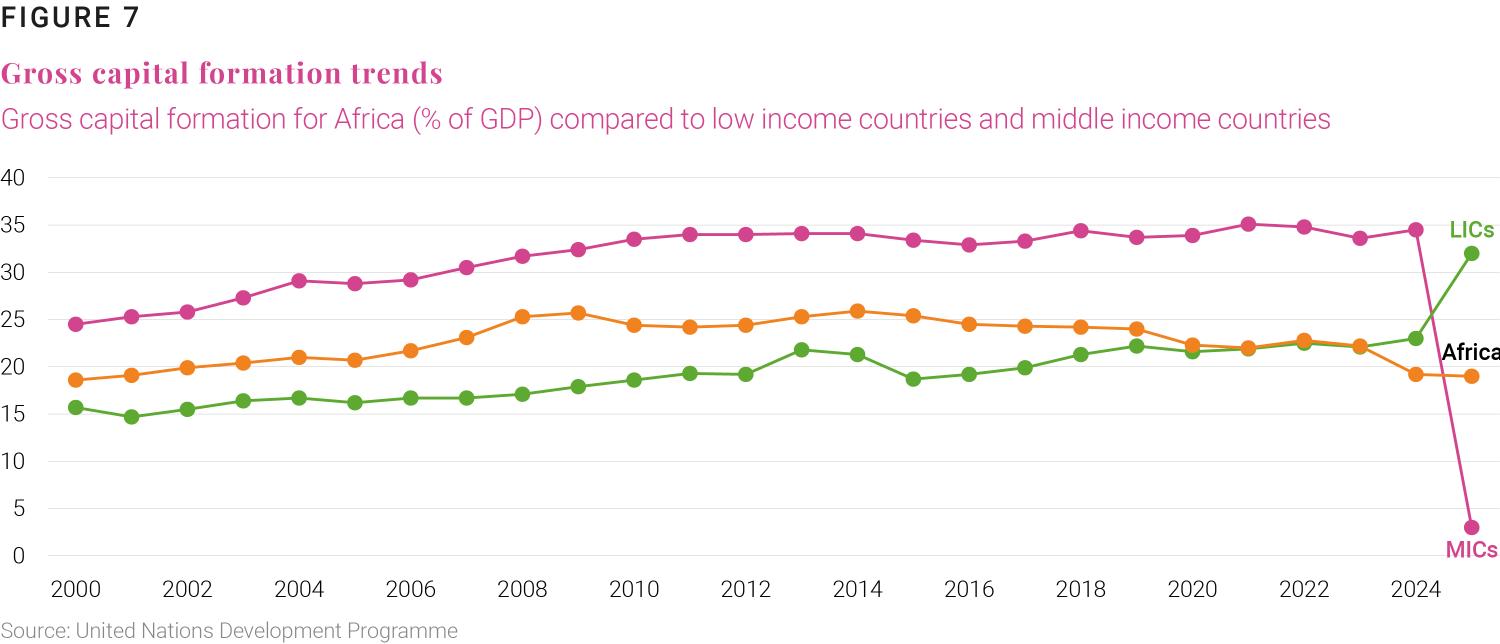

As of end October 2025, only three of the rated 34 African countries are rated as investment grade.9 Thus, borrowing for most of the continent attracts a premium (for the non-investment grade countries) or punitive rates (for the 38% of the continent that is unrated).10 Moreover, this elevated cost of borrowing is often misaligned with the region’s actual financial potential. For example, at 2.6%, default rates on infrastructure investments in Africa are among the lowest in the world.11 Costly financing is also causing a slowdown in Africa’s gross capital formation, which is far below the average of 33% for middle-income countries.12 Yet Africa must invest more if it is to grow. Investment delayed could be development denied.

Pathways to improve Africa’s sovereign credit ratings

Targeted and consistent efforts to improve credit ratings for African countries could be transformative and help Africa finance its development without being burdened with unsustainable debt. Such efforts could free up much-needed fiscal space by reducing borrowing costs and increase the size and quality of investment flows. Furthermore, the credit ratings process could help establish conditions for improved economic governance. However, getting this right requires concerted and coordinated efforts by the credit ratings agencies and African countries.

Credit ratings agencies must:

- Accept that credit ratings are more than “an opinion” in Africa, they are “an assessment,” a distinction recognized by the International Organization of Securities Commissions in 2015.13 As such, more attention should be given to the robustness of the scores in an African context. For example, the Sevilla Commitment14 and the Vatican’s Jubilee Report15 call for innovations like the use of state contingent clauses and longer term analyses.

- Focus on determining African countries’ ability to repay and not revisit backward leaning and lagged indicators. While it is true that credit ratings often mirror GDP rankings and human development indices, a country’s future potential is best measured by more accurate accounting of its wealth (e.g. going beyond GDP to include natural capital) and micro-level governance reforms.

- Invest in in-country intelligence. Global ratings agencies have a weak presence across the continent. Some are making efforts to address this through partnerships and acquisitions, but much more should be done.

- Adapt methodologies to fit the African context. This is not a call for African exceptionalism: Credit ratings methodologies must be globally consistent. However, in emerging markets it is possible to adapt the methodology to more accurately reflect regional conditions; S&P has a tailored approach for Mexico.16

African countries must:

- Take credit ratings missions seriously. Countries must have high-level, technical committees that are equipped and empowered to tell the country’s story convincingly and able to negotiate with the ratings agencies effectively. This function must not be outsourced to external advisors.

- Invest in capacity and data. This must include assuring the quality and timeliness of data during credit ratings missions. Working in partnership with knowledge institutions and development partners, countries should also invest in upskilling technical and strategic staff. As part of its efforts to strengthen countries’ capacity, UNDP’s Africa Credit Ratings Initiative trained over 250 senior African officials in 2025.17

- Align credit ratings activities with development strategies, not political aspirations. For example, UNDP’s initiative works with governments to embed credit ratings strategies within national development plans. This bodes well for stronger alignment and consistency.

- Support the Africa Credit Ratings Agency (AfCRA) established by the African Union.18 The AfCRA could help reduce the cost of borrowing by championing the region’s efforts to reform methodologies, improve data, and strengthen public sector capacity. It is worth noting that knowledge products and policy analysis from Africa’s educational institutions and think tanks must also play a vital role in supporting AfCRA.

Credit ratings are not a silver bullet. They constitute an important signal that can catalyze available and affordable financing, which Africa needs to accelerate its development aspirations and transform lives across the continent.

Related Content

-

Footnotes

- Maggie Mutesi, “Gatekeepers of Growth: How Sovereign Credit Ratings Are Shaping Africa’s Future,” Africatalyst, August 11, 2025., To understand the relationship between access to global financial markets and credit ratings, one must recognize that sovereign ratings assess a government’s ability (and willingness) to meet its debt obligations fully and on time. As such, they serve as a market indicator for pricing risk.

- Misheck Mutize, “Eurobonds Issued by African Countries Are Popular with Investors: Why This Isn’t Good News,” The Conversation, January 8, 2025.

- The IMF and World Bank spearheaded the Heavily-Indebted Poor Countries (HIPC) debt treatment initiative in 1996 and the Multilateral Debt Relief Initiative (MDRI) in 2005 to reduce the stock of debt owed by developing countries.

- Brahima Coulibaly et al., “Is sub-Saharan Africa facing another systemic sovereign debt crisis?,” Africa Growth Initiative at Brookings, April 2019.

- Eric Metreau et al., “World Bank Country Classifications by Income Level for 2024-2025,” World Bank Blogs, July 1, 2024.

- International Monetary Fund, G-20 Background Note on Macroeconomic Vulnerabilities in Africa: Key Issues and Policy Lessons (2025).

- Daniel Cash, Reforming the International Financial Architecture: The Role of Credit Ratings Agencies in the “Debt Crisis” (United Nations University, World Institute for Development Economics Research, 2025).

- UNDP Regional Bureau for Africa, Lowering the Cost of Borrowing in Africa the Role of Sovereign Credit Ratings (United Nations Development Programme, 2023).

- United Nations Development Programme, “Africa Credit Raatings Resource Platform,” 2025.

- “UN General Assembly 2025: UNDP Convenes Dialogues on Credit Ratings Reform,” United Nations Development Programme, September 23, 2025.

- “How Risky Is African Infrastructure Anyway?,” Infrastructure Investor, March 31, 2025.

- The Pontifical Academy of Social Sciences, The Jubilee Report: A Blueprint for Tackling the Debt and Development Crises and Creating the Financial Foundations for a Sustainable People-Centered Global Economy (Initiative for Policy Dialogue, Columbia University, 2025).

- UNCTAD, ed., Credit Rating Agencies, Developing Countries and Bias: Policy Review, United Nations Publication (United Nations, 2025), 24.

- United Nations, Sevilla Commitment: Outcome Document Adopted at the Fourth International Conference on Financing for Development, A/RES/79/323 (2025).

- The Pontifical Academy of Social Sciences, The Jubilee Report: A Blueprint for Tackling the Debt and Development Crises and Creating the Financial Foundations for a Sustainable People-Centered Global Economy.

- “Ratings Firm S&P Launches Methodology Tailored to Mexican Market,” Mexico News Daily, November 11, 2025.

- “About the Africa Credit Ratings Initiative,” United Nations Development Programme, 2025.

- “African Leaders Convene on Establishment of Homegrown Solution, the Africa Credit Rating Agency,” African Union, February 7, 2025

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Sovereign credit ratings and external debt in Africa

March 5, 2026