Finance available for development

The House and Senate are in the throes of reauthorizing the statutory authority of the Development Finance Corporation, whose ability to support new investment projects was suspended on October 1 with the expiration of the BUILD Act. The DFC was established to support U.S. foreign policy interests through advancing economic progress in developing countries by providing loans, equity finance, guarantees, and political insurance for market-viable investments in developing countries when private finance is not available to cover the full cost of a project.

The role of the DFC is even more important today, per global development finance and programmatic trends, than when it was created in 2018 as the successor to the Overseas Private Investment Corporation. With eight major donors (Finland, France, Germany, the Netherlands, Norway, Sweden, Switzerland, and the United States) reducing assistance in the last few years, official development assistance (ODA) declined 7% to $212 billion in 2024 and is projected by the OECD to fall an additional 9-17% in 2025. For the U.S., the takedown of USAID and cancellation of much of foreign assistance, has elevated the DFC’s role as a U.S. development tool.

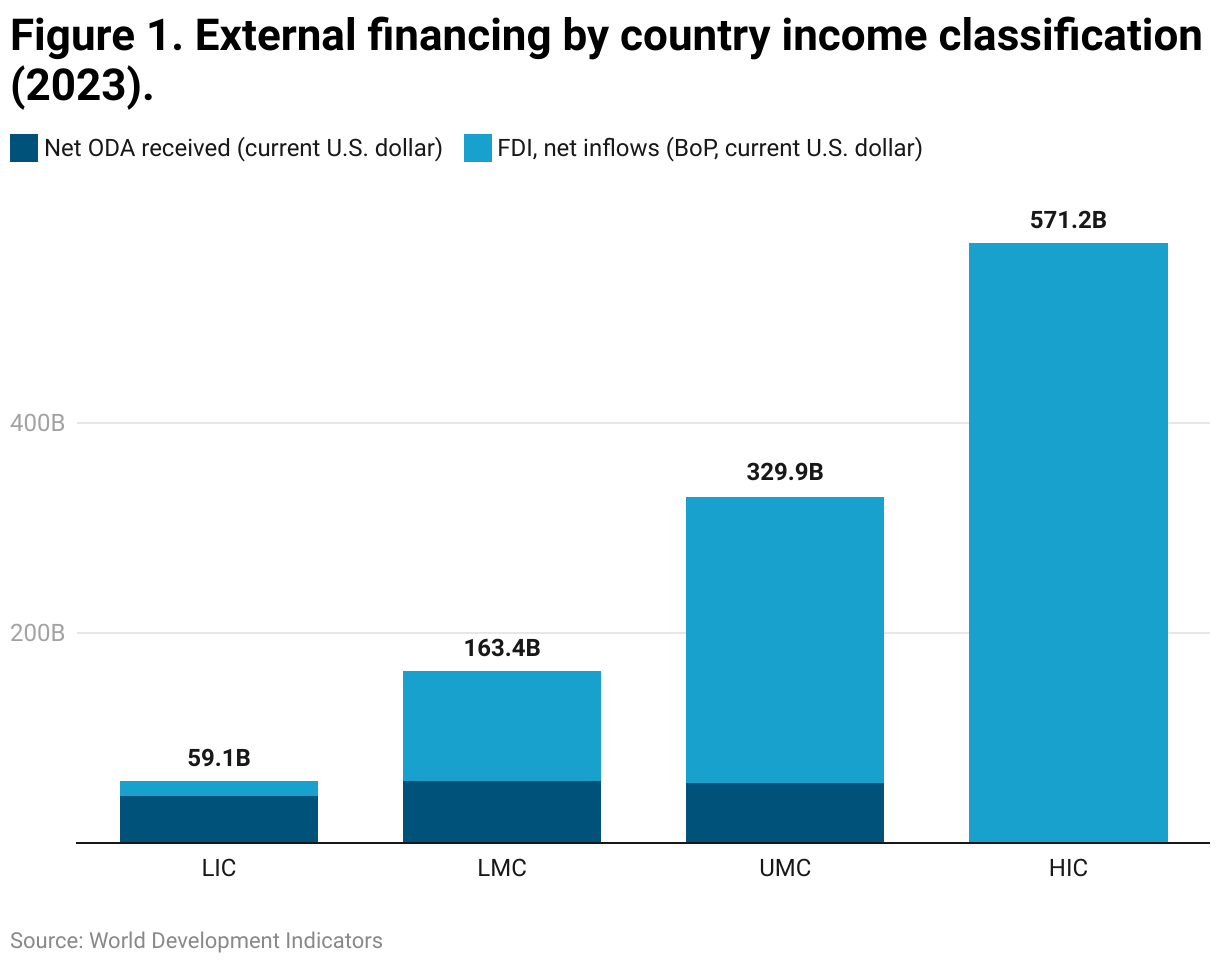

As to where the need is, the Congress has correctly prioritized DFC support for low and lower-middle-income countries. According to the World Bank’s World Development Indicators, external financing is heavily concentrated in higher-income countries. This underscores the limited access of low- and lower-middle-income economies to global capital. For instance, low-income countries (LICs) received $59 billion, between foreign direct investment (FDI) and ODA. Lower-middle-income countries (LMCs) attracted over $160 billion. By contrast, upper-middle-income countries (UMCs) received $330 billion, while high-income countries (HICs) absorbed more than $570 billion—almost ten times the total inflows to LICs.

Private direct investment flows to emerging market and developing countries (EMDCs) have been in relative decline from a high of 4.5% of GDP of the receiving country in 2008 to less than half that level at 2.1% in 2023, even lower than the 2.3% in 2000. Along with these financial trends have come a recognition of the central role of the private sector in a country’s economic progress and efforts to find ways to both enhance the role of the private sector and ensure it is compatible with sustainable development.

Legislation

So, given this environment, it is critically important that Congress move expeditiously to reauthorize the BUILD Act, keeping foremost in mind that, to be effective, it must have the ability to act with nimbleness and take calculated risks in order to serve the needs of clients and be competitive in the global marketplace.

The House and Senate have separate reauthorization vehicles—the House Foreign Affairs Committee reported bill HR 5299 and Senate amendment 3826 to the pending NDAA (National Defense Authorization Act). Each has provisions that would support its focus on development and allow it to operate in a nimbler fashion. Joining those provisions together would make the DFC a stronger, more effective agency. But each also contains provisions that undercut those two core principles.

Development mandate

The BUILD Act is grounded in prioritizing DFC support for investment in low- and lower-middle-income countries. Acknowledging efforts afoot to redirect the DFC to supporting economic projects for the U.S. supply chain, the Senate amendment reinforces the development mandate by placing guardrails around DFC engagement in high-income countries where project finance needs are already met by the marketplace. Specifically, for high-income countries, it would restrict support to 8% of the agency’s outstanding contingent liability, reinforce the statutory provision that DFC support is to be additional—i.e., should not crowd out private finance—and require that a project produce developmental outcomes for the poorest populations in the country.

In contrast, the House bill contains a policy statement that would take the DFC well beyond its legislated development mission and areas of expertise. It directs the DFC to support the U.S. supply chain by facilitating investment in the U.S. and export of energy, telecommunications, technology, and expertise—activities that fall more appropriately in the capabilities of other USG agencies, specifically the Export-Import Bank of the United States (EXIM) and departments of Energy and Commerce.

Further, the DFC is viewed by many as a response to China’s Belt and Road. That is appropriate, but, as the data above on external financing by income-group illustrates, where that support is needed is in low and lower-middle-income countries, not in upper-middle and high-income countries.

Nimbleness

For the DFC to effectively fulfill its mission, it must be nimble and willing to take country and market risks, much as the private sector does. OPIC before and DFC now have been overly risk-averse. The House bill appropriately encourages the DFC to “responsibly increase its risk tolerance.”

At a time when more is expected of the DFC—the House bill increases the agency’s contingent liability from $60 billion to $250 billion, and the Senate amendment to $200 billion—but its staffing has been reduced from some 700 to just above 500, and it has lost the support structure that had been provided by staff at USAID country mission. One obvious path to finding ways to do more with less is to streamline operations. The House bill does that through eliminating the statutory position of chief development officer, a well-intended but ineffective senior management position. In the vein of flattening the bureaucracy to reach the quick decisions the private sector needs, the Congress should avoid the equally well-intentioned Senate provisions of an additional senior-level position (chief strategic development officer) and bodies (Development Advisory Council and Strategic Advisory Group).

At a time when the DFC has lost almost 200 career specialists and professional service is embattled across the government, this is no time for the House provision that would double the number of “administratively determined positions” from 50 to 100.

Current law and the Senate bill set the level of transactions that must be reported to the Hill too low—at $10 million—leading to unproductive staff work for the DFC and Congress and delaying decisionmaking. The House sets it at what may be too high ($100 million) for the Congress to exercise appropriate oversight. A middle ground of $50 million, the level at which decisions currently must be referred to the board, may be a reasonable level.

Transparency

Information is the bedrock for making smart decisions. The DFC has only partially complied with the transparency mandates in the BUILD Act and the Foreign Aid Accountability and Transparency Act. Accurate and detailed data, including at the project level and on impact, is needed for potential clients to make investment decisions, policymakers to exercise oversight, and stakeholders in developing countries to understand and assess DFC investment support. The Senate amendment contains several important provisions to subject meetings of the DFC board to the Sunshine Act and to mandate concerted efforts at monitoring, evaluation, and learning, and publish detailed data on the support it provides and the impact achieved. Business confidentiality is too often used as a ruse, made obvious by the demand for that data by private investors to inform their decisions, to avoid the extra work of making public how public finance is deployed.

Final Bill

Taking the constructive provisions outlined above, along with other provisions common to both vehicles, such as authorizing a revolving fund for equity finance at $3 billion (as a reasonable fix to the current practice of scoring equity as grant assistance), would improve on the original BUILD Act and give the DFC the ability to play the role expected of it. Hopefully, Congress will return to the bipartisanship with which it enacted the BUILD Act and allow the DFC to reopen for business with a renewed development mandate and nimbleness.

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Reauthorization of the Development Finance Corporation

November 5, 2025