Since the beginning of 2023, there has been escalating tension in United States-South Africa relations. South Africa engaged in a joint naval drill—Mosi II—with Russia and China, coinciding with the one-year mark of the Ukrainian invasion. In reaction, a group of U.S. policymakers put forth House Resolution 145, urging the Biden administration to “conduct a thorough review of the United States-South Africa relationship.” The tension escalated in May 2023 when the U.S. ambassador to South Africa publicly alleged that South Africa had secretly provided weapons to Russia to use against Ukraine.

Subsequently, South African President Cyril Ramaphosa formed a three-person panel to investigate the incident. The inquiry concluded that the ship in question did not transport weapons from South Africa to Russia. The White House then issued a statement expressing gratitude to South African President Cyril Ramaphosa for the prompt and thorough investigation and affirmed its commitment to the African Growth and Opportunity Act (AGOA)—a preferential trade program that went into effect in 2000. But some legislators did not take the same stance as the White House—and there is an ongoing debate as to whether South Africa should be excluded from an AGOA renewal in 2025—either on political grounds or due to its status as an upper-middle-income country.

The dominant narrative has been that a loss of AGOA benefits would have disastrous consequences for South Africa. But there has not been a quantitative analysis to back this position. In our recently published research paper, Yash Ramkolowan and I used a computable general equilibrium (CGE) model to assess the economic impact of a loss of both AGOA and the Generalized System of Preferences, another initiative through which South Africa receives trade benefits with the U.S.

When AGOA first went into effect in 2000, South Africa’s economy benefited significantly. For example, South Africa increased its automotive exports to the U.S. from $195 million in 2000 to $1.8 billion in 2013. In 2000, South Africa exported a total of $2.2 billion in automotive exports and 8.7% of it went to the U.S. By 2013, South Africa exported $8.9 billion of automotives and sent 19.9% to the U.S. But over time, many benefits dwindled due to economic diversification and trade diversion. For example, in 2013, motor vehicles accounted for 25% of South Africa’s exports to the U.S. However, by 2022, this figure had diminished to approximately 10%. South Africa now directs almost two-thirds of its automotive exports to the European Union.

The impact of a loss of AGOA on exports and gross domestic product (GDP) would be small. Our model suggests that at worst, South Africa’s total exports to the U.S. would fall by about 2.7%. Certain sectors would be more affected than others. The biggest losses would be felt by the food and beverages sector, with exports to the U.S. expected to fall by 16%, and the transport equipment sector, forecasted to drop by 13%. The third and fourth biggest losses would be felt by the fruit and vegetable sector (-4.5%) and the leather and clothing sector (-3.6%).

In total, a loss of AGOA benefits would lead to a GDP decline of just 0.06%. This unexpectedly small effect is a result of two factors—the nominally higher tariffs on South Africa’s exports to the U.S. and the composition of South Africa’s export basket.

First, average tariffs (nonpreferential) remain below 5% for most products. As a result, exports to the U.S. without AGOA will not be much more expensive. Our model suggests that total production would fall by less than 0.1%. The effect would be most profound in the transport equipment sector, though this would still only lead to a 0.6% contraction in output.

Second, although the U.S. is South Africa’s second biggest trading partner (10% of total exports), the composition of South Africa’s export basket to the U.S. remains concentrated in goods that do not benefit from AGOA. Most of the export basket (just over 50%) to the U.S. is in the minerals and metals sector, which is not affected significantly by the loss of tariff preferences. Thus, a loss of AGOA would affect just a small share of the total 10% of South Africa’s exports to the U.S.

However, our computable general equilibrium model does not capture the potential impact of a loss of AGOA on investment and market confidence, both of which South Africa has struggled with in recent years. The RMB/BER Business Confidence Index (BCI) has been above the neutral midpoint (score of 50) for only two of the past 62 quarters, since 2008. This has been a driver in the loss in South Africa’s private sector investment—its gross fixed capital formation (investment) has declined from 18% of GDP in 2008 to 12% of GDP in 2022, one of the lowest levels of any emerging market. But the effects of a loss of AGOA on investment and confidence would depend on the reason South Africa lost the benefits. Stripping it on political grounds would be more impactful than losing it due to income status.

The possibility of South Africa losing AGOA preferences has been discussed for at least the last decade, given its status as an upper-middle-income country. However, South Africa’s recent foreign policy decisions have intensified these discussions. The narrative that a loss of AGOA benefits would have catastrophic consequences for South Africa is uninformed. Our research shows that the direct impact of the loss of AGOA preferences on South Africa’s export and economic growth would be very small, owing to the composition of the export basket, limited utilization of AGOA, and low (in aggregate) level of preferential margin afforded by these regimes.

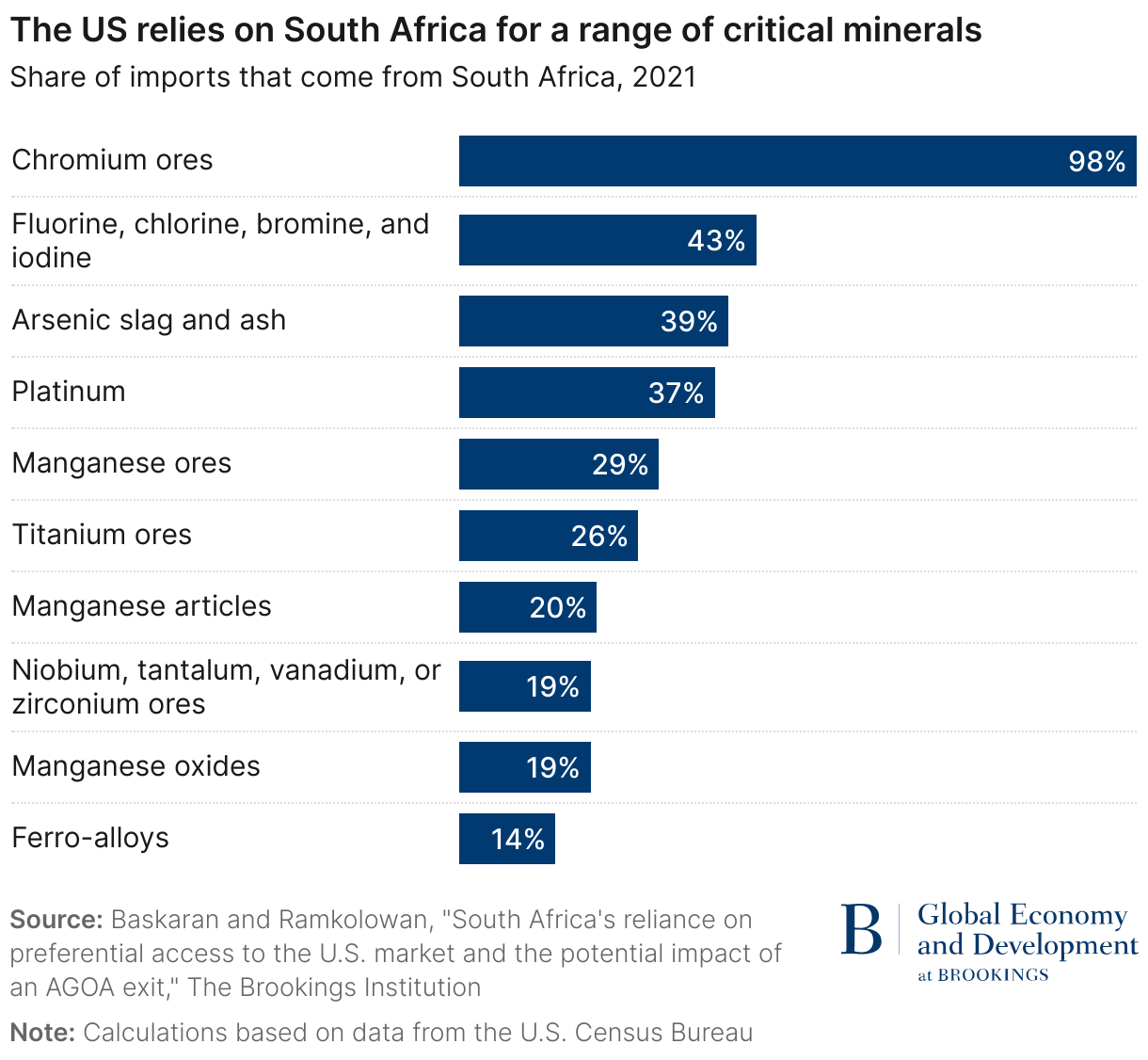

But a loss of AGOA could have ramifications for the U.S. The U.S. relies on South Africa for a range of critical minerals. In 2021, the U.S. imported nearly 100% of its chromium from South Africa as well as over 25% of its manganese, titanium, and platinum. Leveraging AGOA as a form of economic diplomacy is key for encouraging the security of critical mineral supplies.

The United States Geological Survey notes that South Africa is home to 70% of the world’s manganese—a critical mineral that is not substitutable. There has already been a significant increase in global demand for manganese: In 2021, South Africa exported $2.9 billion in manganese ore, and the production increase over the past decade has been significant, jumping 167% from 7.2 million tons in 2010 to 19.2 million tons in 2021. Export sales for manganese have increased 268% over the same period, from 9.3 billion to R5.3 billion rand.

South Africa also has over 80% of the world’s platinum. Given that it is a key input for vehicles powered by hydrogen fuel cells, demand is skyrocketing. In fact, 2023 was the first year in many that there was a global deficit, and some forecasts suggest this could increase by up to 1.5 million ounces in 2024—a threefold increase of 2023’s deficit.

A key finding of our paper is that policymakers should consider the inclusion of a critical minerals provision in a revised AGOA. Without it, AGOA is not notably beneficial to South Africa or the U.S., and weakening economic diplomacy may undermine future critical minerals security for the U.S.

Author

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Quantifying the impact of a loss of South Africa’s AGOA benefits

January 17, 2024