Surging unemployment claims show that our labor market, built for efficiency, can crumble in times of crisis at huge human and economic costs. The pandemic has exposed a weak point in the country’s economy: the precarity of low-wage workers. Many have adapted to unimaginable circumstances, risking their own well-being, implementing public health protocols, and keeping the essential bits of the economy, like access to food, running.

A lack of labor market protections exacerbates these workers’ insecurity and leaves the whole system fragile. Fifty-three million Americans, 44 percent of the labor force, earn low wages. In the best of times, these workers cycle more frequently from one job to the next without wage advancement. This lack of job stability causes financial volatility for households even when the economy is growing.

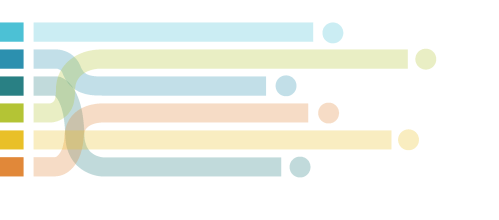

Workers’ tenuous connection to the labor market is reflected not only in the low wages they earn, but in the safety net available to them. We find that workers who earn low wages and do not have employer-sponsored health care account for 22 percent or 32 million of the country’s workforce. In a crisis, these workers are the least attached to their employer and thus the most likely to be laid off or have their hours reduced. And nearly 40 percent of them, 12.3 million individuals, work in the hospitality and retail sectors, the two sectors most immediately impacted by COVID-19-related layoffs (Figure 1). Not surprisingly, the United States is experiencing more job losses due to social distancing measures than other high-income countries.

Source: Brookings analysis of Emsi, OES, and ACS data.

Note: We define vulnerable jobs as those that pay less than the median wage and do not provide employer- sponsored health care.

Since the 1970s, low-wage jobs as a percent of total employment in the U.S. have increased while middle-wage jobs have declined, in part due to the loss of certain industries and profound lack of consistent education that would allow workers to learn job skills for the future. Many other high-income countries experienced the same dislocation of industries over this period, but their investments in education and employment support helped displaced workers and newcomers to the workforce adapt.

In addition, the poor quality of low-wage employment leads to a cycle of attrition and replacement that drives the labor market toward a less-than-optimal equilibrium with neither firms nor workers incented to invest in the job. This takes a steep toll on workers’ skills and opportunities for training: Low wage earners have little incentive to spend scarce time and hard-earned money building skills; meanwhile, employers, though frequently lamenting skills gaps, have little incentive to train workers who they expect to leave. The labor market arrives at a “low skill equilibrium.”

A modern benefits system

COVID-19 made explicit the consequences of this less-than-optimal equilibrium and broader worker precarity that is exposing the country to systemic risk. The pandemic is leaving economic disaster in its wake and laying bare a system in need of a reboot. As policymakers turn their focus from public health to the labor market, they can view the crisis as an opportunity to rebuild a more robust and responsive employment system for both workers and companies.

Political leaders and CEOs should not miss this calling.

A robust economic recovery hinges on at least two policy agendas: expanding unemployment insurance to protect workers through this and future shocks, and efficiently facilitating their reemployment. If in doing so companies and policymakers also raise the skill equilibrium and make work less precarious, the country will emerge more resilient.

Not surprisingly, the United States is experiencing more job losses due to social distancing measures than other high-income countries.

With respect to the first policy agenda, the federal government has taken steps that, though unprecedented in magnitude, could go further. Some of the expansions to unemployment insurance are set to end July 31, an arbitrary expiration date that will most likely not give sufficient time for people to get back to their jobs.

In contrast, in other high-income countries such as Germany, employees and employers have for decades made significantly larger mandatory contributions to unemployment funds that are ring fenced and provide a certain minimum wage replacement for a certain time in between jobs. They also have a fund that companies can draw on to adapt to downturns by reducing workers’ hours without greatly reducing their pay or benefits. Importantly, these programs benefit companies by reducing their costs of hiring and training new employees.

With private sector buy-in, policymakers in the U.S. can act now to put in place similar programs that, with funding over time, can prevent today’s tragedy in the future: 20 percent or more of U.S. workers losing their jobs and lining up at food banks.

When we turn to recovery and the second policy agenda—facilitating reemployment—portable benefits are another kind of modern scheme that can be adapted to assist workers’ economic mobility through training and career navigation. Portable benefits involve individual accounts to help workers accrue and access benefits even as they transition from one employer to the next, important especially for gig and contract workers who make up an increasing share of the labor force. The crux of these schemes is shared investment by workers, employers, and the state.

For example, Austria’s “backpack” model offers private sector workers portable severance pay, financed by employers who contribute a percentage of employees’ monthly pay to a fund that workers carry as they progress through their careers (like a backpack) and can redeem if they are laid off. Other examples include Singapore’s Skills Future credit system and France’s recent implementation of “personal training accounts.”

The focus on training will become increasingly important in recovery because the jobs available will likely look very different. Coronavirus is pouring jet fuel on top of a labor market already experiencing rapid technology-driven change. Public health measures are accelerating trends away from brick and mortar to online. Meanwhile, entire sectors are reassessing the costs and benefits of automation versus manual labor, and companies are building core-competency in lines of business that can be conducted remotely, further isolating the 42 million people without access to high speed internet.

No doubt there will be a high price tag attached to the programs described above. But a quality system, built over time with contributions from everyone, would have likely cost far less than the giant CARES package and additional stimulus packages likely to come, not to mention the costs of unemployment to firms—the lost know-how and ensuing hiring costs—and the costs of unemployment to broader society—increased crime and diminished community health.

There is an imperative but also an opportunity to emerge from this economic shock with a more decent labor market—one that assures living wages, safe work environments, a net that catches all, and a springboard that gets people back on their feet. Companies would win here too. But without a clear first-mover advantage, improving the equilibrium demands concerted policy action. We can invest to build a digitally savvy, surefooted workforce for the future, or risk furthering the gap between low-, middle-, and high-wage workers, ultimately missing the opportunity for a more resilient society.

Download the data used in this analysis

Martina Hund-Mejean is the board chair of the Mastercard Impact Fund and the former CFO of Mastercard. Marcela Escobari is a senior fellow at the Brookings Institution and leads the Workforce of the Future initiative, which receives support from the Mastercard Impact Fund.

Brookings is committed to quality, independence, and impact in all of its work. Activities supported by its donors reflect this commitment and the analysis and recommendations are solely determined by the authors.

Related Content

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Our employment system has failed low-wage workers. How can we rebuild?

April 28, 2020