In September of 2022, not long after Russia’s invasion of Ukraine, officials from the U.S. Department of Justice (DOJ) raided and seized several luxury properties in both New York City and Miami. The average person would have had little idea why these particular properties were special; the official register only listed an anonymous Panamanian shell company, one with a mailing address at Madison Square Garden, as the putative owner. But it was later revealed that the DOJ officials were part of KleptoCapture, a special task force created to seize and freeze the assets of Russian oligarchs, and that the true owner of the $70 million property portfolio was Viktor Vekselberg, a Russian-Cypriot billionaire who had been subject to U.S. sanctions for many years. Even though the authorities eventually pieced together the puzzle and located his gargantuan property portfolio, Vekselberg had managed to fly under the radar for years until that point.

The Vekselberg incident illustrates two alarming facts about American real estate. The first is that offshore investors can easily hide their identity by using opaque corporate ownership structures to keep their name off the register. The second is that, because this practice is so common, offshore investment in the real estate sector is likely far greater than what can be measured with public data.

Real estate has always been considered a risky sector, highly vulnerable to money laundering, tax evasion, and corruption. This is because high-value properties offer both a safe store of wealth and an asset that can easily be flipped for the purposes of laundering. It is also a sector that is very rarely subject to the same level of effective due diligence checks or automatic reporting requirements that financial accounts are. The true amount of money laundered through U.S. real estate is unknown, but recent reports by groups like the Anti-Corruption Data Collective and Global Financial Integrity have uncovered at least $2.6 billion worth of cases through both residential and commercial property in recent years.

These risks are amplified even further when the ownership originates offshore, as foreign authorities will struggle to spot instances of tax evasion or corruption when the wealth is hidden in U.S. real estate, with no public transparency of ownership. But to understand the risks that offshore ownership poses, we first need to understand just how much real estate foreigners own in the U.S.

Unpacking anonymous corporate ownership in three American cities

In new research, we used public data to attempt to measure offshore ownership in three major U.S. cities: New York City, Miami, and Boston. This work is part of a wider effort to measure offshore ownership in the largest, most popular cities around the world—part of the Atlas of the Offshore World. But while that initiative was able to estimate offshore ownership for big global cities such as London or Dubai, the black box of offshore ownership in the U.S. was much harder to pry open.

For each city, we attempted to trace the ownership of real estate using both publicly-available data on the value of each property as well as information on the direct owner of that property, including their name, mailing address, and whether they were likely a company. For New York City, we could push the analyses even further by matching companies to the New York State Registry, occasionally giving us the jurisdiction of the company rather than just its mailing address.

Through our analysis of each city, we uncovered the following three things:

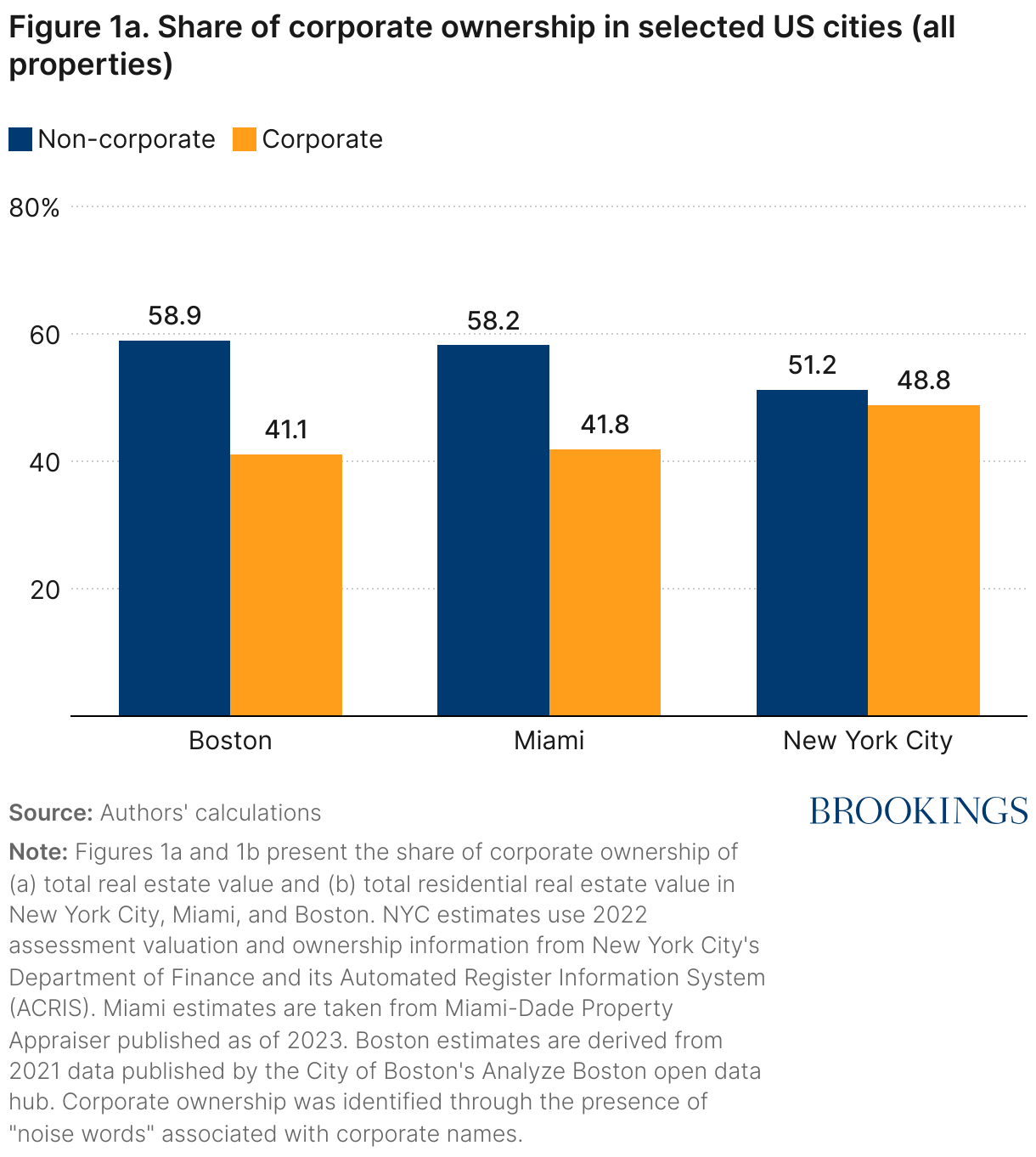

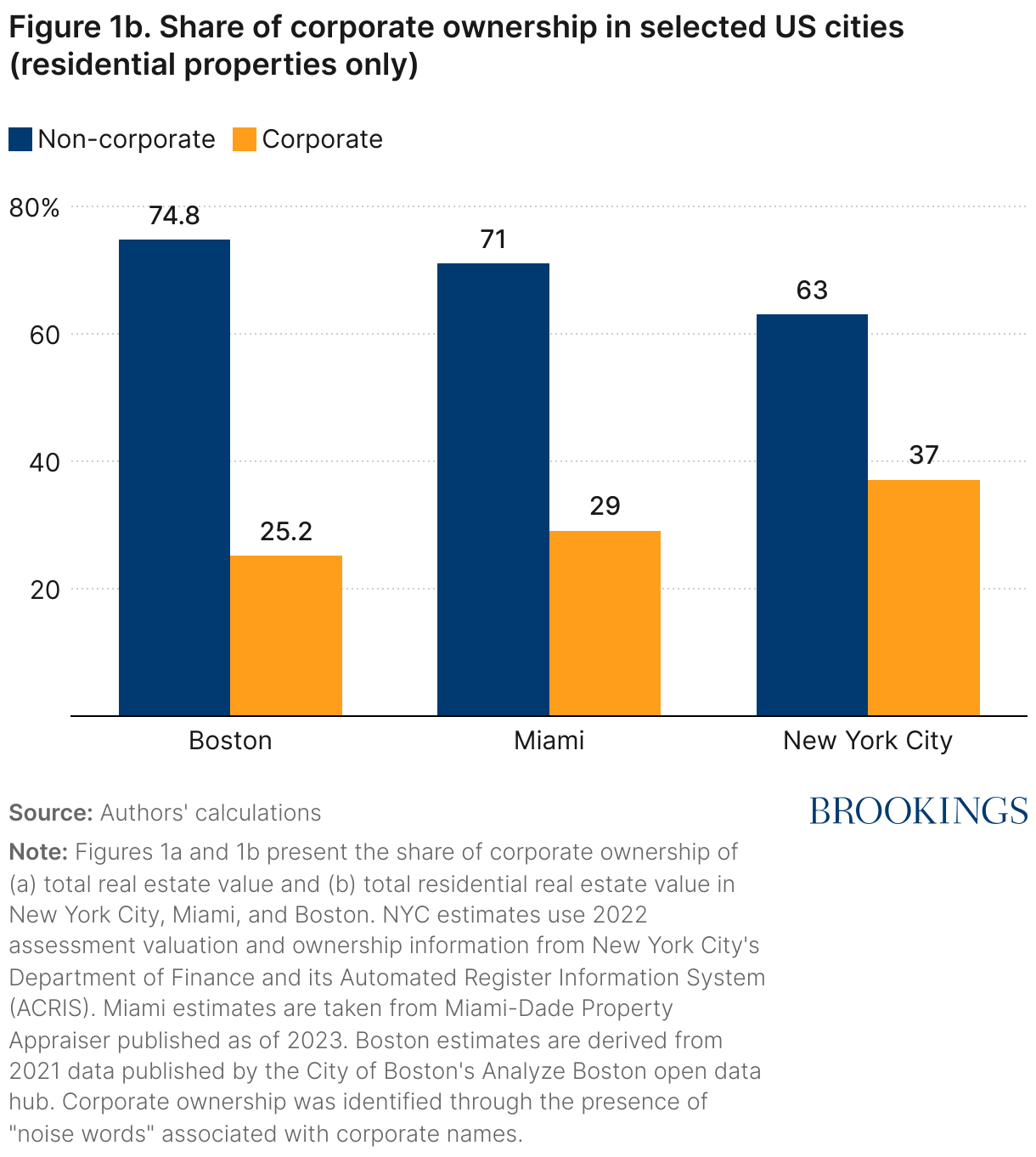

1. Corporate entities own a large swath of real estate in each city, particularly in the luxury market

Corporate entities own a large swath of real estate in each city, ranging from approximately 41% (in Boston) to nearly 49% (in NYC). Some of this dominance is due to the preponderance of corporate ownership in the commercial property market relative to residential. When we zero in on only residential properties, the share of corporate ownership drops to between 25-37% across the three cities. By our estimates, most of this value is held via limited liability companies (LLCs), which are more likely to be held anonymously. Out of all corporate-owned real estate in each city, roughly 71%, 68%, and 67% of the value is owned by LLCs in NYC, Miami, and Boston, respectively.

We also found that corporate ownership is more highly concentrated in the luxury market in each of our three cities. The probability that at least one owner of a residential property is a corporation increases dramatically as the price of the property exceeds the $1-2 million mark. For properties that are valued at $10 million and $100 million, the probability that a corporate owner is involved exceeds 50% and 80%, respectively.

Figure 2. The likelihood of corporate ownership increases with the value of the property

Note: The figure displays local polynomial estimates of the probability that a property is fully-owned or partly-owned by a company, as a function of that property’s assessed value.

2. Shell company ownership is twice as common for luxury properties, increasing owner anonymity

Neither companies nor LLCs are necessarily created in order to obscure one’s identity. But when we focus explicitly on shell companies—companies that are likely to have little to no economic presence and are often used to create anonymity—we find that they are about twice as likely to be listed as owners of high-value properties. Much of U.S. luxury ownership, then, is opaquely held through shell companies with no clear method of establishing who the ultimate owners of the properties are.

3. The public data suggests—improbably—that offshore ownership is close to zero

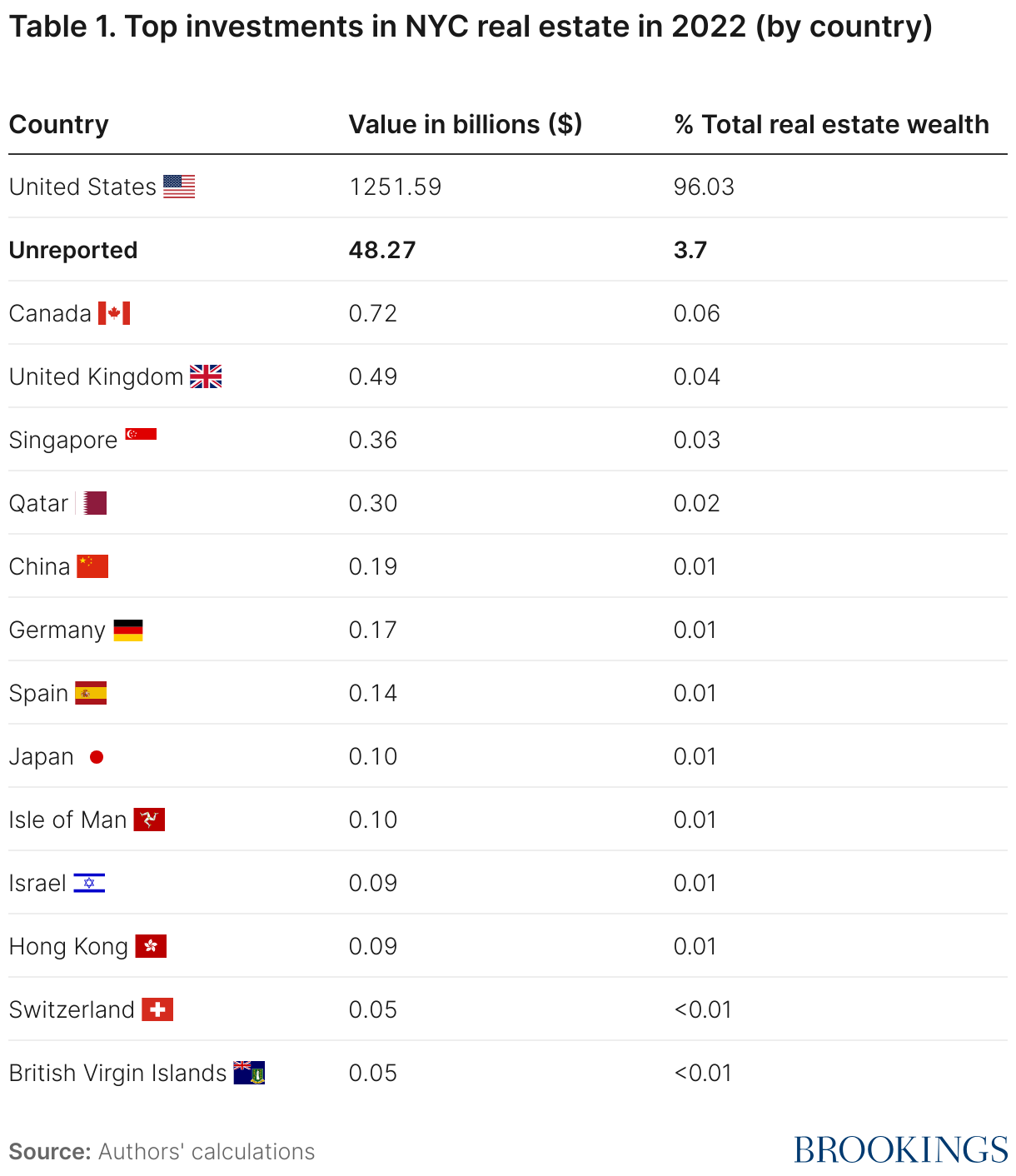

Lastly, and most importantly, ownership appears too “domestic,” in that there is far less direct foreign ownership than what would be expected given the popularity of these markets. Using NYC real estate as a case study and relying solely on public data, we can attribute only 0.27%, approximately $3.7 billion, of the total value of NYC real estate to foreign jurisdictions (Table 1). Over 95% of the value is allocated to entities within New York State, while the remaining 3.7% lacks sufficient information for jurisdictional allocation. This underscores how domestic corporate ownership may mask the true extent of foreign-held real estate, as “American-based” shell companies could be listed as such to obscure the identities of offshore owners.

We failed to open the black box, but the US Treasury has the power to do so

Our work highlights just how difficult it can be to identify the ultimate owners of real estate-owning companies in a setting where multiple, complex layers of ownership are common, and there are no standards in place for public reporting of beneficial ownership. At present, no U.S. state has created a public beneficial ownership register, although New York State will start implementing one next year. Often, for lack of such data, researchers turn to other sources, such as proprietary data on ownership like Bureau van Dijk’s ORBIS, or offshore leaks such as the Panama Papers. Yet both fall short of allowing us to understand who really owns U.S. real estate, as neither have detailed ownership information for the majority of American LLCs.

However, there is hope: Thanks to two recent policy innovations, American authorities will soon have enough intelligence to start measuring, in aggregate, how much real estate is owned by foreigners.

The source of intel is the U.S. Financial Crimes Enforcement Network (FinCEN)’s Geographic Targeting Order program, which since 2016 has been gathering beneficial ownership information for most corporate all-cash purchases of real estate in the largest cities in the country. The agency is also in the process of considering an extension of these reporting requirements to all residential real estate nationwide.

The second source is FinCEN’s beneficial ownership register for all U.S. corporate entities, launched earlier this year. By combining this beneficial ownership data with real estate registries published by cities like NYC, Miami, and Boston, the Treasury could quickly publish a comprehensive picture of foreign ownership of the vast majority of luxury properties in the country.

But there are good reasons to suspect that FinCEN, with only 350 employees and a budget only slightly higher than the Rock’s Jungle Cruise movie, lacks the capacity to quickly and regularly generate reports on the amount of offshore-owned real estate in the U.S.

We think there are several ways that the Treasury could break open the black box.

First, the government could take the necessary steps to make both the information obtained through its GTO program and via the Corporate Transparency Act publicly accessible in a machine-readable fashion, or at least accessible to parties with a justifiable interest. Aside from the other benefits that public beneficial ownership would bring (such as better verification of the underlying information), a publicly-accessible database would allow researchers to quickly understand who around the world has invested in U.S. real estate, and which markets may be the most at risk. The U.K. has already taken the step of making their data public, resulting in groundbreaking research on the scale of offshore ownership, a reduction in offshore investment, and discovery of multiple properties owned by sanctioned oligarchs.

Failing public access, FinCEN should open itself up to academic partnerships, much in the same way the IRS has done over the past few years. This would allow academics, who have a comparative advantage in crunching data and producing meaningful statistics, to produce public-facing, aggregate estimates of foreign-held real estate. And it would do so while maintaining the confidential privacy concerns that the Treasury and law enforcement currently have over the beneficial ownership data they have been collecting.

The Treasury has the ability to start shedding light on this phenomenon immediately. If they choose not to, then it will be up to states like New York to lead the way, through the implementation of public-facing beneficial ownership registries. Until either of these things starts happening, the black box will stay closed.

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Offshore ownership of American real estate is a black box. The Treasury has the power to open it.

August 13, 2024