The provision described in the report was adopted as part of the OBBBA legislation signed into law in the summer of 2025. (March 4, 2026)

Tucked into President Trump’s “One Big Beautiful Bill Act” (OBBBA) is a costly and ineffective provision that allows employees to repay their student loans out of their compensation tax free.

The tax expenditure was first enacted in 2020 and expires this year. Under current law, up to $5,250 per year of an employee’s compensation can be used to repay their student loans, and those payments are not subject to federal income or payroll taxes. Extending the student loan tax break would cost $11 billion over the next ten years.

When the provision was first debated, I argued that instead of providing relief for struggling borrowers it would instead be a windfall for high-income, white-collar workers who would have been able to pay off their loans without a tax break. There are two reasons for this:

- In order to benefit from the tax break, a borrower not only needs to be employed but must be working for an employer large and sophisticated enough to establish and sponsor a repayment plan.

- As with many “upside down” exclusions and deductions, the borrower’s tax savings depends on their tax bracket, with the highest-earners getting the largest break.

Data from the Bureau of Labor Statistics’ National Compensation Survey bear out these predictions: Benefits are indeed concentrated among high-income workers, in occupations requiring four-year degrees, and at large employers.

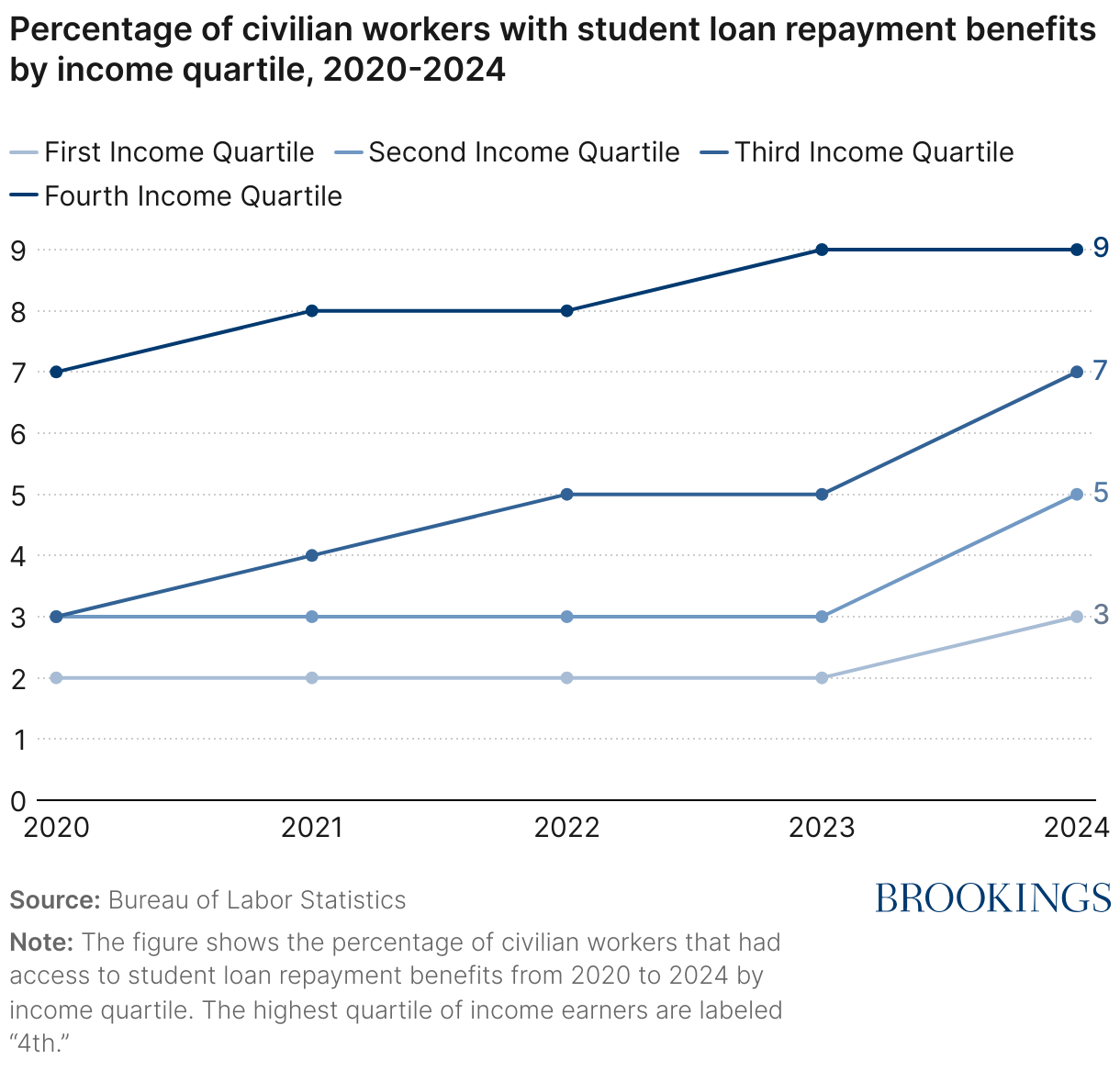

Student loan benefits are more common among the highest paid workers

High-income workers are significantly more likely to receive student loan repayment assistance from employers. As of last year, 9% of workers in the top quartile of the earnings distribution have access to student loan repayment benefits, compared to 3% of workers in the bottom quartile of the earnings distribution (Figure 1).

In other words, about 40% of the beneficiaries of the program are in the top 25% of the compensation distribution—among Americans who have jobs—and about 20% are in the top 10% of the distribution.

Simply put, the benefits of tax-free student loan repayment are concentrated among high-income workers. Contradicting the stated intention of the program to help struggling student loan borrowers, few workers at the bottom of the income distribution have access to this benefit.

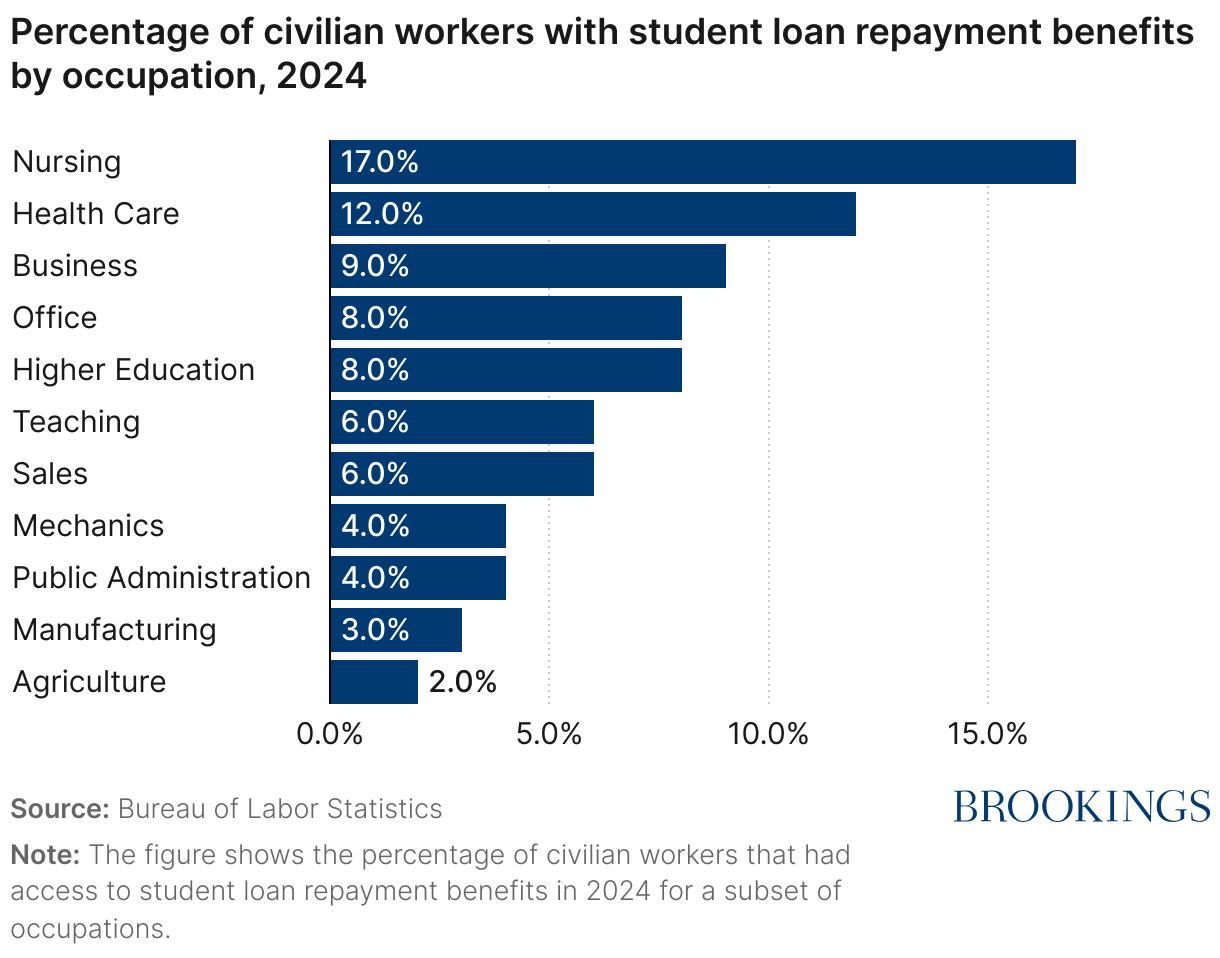

Student loan benefits are more common among well-educated, white-collar professionals

Nursing is the occupation with the highest access to student loan repayment benefits (Figure 2). This reflects the growing number of health care employers using student loan repayment benefits as a tool to recruit and retain employees. Nearly one in five nurses had access to employer-based student loan benefits. Other health care occupations are second, with 11% of workers receiving student loan repayment benefits.

Worker occupations that require less education are much less likely to have access to student loan repayment benefits. Fewer than one in 20 workers in manufacturing or mechanics have access to these benefits, while approximately one in 50 agricultural workers have access to these benefits.

Unsurprisingly, occupations with higher percentages of college-educated workers are more likely to have student loan repayment benefits as employers offer benefits that appeal to their workers.

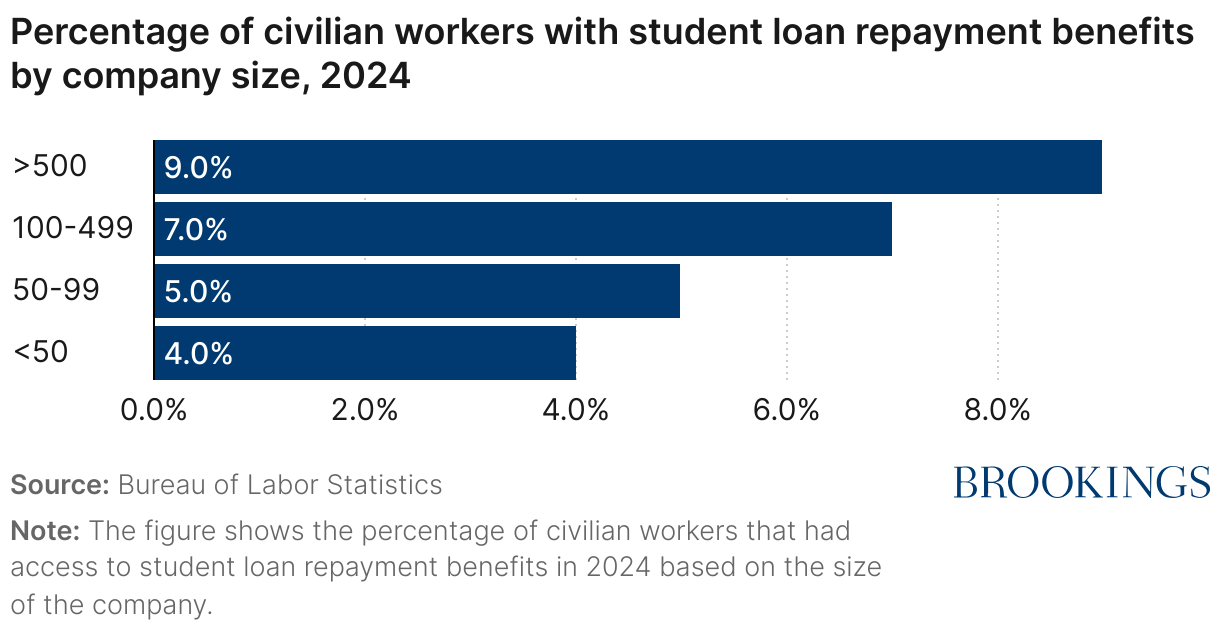

Student loan benefits are most commonly offered by large employers

In order to provide the tax benefit to employees, employers must establish an educational assistance program, which requires some level of sophistication and investment on the part of the employer. Setting up an educational assistance program requires the employer to establish a formal written plan, nondiscrimination testing, recordkeeping of eligible expenses, notice requirements for employees, and tax reporting.

As a result, larger employers are more likely to provide the benefit (Figure 3). In companies with less than 50 people, only 4% of workers have student loan repayment benefits. This percentage increases to 9% for workers in companies with more than 500 people.

Bottom line: access to this tax break varies significantly across workers depending on who they work for.

Congress has other options

Given the cost of this student loan tax break, which disproportionately benefits high-income, white-collar workers, Congress might consider other ways to use tax dollars to help student loan borrowers. One option is through income-based repayment plans, which are available to all borrowers regardless of their employment status or whether their employer offers a repayment assistance program. While these plans also have suffered from administrative challenges arising from burdensome application and recertification requirements, these issues are addressable with modest reforms. Despite these problems, use of these plans is far more widespread than the student-loan tax break, and income-driven plans offer a much better approach to reducing default risk and managing financial burdens on borrowers.

Authors

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

OBBBA would extend a student loan tax break that only benefits the best-off borrowers

June 24, 2025