Studies in this week’s Hutchins Roundup find that non-profit hospitals with more market power don’t provide more charity care, there has been a significant increase in the share of corporate saving globally, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Nonprofit hospitals do not provide more uncompensated care when competition decreases

Some argue that nonprofit hospitals should receive more favorable anti-trust treatment because higher profits would allow them to provide more public benefits. However, using data on California hospitals for 2001-2011, Cory Capps of Bates White LLC, Dennis Carlton of the University of Chicago, and Guy David of the University of Pennsylvania find no evidence that nonprofit hospitals are more likely than for-profit hospitals to provide more charity care or unprofitable services in response to an increase in their market power. They also conclude that government-run hospitals, rather than nonprofit hospitals, provide a disproportionate amount of uncompensated care.

Due to rising profits, nearly two-thirds of global investment is now funded by corporate saving

In the early 1980s, most global investment was funded by household saving; nowadays nearly two-thirds of it is funded by corporate saving. Using data for more than 60 countries, Peter Chen and Brent Neiman of the University of Chicago and Loukas Karabarbounis of the University of Minnesota find that global corporate saving (that is, profits that aren’t paid out in dividends) rose from less than 10 percent of GDP to nearly 15 percent of GDP over these years, and the corporate sector became a net lender of funds in the global economy. This shift in composition of savings reflects the “pervasive increase” of profits as a share of GDP rather than developments in particular countries, industries or firms.

Immigrant inventors in the U.S. may be more productive than their domestic counterparts

Patent records show that immigrants account for about 30 percent of inventors in the U.S. today, up from about 20 percent during 1880-1940. Ufuk Akcigit and John Grigsby of the University of Chicago and Tom Nicholas of Harvard find that technologies in which immigrant inventors were more prevalent between 1880 and 1940 experienced faster growth during 1940-2000. They also find that immigrant inventors were more productive during their lives – a larger total number of patents granted than native-born inventors – but received significantly lower wages.

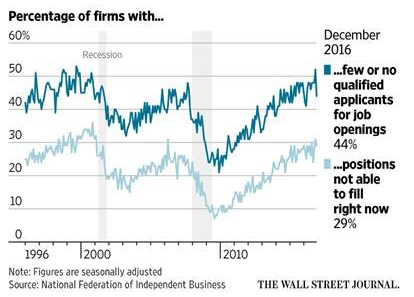

Chart of the week: As the labor market tightens, small businesses are having a harder time finding qualified workers

Quote of the week: “There is an open question about whether or who should supervise fintech lenders in the United States, made all the more complicated by the interplay between our state and federal regulatory frameworks,” says Philadelphia Fed President Patrick Harker.

“Most personal finance companies, for example, are licensed and regulated at the state level. Uncertainty about the boundaries between these two competing spheres of authority can be seen in some states’ reactions to the OCC’s proposal. But, particularly if we’re talking about loans to consumers, it’s only a matter of time until federal consumer protections will come into play. All of which is to say, it’s complicated. But it continues to be, in my opinion, in the interest of fintech companies to be regulated. This may sound like the particular nannying of a sometime regulator asking for more oversight. I’m not speculating at all that the Fed will be involved in fintech regulation. But I can say that none of us are trying to stifle innovation. If anything, you’ll hear us praise the ingenuity and imagination that comes from the technology sector. But there are risks, and we should be talking about them. Regulation can’t solve everything, and it can’t anticipate or guard against every problem. But it can try. For me, regulation is not just a question of protecting consumers; it’s a question of protecting the innovators as well. It’s in their best interest to have an established framework in which to operate. In part because the trust it engenders will underpin their essential role in the financial system.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Hospitals, corporate saving, and more

Thursday February 9, 2017