Studies in this week’s Hutchins Roundup find that the uncertainty about the macroeconomic outlook is considerable, unemployment increases opioid abuse, and more.

Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

All macroeconomic projections are highly uncertain

David Reifschneider of the Federal Reserve Board and Peter Tulip of the Reserve Bank of Australia use the historical forecast errors made by various private and government groups to analyze the uncertainty surrounding projections of real activity and inflation. They conclude that, if past performance is a guide to future accuracy, considerable uncertainty surrounds all macroeconomic projections. They also find that the Fed staff, Congressional Budget Office, Blue Chip consensus and other forecasters have been equally accurate in their predictions. Finally, they show that estimates of uncertainty about future real activity and interest rates are now significantly larger than before the financial crisis, while estimates of inflation accuracy have changed little.

Fluctuations in the local unemployment rate are linked to opioid deaths and hospitalizations

During 1999-2014, the death rate from drug overdoses in the U.S. rose by 203 percent among whites. Using county-level mortality data for the entire U.S. from 1999-2014, Alex Hollingsworth and Kosali Simon of Indiana and Christopher Ruhm of the University of Virginia find that when the county unemployment rate increases by 1 percentage point, the opioid death rate rises by 3.6 percent and the emergency department visit rate for opioid overdoses increases by 7.0 percent. These findings are not restricted to periods of recession and are primarily driven by adverse events among whites, they find.

Interest rate cuts have smaller effects on bank lending when interest rates are already low

Using data on 108 large international banks, Claudio Borio and Leonardo Gambacorta of the Bank for International Settlements find that, when interest rates are low, reductions in short-term interest rates are less effective in boosting bank lending. This result does not stem from the impact of a financial crisis on banks or weakness in loan demand. Rather, it likely reflects the negative impact of low rates on the profitability of banks’ lending activities, the authors conclude.

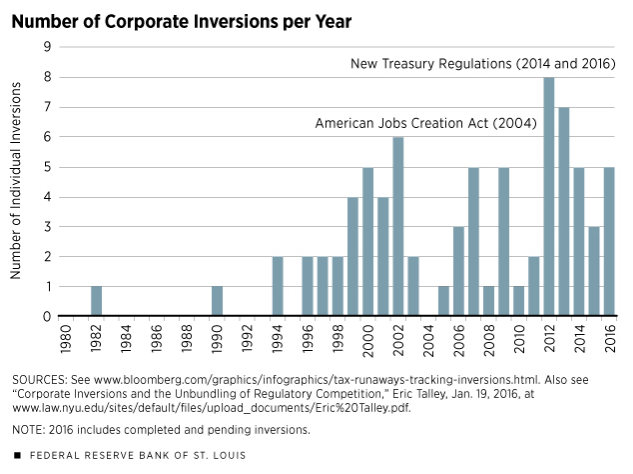

Chart of the week: Tracking the ebb and flow of U.S.-based multinationals moving their corporate Headquarters overseas

Quote of the week: “If we become more confident about the economic outlook, that the recovery will be sustained, then… that might make me a little bit more comfortable to proceed with balance sheet normalization a little bit more quickly,” says New York Fed President William Dudley.

“I think the important thing here is that when balance sheet normalization occurs and we start to end the reinvestment, don’t think of it as an active tool of policy. Think of it as a passive tool, number one. And number two, to the extent that we then do decide at some point in the future to taper or end the reinvestment, that will also be a way of removing accommodation. And so that would be a bit of a substitute for raising short-term interest rates. So, I would guess, my own personal view, is if we move to balance sheet normalization, that might actually stretch out the process of raising short-term interest rates a little bit because the two are substitutes for one another in terms of removing monetary policy accommodation.”

Related Content

Related Books

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Hutchins Roundup: Forecast uncertainty, opioid deaths, and more

Thursday, March 2, 2017