Facing a pandemic-triggered economic slowdown, U.S. school districts now need to consider doing something they haven’t had to do in recent budget boom years: Draft a budget that assumes they’re headed for a financial fall.

Why? More than ever, school districts rely on state money. In many states, much of the state revenue comes from income and sales taxes—both of which abruptly collapsed when states shut down most business activity. While most districts will see little impact on their 2019-20 budget, it’s next year (2020-21) when leaders should expect state revenue shortfalls to hit district budgets.

Already, states are draining their rainy-day funds to address critical pandemic needs. Looking to next year, K-12 education will be competing for fewer state dollars against priorities like emergency public health, Medicaid, and higher education (which tends to see enrollment rise as the economy falls). At about $270 per K-12 pupil, the recently passed federal stimulus package will likely fall far short of filling the inevitable fiscal gaps.

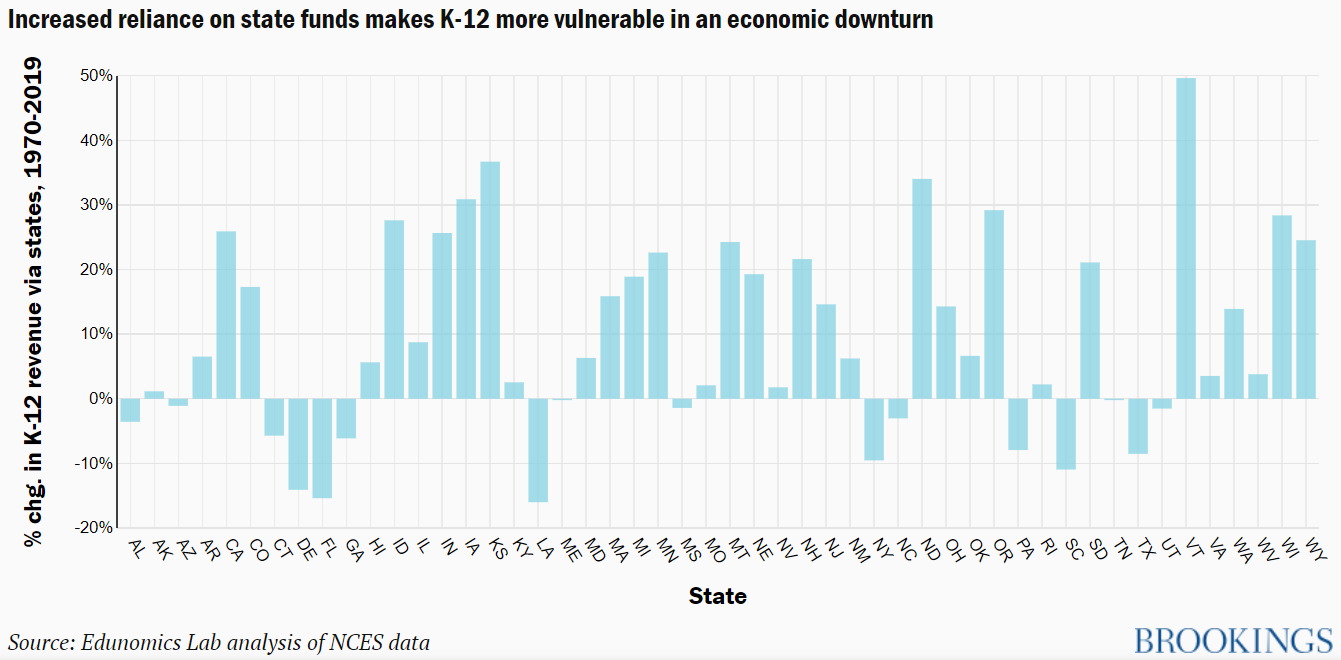

It wasn’t always the case that school district funding was so tied to the economy. Local schools used to be fairly insulated from economic downturns because they relied largely on local property taxes, a highly stable revenue source. Of course, funding schools on property wealth makes for huge gaps between wealthy and poor communities. So, in the name of greater funding equity, most states now play a much bigger role in funding schools. While the pattern has been playing out over the decades, it has continued in recent years with new state formulas in Illinois, Indiana, Washington, and Kansas, all designed to address inequities among districts. Analysis of the state share from 1970 to 2019 demonstrates that in 34 states, the share of K-12 revenue coming from state sources has grown from decades past. This information is displayed in the figure below. (Mobile users: Click here to open this figure in a new tab.)

In doing so, many of these states have effectively traded K-12 revenue stability for greater funding equity. This little-discussed dynamic raises big questions as the education sector starts to grapple with the financial implications of the coronavirus-sparked economic slowdown.

Multi-year commitments make for sluggish K-12 responses

While state revenue expands and contracts with the economy, the districts relying on this revenue behave as if they were still in a protective fiscal bubble. Districts often commit years in advance to teacher pay raises—commitments that are insensitive to changes in the economy or surrounding labor markets. In most private sector industries, employers adjust compensation plans quickly such that workers forego pay raises in a recession. But in K-12 education, teacher pay raises are baked in years down the road through collective bargaining agreements and automatic pay bumps from things like seniority, advanced degrees, and National Board Certification. For example, in 2008-09, right after the onset of the Great Recession, Seattle teachers received a 14% pay increase. With built-in cost escalators, districts box themselves into a framework that makes it harder to strategically flex their spending in response to economic (and therefore, revenue) shifts.

At the same time that state-provided K-12 monies are increasingly vulnerable to economic downturns, state-administered pension payouts to public education retirees are entirely insulated from them. Unlike in the private sector, most public educator retirement plans guarantee fixed payouts based on final average salary, regardless of the investment returns the pension fund earns—or loses.

Deeper budget gaps can eventually prompt layoffs

Initially, districts typically start with belt-tightening cuts such as hiring freezes, eliminating travel, canceling vendor contracts, or adopting “efficiency” measures that save on utilities and the like. They then move to eliminate what the system knows it can live without, such as any newly added programs or services. But none of these budget changes amount to much in the way of savings. Labor makes up 80 percent of K-12 costs, so if the gaps are significant, districts will ultimately have to cut personnel. Take Nevada’s hard-hit Clark County School District, which laid off more than 500 employees in a single year during the Great Recession.

Recessions bring inequitable impacts across schools, districts, and states

If K-12 systems do institute layoffs, the layoff policies will matter. Notably, layoffs of junior teachers disproportionately impact high-poverty schools, which tend to have a higher share of such teachers than more-affluent schools. Those layoffs would come at the worst possible time for high-poverty schools, as even more students fall into poverty and need more from schools as their parents and guardians lose their own jobs.

And where a state funding formula is designed to bring more state dollars to those districts that can collect fewer funds from local sources, a reduction in state revenue could translate to deeper cuts for districts with lower property values. For instance, New York’s Rochester City Schools rely on the state for more than 75% of the district’s funding, whereas Scarsdale Union gets more than 90% of its money from local sources.

Just as the looming financial shortfall won’t be equally felt in all districts, it won’t be equally felt in all states. Where states rely more heavily on property taxes (versus sales and income taxes) or where their economy is less affected, state coffers may see less shortfall. The last recession was a first in that it brought federal rescue funding for K-12 education. The recent CARES Act came with lower levels of funding for K-12—although there is already talk of more federal funding in the months to come. But even where federal stimulus funds help, the challenge of a federal stimulus is that it tends to treat all states based on a formula that has nothing to do with the relative depth of revenue loss in the state. And in fact, the CARES Act funding is applied in proportion to each state’s Title I formula (primarily driven by census counts of student poverty). If future stimulus follows the same pattern, it is clear that some states will be left with deeper unfilled gaps than others.

Is this a pattern destined to repeat itself with every economic downturn?

Now that we’ve built an education funding structure that’s more susceptible to economic shifts, the big question for public education is: What’s the “new normal” when we hit a downturn? Maybe a federal bailout becomes the norm. Or is part of the problem that school systems are making multi-year financial commitments when revenues are so dependent on the economy? Should we be asking school systems to adjust their practices so that they can be more nimble—tweaking salaries and expenditures on an annual basis? If so, perhaps now is the time to make future stimulus funding contingent on financial reforms that leave systems in better shape come the next economic downturn.

If not, the cycle is destined to repeat: economic slowdown followed by financial upheaval in districts, followed by pleas for federal money—without which students will be left to pay the price.

Correction 4/17/2020: An earlier version of this post cited inaccurate figures of K-12 state funding from a narrower time period, though the overall trend described remains valid. The revisions correct the data and references to it within the text and within the figure.

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

{kind=link}