The true character of society is revealed in how it treats its children.”

Nelson Mandela

Elected officials of both parties have proposed new and better government support for families with children. President Trump’s One Big Beautiful Bill Act includes some of these proposals, but overall, because of the law’s benefit cuts for working class and lower-income families, it will likely end up hurting roughly as many families with children as it helps.

- Parts of the law increase help for families with children: The maximum Child Tax Credit was increased from $2,000 to $2,200 per child; however, the increase remains only partially refundable and thus will not be available to many low-wage working families. In addition, on a much smaller scale and with some questions remaining about its workability in practice, the One Big Beautiful Bill Act (OBBBA) created a new type of child savings, “Trump Accounts,” and a temporary program of $1,000 payments for each child born in President Trump’s presidential term. The adoption credit has also been improved. In each of these provisions, there are further changes that could enable these programs to help more children and more families.

- However, many of the law’s most substantial changes will reduce help to children, particularly those in working class and poor families. The law imposes new legal and bureaucratic filing requirements to previously bipartisan programs, particularly the Supplemental Nutrition Assistance Program (SNAP, formerly known as “food stamps”) and Medicaid, that will keep many families from getting benefits, including benefits for which they are eligible.

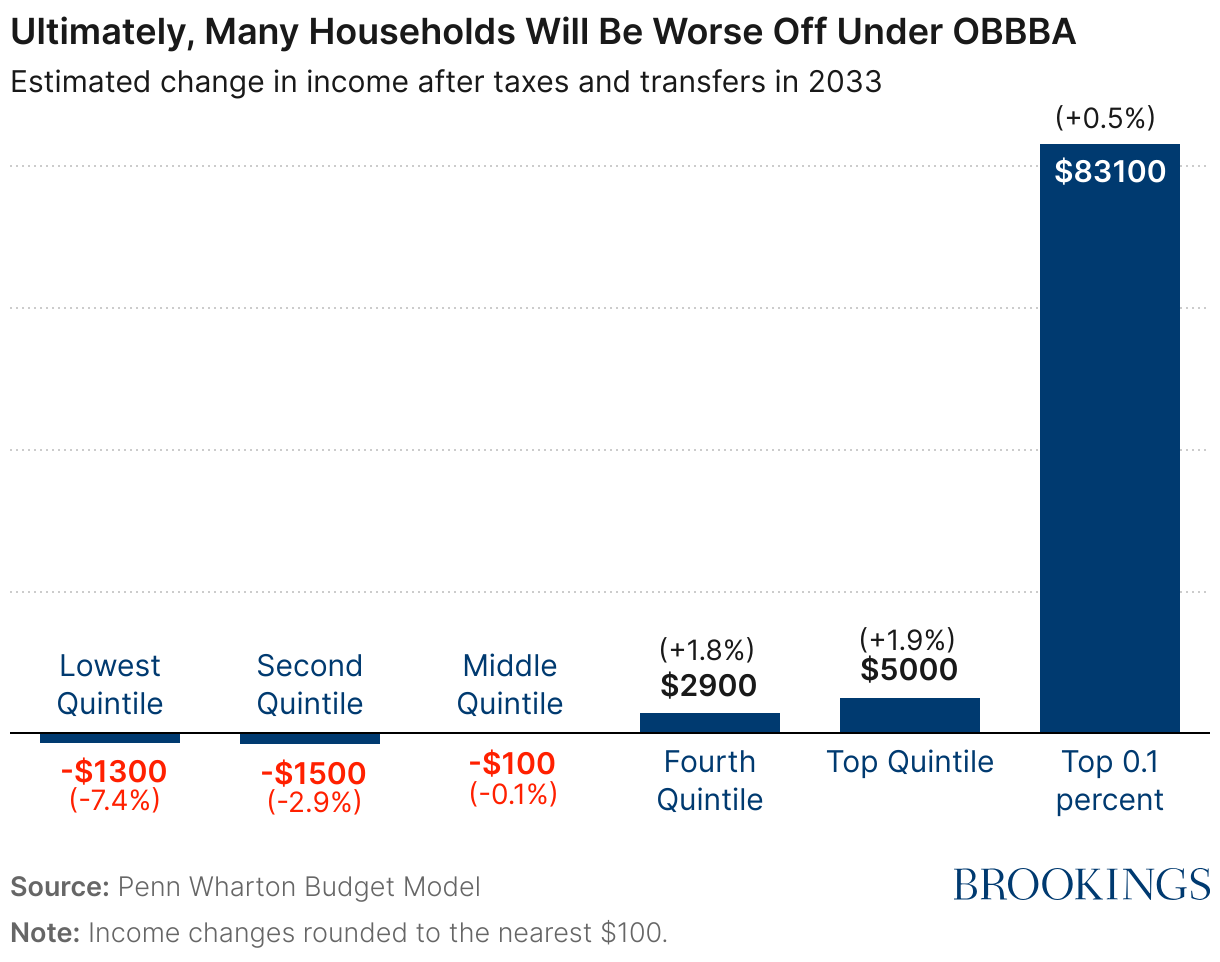

- Overall, OBBBA will likely end up reducing benefits for roughly as many families as it helps, with the greatest losses concentrated among the least well-off. By 2030 the 40% lowest-income households will experience a net loss on average, and the middle quintile will have roughly no net change; there will be ongoing net gains for the top 40% of households.

This note describes some key changes embedded in OBBBA, some related proposals by Democrats, and some improvements that might be made in the future.

Is child policy becoming bipartisan?

Politicians of both parties, who once made a show of kissing babies, have progressed to making a range of proposals to improve children’s lives and prospects. In some cases, perhaps frustrated by ongoing political polarization, they’ve chosen to support the same or similar approaches, including extra tax credits or actual payments for children and child savings accounts. For example, both Senator Ted Cruz (R-TX) and Senator Cory Booker (D-NJ) have proposed savings accounts be started for every child at birth.

Although the recently enacted OBBBA was in no way bipartisan, it included some proposals endorsed by both Republicans and Democrats. At the same time, however, the Act reduced the scope of the previously bipartisan SNAP safety net program and of Medicaid.

Furthermore, despite claims by representatives of both parties to support working families with children, the changes in OBBBA overwhelmingly help families that are already better off. After the temporary tax benefits end, roughly half of U.S. families will be worse off, with most benefits of the bill going to the top 40% of the income distribution.

Below, we discuss two kinds of assistance for families for children: those that provide immediate resources and those that support saving for children’s futures.

Money for children now: Child income tax credits, baby bonus checks

Congress has subsidized children through the tax code for at least a century, starting with dependent exemptions from income1 and following with the Earned Income Tax Credit in 1975 and the Child Tax Credit (CTC) in 1997. By far the most significant action benefitting some children in OBBBA is an increase in the CTC. However, most low-income children are excluded from these higher benefits. At the same time, the Act would dramatically reduce other previously bipartisan safety net programs that support low-income children, particularly SNAP.

Child Tax Credit

The CTC is a tax credit for families with children. It was originally conceived as an anti-poverty program, though for much of its history most of the CTC’s benefits have gone to middle class or wealthier families. The CTC phases in with earnings and the credit is only partially refundable, meaning that if the credit exceeds a filer’s tax liability, families can receive a portion of the credit as a tax refund. Approximately 60 million children benefit from the current credit. In response to the COVID-19 recession, for one year the credit provided families with as much as $3,600 per child and allowed low-earnings families to get the full benefit, but that expired and the maximum returned to the pre-OBBBA maximum of $2,000. Because of the phase-in and other limitations on refundability, an estimated 17 million children in families with low incomes receive less than the full $2,000-per-child credit or no credit at all.

OBBBA Changes

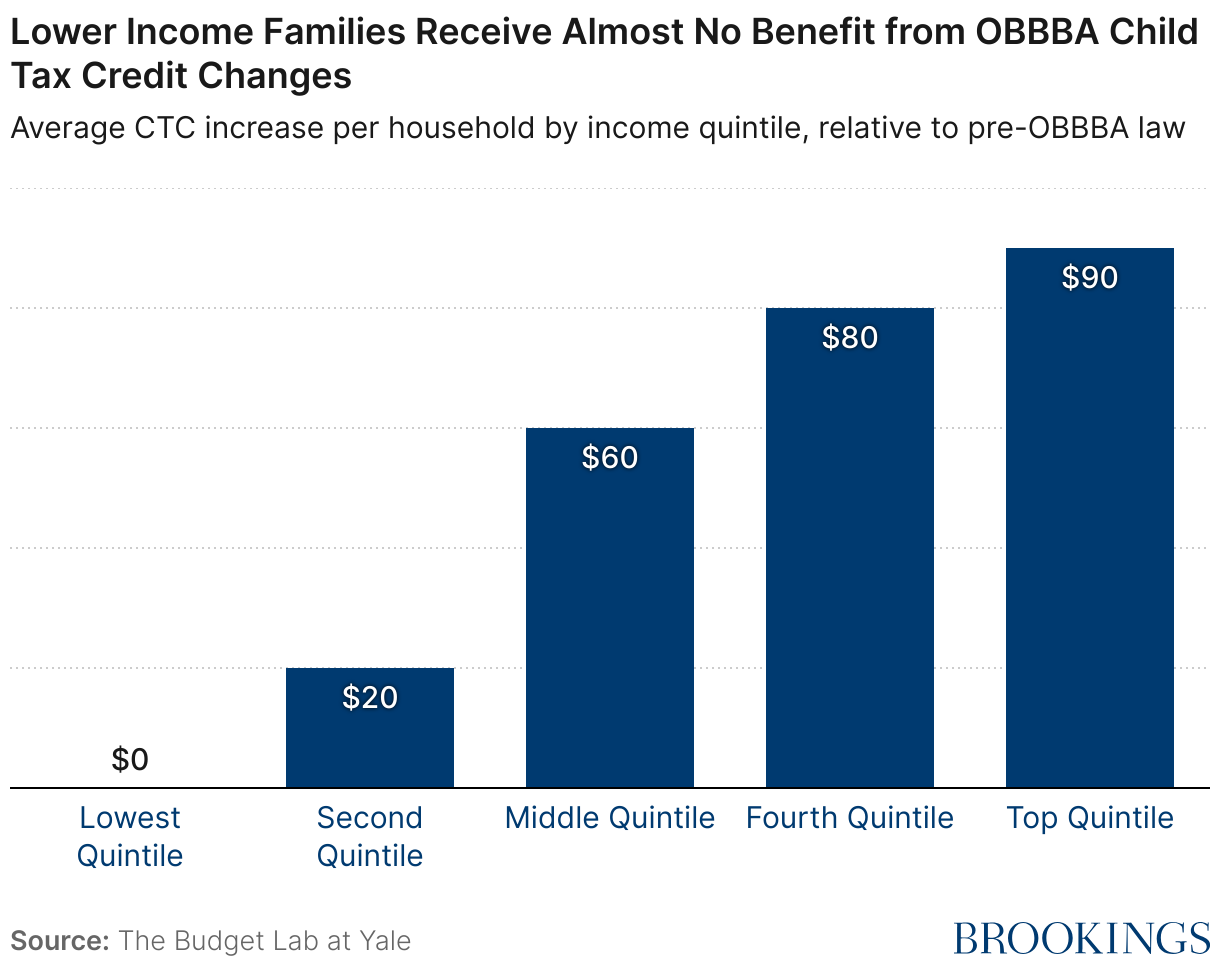

Under OBBBA, the maximum credit was raised to $2,200 per child and then indexed to inflation. Because the bill did not make any changes to the CTC’s refundability or phase-in with earnings, this change will not benefit any of the estimated 17 million children who were left out under pre-OBBBA law. Furthermore, the act’s increase in the standard tax deduction and other changes will increase the number of children whose families don’t get the full credit.

The OBBBA CTC expansion primarily benefits families with above average income. As this graph from the The Budget Lab shows, the bottom 40% receive little or no benefit.

Possible Improvements

There are many possible changes to broaden the CTC’s reach and help more children. (See Crandall-Hollick, Maag, & Jha 2025.):

- CTC “Baby Bonus”: Make the full credit available for all newborns, so that every newborn child’s family would get the full credit for their first year. This could be considered a CTC-based “baby bonus”.

- Allow full refundability as long as parent earnings are above the minimum ($2,500/year).

- Start phasing in refundability from the first dollar of parent earnings.

- Allow full refundability for families with multiple children.

Adoption Credit

Under current law, adoption expenses of up to $17,280 per child can be credited against income taxes. In practice, few families get the full credit because the credit is nonrefundable and few families have an income tax bill greater than this amount.

OBBBA Changes

Under OBBBA2 up to $5,000 of qualified adoption expenses will be refundable, thereby increasing the available adoption credit for approximately 45,000 children per year.3

Possible Improvements

Congress could broaden the benefits of the adoption credit by reducing the total credit and increasing the refundable amount, e.g., reducing the maximum to $12,000 while increasing the refundable amount to $6,000.

Direct cash grants: “Baby Bonuses,” SNAP, etc.

Some observers, concerned about declining birthrates, have proposed a cash payment for newborns soon after birth. Although President Trump has expressed support for a $5,000 “baby bonus”, the administration made no specific proposal and none was included in any version of the OBBBA. (A baby bonus could be implemented via a change in the CTC, as described above.)

Important safety net programs affecting children were cut by OBBBA

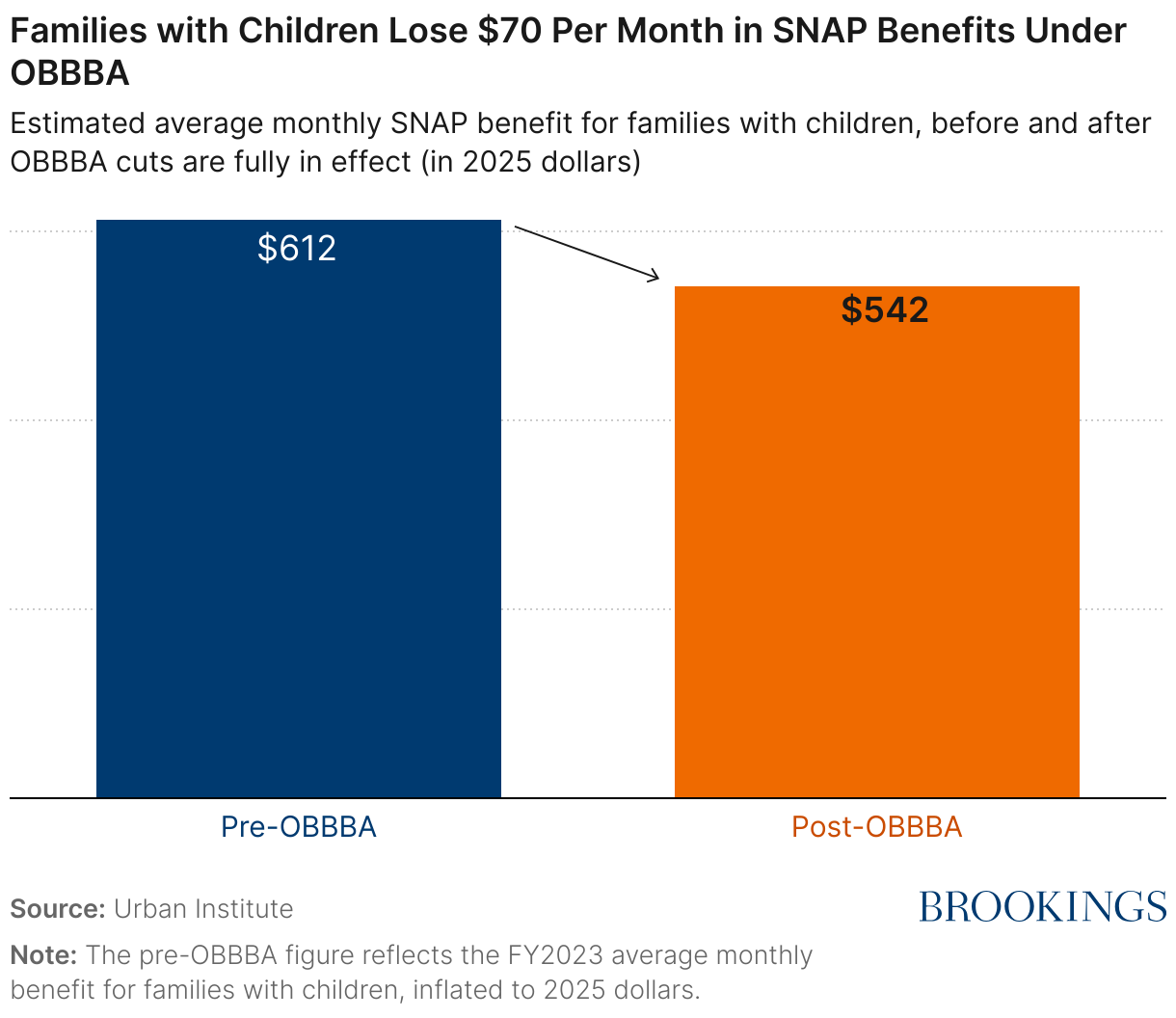

There are many federal safety net programs that provide cash or in-kind benefits to families based on having children and the number of children. The largest near-cash program, SNAP, will be cut back very substantially by OBBBA. An Urban Institute report estimated that the SNAP cuts would affect 3.3 million families with children and reduce their benefits by an average of $840 per year.

Money for children’s futures: Baby bonds & Trump child savings accounts

With multiple rationales, policymakers with varying perspectives have concluded that children and their families would benefit from starting life with a nest egg, a savings account to be created early in a child’s life, to be then held and used well in the future for education, homebuying, or other purposes. States, cities, counties, and nonprofits have started programs that both establish child savings accounts and provide a starter contribution to those accounts. According to the Congressional Research Service, over 100 such programs had been started by 2023, in addition to the education savings account programs operated by many states under Section 529 of the Internal Revenue Code.

These programs draw from work in the early 1990s by academic Michael Sherraden which proposed a national program of “Individual Development Accounts” for the poor. This led to local programs in many cities and some states. A similar approach using the term “baby bonds” was proposed by scholars in 2010 as a means to reduce racial gaps in wealth, and this proposal was adapted into the American Opportunity Accounts Act introduced by Senator Cory Booker (D-NJ) in 2018. Under those proposals every child would receive a grant at birth, with additional government grants to children in poorer families in later years. Some child investment programs, such as New York City’s RISE program also incorporate philanthropic gifts.

The approach became bipartisan this year when Senator Ted Cruz (R-TX) proposed that each newborn child receive a one-time $1,000 grant in an “Invest America Account.” Cruz’s rationale was less about reducing wealth disparities and more that such accounts would give children a stake in the future and an understanding of investment markets. In place of ongoing government contributions, he proposed that parents, employers, philanthropies, and others could contribute to the child accounts. The Cruz proposal was, with modifications, adopted in OBBBA.

What are the benefits of child savings accounts?

Advocates of these accounts see several advantages. First, they note with some evidence that having a personal account early in life that can only be accessed later substantially increases a child’s and family’s interest in education and personal betterment. Some believe that these accounts will also improve financial literacy and understanding of the economy and investment.

Other advocates, noting that disparities in wealth are associated with differences in educational opportunities, attainment, and future income and that wide racial differences in wealth persist, believe these programs could reduce wealth disparities at the start of life. The original child savings programs focused on this rationale, with payments or participation incentives that favored the poor. There is research that finds higher wealth associated with better educational and health outcomes, as well as stronger protection against material hardship following disruptive events, suggesting that policies that facilitate wealth-building could have profound effects.

OBBBA’s Trump Accounts & $1,000 contribution pilot program

OBBBA permits4 the secretary of the Treasury and/or private financial institutions to offer “Trump accounts,” savings accounts for children under 18 that offer some limited tax benefits if invested and not used until age 18. Contributions to these accounts, limited to $5,000 per year from family members, would be taxed as ordinary income. In addition, there is a 10% penalty for withdrawals before age 59½, with certain exceptions for education, home buying, adoption, disaster relief, etc. Contributions are also permitted from employers, up to $2,500 per year, and as part of a general program from government or philanthropies supporting all children in an approved geographic area.

The act also creates a pilot program of $1,000 government grants for any child born in the years 2025-28 (with a Social Security number) if the parent or Treasury elects5 and if there is an account established for that child. Although the government funds to be provided are given only at birth and are generally much smaller than the CTC, if made universally available they will reach some poor families with children that the Child Tax Credit does not.

Will Trump Accounts work?

While both Republicans and Democrats have endorsed at least the outlines of child savings accounts and a universal starting grant, there are many potential supporters who have questioned the design of Trump Accounts as enacted by Congress. A comprehensive review of child savings accounts systems undertaken by the Aspen Institute’s Financial Security Program raised a series of challenges, only some of which were responded to by the Congress. The Aspen publication noted ominously that similar program in the U.K. had been regarded as a failure and had in effect “poisoned the well” so that other efforts were unlikely to be considered for many years. That may have been a warning for Trump accounts.

Making Trump Accounts and the $1,000 per newborn pilot program work will require:

- Treasury to encourage all new parents to sign up for (“elect”) the $1,000 grant and/or the Treasury can do so itself. OBBBA does not auto-enroll children. It requires either the parent or the Treasury to “elect” newborn participation in the grant program.

- Treasury to establish and pay for the millions of accounts for all newborns. Although the law permits private financial institutions to establish these accounts, in practice they are unlikely to do so on their own. The administrative costs of setting up millions of individual private accounts will be large and, after receiving the $1,000 initial grant, many families will conclude that they cannot afford further contributions. Private firms will see little benefit in maintaining millions of individual accounts holding $1,000 with little prospect for more contributions. For that reason alone, Treasury will likely need to set up the program at least initially, perhaps by managing the funds in a single investment pool and having the individual accounts administered centrally. Treasury may also have to subsidize at least part of account administrative costs.

For those families that can afford additional contributions, the existing nationwide programs of tuition savings accounts (“529 Plans”) are likely to be preferred: Investment earnings within Trump Accounts will be taxed at the ordinary income tax rate (plus a possible 10% penalty unless used for approved purposes), whereas proceeds from 529 plans if used for tuition expenses are not taxed at all.

Possible changes

Since the program has the president’s name on it, Treasury is likely to make every effort to help Trump Accounts succeed and be widely adopted and used. Some changes have already been suggested:

- Provide additional government contributions for children of less well-off working families. This could be done several ways: Under the approach proposed by Senator Booker, the government could make smaller grants annually to children in families below an income limit. Alternatively, this could be done by allowing a full refund of the Child Tax Credit regardless of income while requiring the increased refund be invested in a Trump Account or something similar.

- Ensure that child savings don’t penalize other public support. Retirement accounts and tuition assistance 529 program savings are generally not considered assets in setting eligibility for SNAP and other programs, and they are given preferential treatment in determining student loans. Trump Accounts could get similar treatment, as the Aspen Institute working group proposed for early wealth building policies.

- Consolidate the many different tax-favored savings accounts into a single account type. (Muresianu & Cluggish, 2025) Since the Trump accounts are in some respects tax-disadvantaged compared to 529 school savings and also to several retirement accounts, a way to ensure the success of the effort might be to incorporate those accounts into the Trump account program.

What’s the right balance between helping children now versus saving for the future?

Unsurprisingly, there are differences of opinion whether additional resources should be devoted to immediate financial relief (using the CTC or a child grant) or instead to child savings accounts and wealth building for the longer term. There are advocates of both approaches and both have been shown to benefit children and families. However, there isn’t yet enough experience with child savings accounts to form judgments about the appropriate balance of resources between them.

We can do better

Given the broad public support to help children and families with children, elected officials from both parties will claim their efforts do so. As the distinctly non-bipartisan experience with OBBBA shows, however, many programs fall short of the rhetoric: overall, OBBBA seems likely to harm as many families with children as it helps.

Future bipartisan efforts can and should do better, supporting all families with children, including those who are more in need.

Related Content

Authors

-

Footnotes

- The dependent exemption was replaced by a larger standard deduction in the Tax Cut and Jobs Act of 2017. That standard deduction was increased in OBBBA.

- Section 70402.

- JCT estimated $2.3B over 10, which would be 45k children per year at $5k each.

- OBBBA does not require either the secretary or private financial firms to offer Trump Accounts. OBBBA §530A(b)(1)

- There have been press reports that the contribution is automatic, but this is not accurate – see bullet point below for details. OBBBA §1634(a).

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

How children are treated in the One Big Beautiful Bill Act

October 21, 2025