Last month, the International Monetary Fund published its regional economic outlook for sub-Saharan Africa, which seeks to answer the question: What does the post-pandemic road to economic recovery look like?

While no sub-Saharan African country has avoided the pandemic, cases have dropped substantially after peaking in July (Figure 1). This trend stands in stark contrast with the movement seen in advanced countries elsewhere in the world, which saw a nadir in cases in June and have peaked in recent months. However, though the acute impact of the pandemic has been receding, the lingering economic consequences will make sub-Saharan Africa’s recovery complicated and winding, say the authors.

Figure 1. Daily cases of coronavirus, sub-Saharan Africa vs. advanced economies

Source: Regional Economic Outlook: Sub-Saharan Africa, International Monetary Fund. October 2020.

Source: Regional Economic Outlook: Sub-Saharan Africa, International Monetary Fund. October 2020.

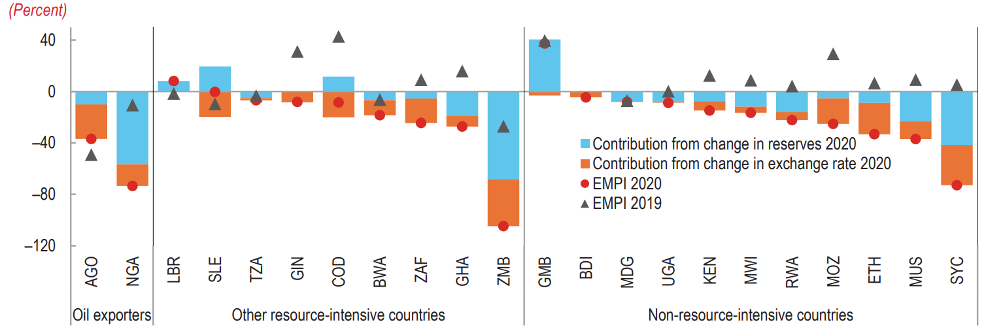

In general, the report notes that not only were the most developed economies of sub-Saharan Africa hit hardest by the effects of the pandemic, but that the pandemic also weakened the ability of these economies to stabilize prices and exchange rates (Figure 2). Figure 2 also shows how the exchange market pressure index (EMPI), which captures negative movements in reserves and exchange rates, has changed over the past year: In short, the data reveal widespread currency depreciation and reduction in reserves in the countries analyzed. Resource-intensive countries Nigeria and Zambia and tourism-dependent Seychelles witnessed sharp reductions in their reserves and currency depreciation (Nigeria’s peg has been devalued multiple times). Low-income countries like Liberia, Gambia, and Uganda did not experience large drops in the EMPI.

Figure 2. Exchange market pressure in select countries of sub-Saharan Africa

Source: Regional Economic Outlook: Sub-Saharan Africa, International Monetary Fund. October 2020.

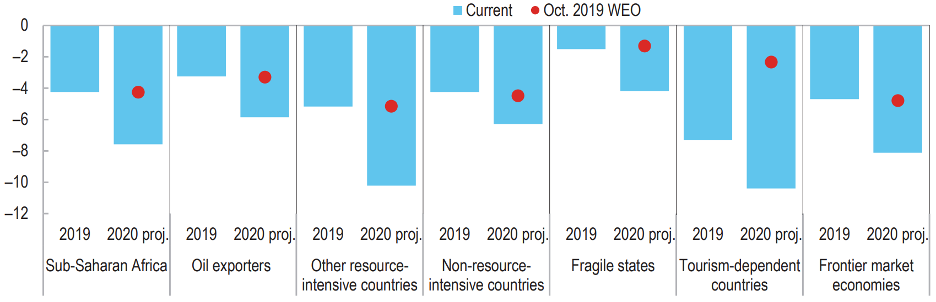

Difficulties in controlling prices and currency values have complicated the debt picture as many countries borrow to finance stimulus packages. Figure 3 shows how the fiscal balance has changed compared to last year’s projections. On the regional level, 2020 fiscal deficits nearly doubled to just under -8 percent compared to -4 percent in 2019—well beyond last year’s projection for 2020. In line with the trends noted above, non-oil, resource-intensive countries and tourism-dependent countries ran the greatest fiscal deficits relative to 2019 projections. Non-resource-intensive countries had the smallest increase in their deficit over projections. At -4 percent, fragile states registered the smallest budget deficit, though they were also projected to do so even before the pandemic. The latest report estimates that the increase in fiscal deficits will contribute to a roughly 10 percentage point regionwide increase in the public debt as a share of GDP.

Figure 3. Change in fiscal balance 2019-20, select countries of sub-Saharan Africa

Source: Regional Economic Outlook: Sub-Saharan Africa, International Monetary Fund. October 2020.

For discussion on how East Africa has used trade to weather the economic effects of COVID-19, consult “Crisis? What crisis? COVID-19 and the unexpected recovery of regional trade in East Africa.” For information on how countries in sub-Saharan Africa are using the debt service suspension initiative to create fiscal space, read “The unfinished agenda of financing Africa’s COVID-19 response.”

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Figure of the week: The post-pandemic road to economic recovery in Africa

November 5, 2020