This article is part of the Brookings Center for Sustainable Development compendium “Innovations in public finance: A new fiscal paradigm for gender equality, climate adaptation, and care.” To learn more about the compendium’s chapters, cross-cutting themes, and policy-relevant insights, see the “Introduction: Six themes and key recommendations for embedding gender equality, care, and climate in fiscal policy.”

Introduction

Despite improvements in women’s economic well-being, opportunities and rights, significant and persistent income and employment gaps remain between men and women.1 These gaps not only disadvantage women, and those with fewer resources and opportunities more generally, but also undermine human rights and can damage economic prosperity for all.2

Gender gaps in economic outcomes arise mostly because there are more women in lower-income households, women perform a higher share of unpaid work as the main carers of children and the elderly, and take on most of home production, leaving them with less time for education and paid work in the labor market. If they do paid work, they are less likely to be in permanent and full-time employment and more likely to be second and low-wage earners or own-account workers under vulnerable employment conditions.3 Global analysis finds differences in human and physical capital, income, composition of income, employment, entrepreneurship, asset ownership, and consumption patterns between men and women, are in turn mediated by gaps in a wide array of legal rights and protection and social norms more generally.4

Successful fiscal policies will be those that best target the underlying causes of these gender inequalities.5 Successful policies are most likely those that can directly facilitate women to access and keep quality and well-paid employment into the future, while also reducing income poverty and inequalities today. Focus should be on ensuring that direct (income) taxes and cash transfers are designed to minimize work disincentives faced by low-wage or second earners or those engaged in small enterprises; on improving provision of care for children and the elderly, gender-neutral parental leave, and flexible work arrangements; and on improving the overall fairness (progressivity) of the tax and benefit system as a whole.6

While not every tax and spending policy has to address gender gaps or reduce poverty directly, they need to complement one another to ensure a more equitable, efficient fiscal system as a whole. Indirect taxes on consumption, while often considered to be regressive as a share of income, can be effective revenue-raisers to fund more cost-effective expenditure policies that address underlying causes of gender gaps.7 Individual policy choices should therefore consider what is suitable for each local context, specific drivers of inequality, administrative capacity, and prevailing norms. For example, in contrast to high-income countries (HICs), low-income countries (LICs) face a greater urgency to narrow gender gaps in opportunities through investment in human capital (health8 and education9 spending) for all, while also enhancing infrastructure that reduces time involved in unpaid work, like fetching water, or accessing key services, such as walking to sanitation facilities.10

Many countries currently face increasing pressures to raise the level of taxation to finance growing public debt and fiscal deficits, which have been worsened by rising costs of borrowing, increases in cost of living, and cutbacks in overseas development assistance. The domestic revenue mobilization (DRM) imperative must consider not only the efficiency of tax collection, ensuring that the social benefits of delivering high-quality public spending are above or equal to the cost of raising taxes, but how fairly the burden is distributed. Otherwise, this risks not only widening income and other gaps but also hindering sustainable, inclusive economic growth. Evidence increasingly suggests there is no clear trade-off between income inequality and growth.11 Insofar as inequality is considered a negative externality, addressing it—including disparities between men and women—can contribute to economic growth.12 Where there has been a desire or pressure to address gender gaps through fiscal policy, reforms often focus on partial or tokenistic measures—such as reduced stamp duty on property transactions and lower registration rates to women homebuyers, despite lacking evidence on their cost-effectiveness.13

In this contribution we argue that fiscal policy can play a key role in reducing income inequality and poverty—including between men and women—while also fostering economic growth. We focus on how taxes and select social spending can be used most effectively if countries take a holistic approach to policymaking. We also briefly outline reform options for improving each individual policy instrument. Finally, we make the case for investing more in essential tools for effective and evidence-based policy design and administration needed to support more joined-up, fairer fiscal systems.

Holistic approach to fiscal policies

While not the only policy lever, evidence from fiscal incidence analysis (FIA) across countries shows that tax and social spending taken together, in most countries, reduces within-country income inequality, including between men and women, and may reduce poverty, but with wide variation in the magnitude of its impact.14 Variation in patterns of inequality, even among countries of similar levels of development and national income, reveal that policy choices, such as the level and progressivity of direct taxation and social spending play a crucial role—both in the present, through direct resource allocation, and in the future, by influencing paid employment, education, and health outcomes, but with wide variation in the magnitude of its impact.15

Cross-country incidence analysis by policy instrument shows that, on average, direct income tax and social spending (cash transfers and in-kind spending on education and health) have the greatest impact on income inequality overall and on work incentives. These instruments can be even more impactful when combined with policies that support caregiving responsibilities for both parents. In lower-income countries, the capacity to redistribute income is less, due to the smaller size of the government, narrower tax bases and weaker social safety nets (SSNs). Most of the fiscal redistribution operates via direct social spending in education and health, though it can change significantly as countries grow, develop, and make policy choices. Results of this type of incidence analysis highlights the importance of how effective each instrument is individually and in combination. Assessing the design and administration of fiscal policies is, therefore, fundamental to informing government decisions about how to balance sometimes competing objectives, such as ensuring tax and spending is equitable and efficient as well as achieving sufficient, sustainable revenue to finance goods and services that promote sustainable, inclusive growth.16

Applying a holistic approach to fiscal policy for closing economic gaps between women and men does not mean that every tax or spending measure must directly target gender disparities or be explicitly pro-poor. Rather, the aim is to ensure that the overall system is balanced across three key objectives—redistribution, revenue generation, and economic incentives—tailored to each country’s context. Research shows that in most countries, there is significant scope to improve the design and implementation of tax and benefit systems, making them more progressive, efficient, and effective for both women and men. Drawing on these insights, principles, and good practices, we present policy reform options by type of instrument to help balance trade-offs among key fiscal objectives.17 These can inform the design of integrated tax and spending packages that address the root causes of gender economic gaps, tailored to each country’s income level, economic structure, inequality patterns, fiscal systems, and state capacity.18

Tax systems to support gender equality: policy options based on principles and emerging evidence

Drawing on emerging evidence and sound tax policy principles, gender-equitable tax policies typically include progressive personal income taxation, minimal disincentives for low-income and secondary earners, equal tax treatment across various forms of labor and capital income, and broad-based value added tax (VAT) and corporate income taxes.19 Tax incentives or breaks should not be granted based on the sex or gender of the asset or firm owner, employee, or consumer. A well-designed tax system should also aim to be simple, transparent, and neutral to minimise economic distortions.20 A well-functioning tax administration and efforts to reduce compliance costs are also crucial for making tax systems more equitable and supportive of women’s economic participation. In lower-income countries—where improving overall revenue collection efficiency may have a greater impact on net redistribution—enhancing compliance, tax and customs administration,21 and taxpayer behavior22 will be especially important.

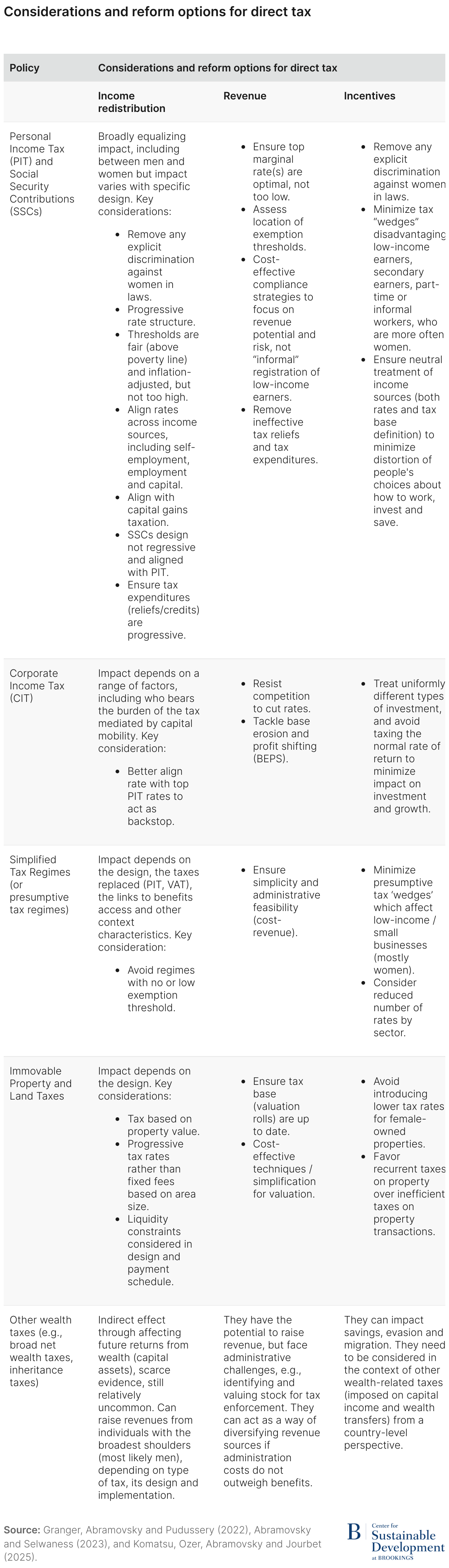

Table 1 summarizes key research insights, evidence gaps, and options to improve the design and implementation of direct taxation in line with policy objectives. We expand on several important points here. Although direct taxes [such as personal income tax (PIT) and property taxes] are not typically the largest source of tax revenue, they have a direct impact on post-tax income distribution—especially when structured with progressively rising marginal rates.

Comprehensive PIT systems that tax all income sources equally tend to be more progressive and better at reducing gender income gaps than dual systems, which tax capital income at lower rates. This is because capital ownership is highly concentrated among top-income individuals.23 In addition, comprehensive PIT systems promote neutrality by i) ensuring entrepreneurial income is taxed similarly to wage income (preventing self-employed individuals from reclassifying labor income as capital to pay lower taxes); and ii) applying uniform taxation across different types of capital income (e.g., capital gains, interest, and dividends), thereby reducing behavioral distortions. However, implementing such systems can be more complex and may create stronger disincentives for savings and investment if the tax base is not carefully designed to mitigate these effects.24

Closely related is the role of corporate income tax (CIT), which serves as a backstop to PIT by discouraging individuals from sheltering personal income within corporations as retained earnings or deductible expenses.25 Several studies suggest that many countries still have room to raise top marginal PIT rates and align them more closely with CIT rates without negatively impacting economic growth or employment.26 In many low- and middle- income countries (LMICs), statutory rates are relatively higher than in many HICs but taxable personal and corporate incomes are narrow due to significant exclusions from tax bases (i.e., high tax-free thresholds,27 deductions for medical or educational expenses28 or tax incentives for firms29), resulting in low levels of effective tax rates, revenues, and progressivity.

Finally, while taxes on wealth (excluding immovable property) remain relatively rare, they are increasingly being reconsidered as a complementary tool to ensure high-net-worth individuals (HNWIs) contribute their fair share.30

Impacts on labor market decisions at the margins—such as whether to work or how many hours to work—are closely linked to tax rates and the way taxes are applied, including credits, reliefs, and their interaction with benefit payments. Strengthening formal work incentives by minimizing tax “wedges”—the gap between the labor cost to the employer and the employee’s take-home pay—is especially important for low-income, second, or part-time earners, who are more often women. In tax systems that still apply joint taxation for couples, or where tax credits are calculated jointly, second earners often face higher effective tax wedges, which can discourage labor force participation.31

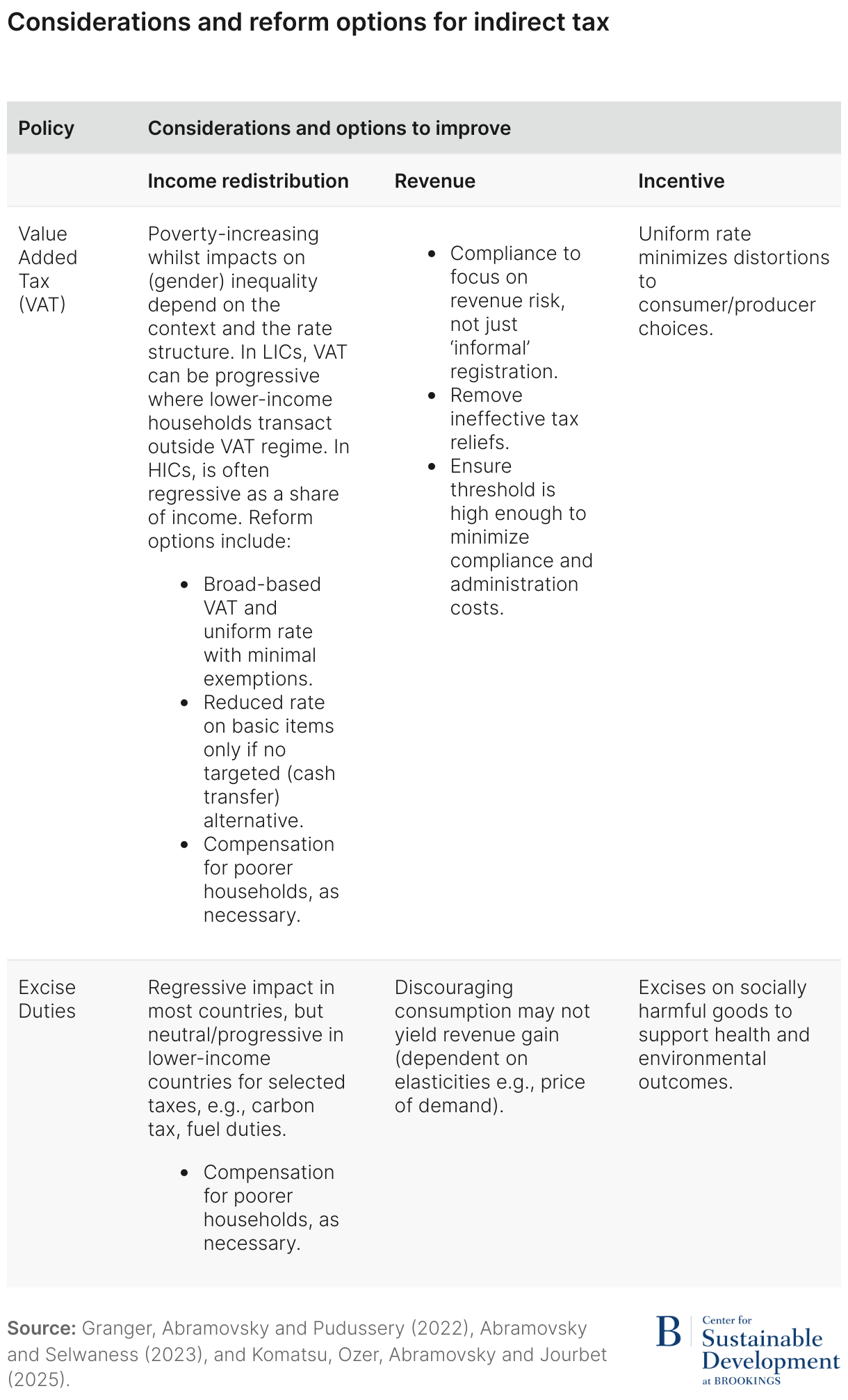

Table 2 highlights reform options for two important indirect taxes in terms of revenue: VAT and excise duties. Indirect taxes represent a substantial share of revenue in most countries, including HICs with strong and progressive PIT systems.32

As efficient revenue-raising instruments, addressing compliance gaps and inefficiencies is crucial to maximizing resources available for equitable social spending.

To mitigate the poverty-related and often regressive effects of VAT, many countries apply exemptions or reduced rates on basic goods (e.g., staple foods)—a form of tax expenditure. However, this approach is generally poorly targeted, often benefiting higher-income consumers more than the poorest in absolute terms. In lower-income countries, where the poorest households frequently consume goods sourced from home production or informal vendors, this approach is even less effective in reaching those most in need. A more efficient and equitable alternative is to maintain a broad VAT base with a uniform rate while using targeted cash transfers to support low-income or vulnerable groups.33

In lower-income countries, consumption patterns suggest that excise taxes on certain goods and services—such as fuel, vehicles, carbon emissions, and other luxury items—can have progressive effects. Nonetheless, these taxes may still impose burdens on low-income households. To protect the poor, such measures should ideally be accompanied by compensatory transfers.34

Selected social spending

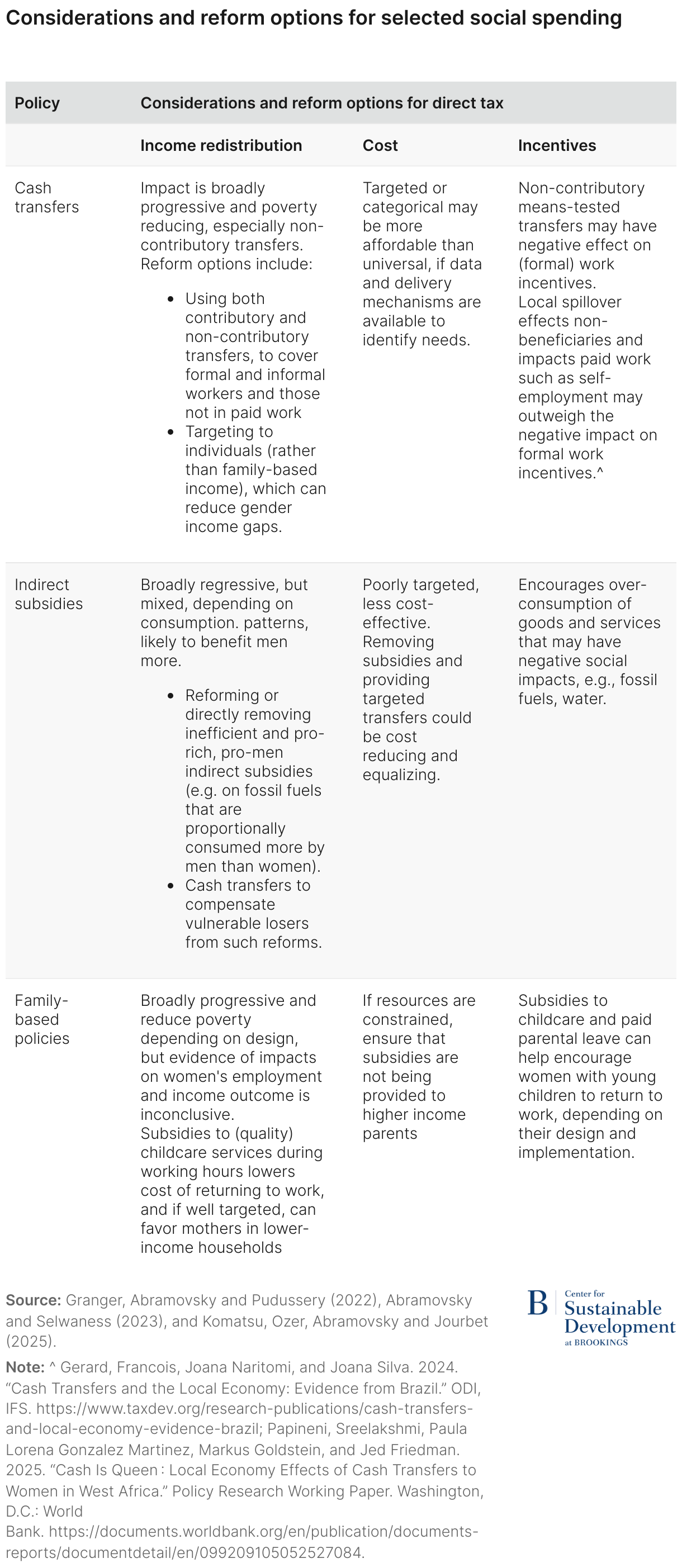

Table 3 presents reform options for social spending instruments that play a critical role in reducing poverty and gender inequality. Among these, cash transfers—particularly non-contributory and poverty-targeted ones—are broadly progressive and effective in reducing poverty. When targeted at individuals rather than households, they can be more effective in addressing women’s poverty. Combining contributory and non-contributory schemes can enhance coverage across formal and informal workers, as well as those not in employment. However, how best to achieve this in practice remains an open and context-specific question. While means-tested transfers may weaken incentives for formal employment, they can have overall positive effects on local economies.

Indirect subsidies, such as those on fossil fuels, are often regressive and disproportionately benefit men. Reforming or removing these subsidies and replacing them with targeted transfers can improve equity and reduce fiscal costs.

Family-based policies, including subsidies for childcare and paid parental leave, can lower barriers to women’s labor force participation—especially when targeted to low-income households. However, evidence on their long-term effects on women’s income and employment is mixed, underscoring the need for careful policy design and implementation.

Considering complementary policies

Taking these taxation and spending policy options together, and considering packages of complementary measures from each list, could be a more effective approach to tackling complex income and gender gaps while balancing the objectives of redistribution, revenue, and incentives. For example, in addition to removing any explicit bias in tax and benefit systems, reforms that may negatively affect low-income households such as removing fuel subsidies can be combined with targeted SSNs spending and still be revenue raising.

While fiscal policy is a powerful tool for promoting fairer outcomes, economic incentives and income redistribution alone may not be sufficient to address deeper, structural causes of inequality. A truly holistic approach to fiscal policy must also consider social and cultural norms, the unequal distribution of unpaid care work within households,35 and the types of jobs available.36 These broader contextual factors are essential for designing policies that effectively support gender equity and inclusive growth.

The way forward: Essential tools for effective and evidence-based policy design and administration

Designing a more holistic fiscal policy and building resilience to increasing risks of climate-related shocks requires better quality and more joined up data and analysis. Yet, limited data and analytical capacity remain major obstacles to understanding the drivers of gender economic gaps and determining how fiscal policies can best address them—especially given their context-specific design and impacts. Estimating behavioral responses, distributional impacts across household income and expenditure, and the impacts of revenue and spending policies requires robust data and analytical tools, which are often lacking—particularly in L&MICs.

Moreover, while it is essential to consider the combined effects of tax and social spending policies, these instruments are often designed in silos with limited coordination. This fragmentation hinders the development and implementation of effective, evidence-based reform packages.

A holistic approach to fiscal policy must address these gaps. In this context, we highlight key and complementary data and tools essential to foster better design of fiscal policies that work better for both women and men, drawing on evidence from the country-level insights from the Centre for Tax Analysis in Developing Countries.

Unlocking the power of data

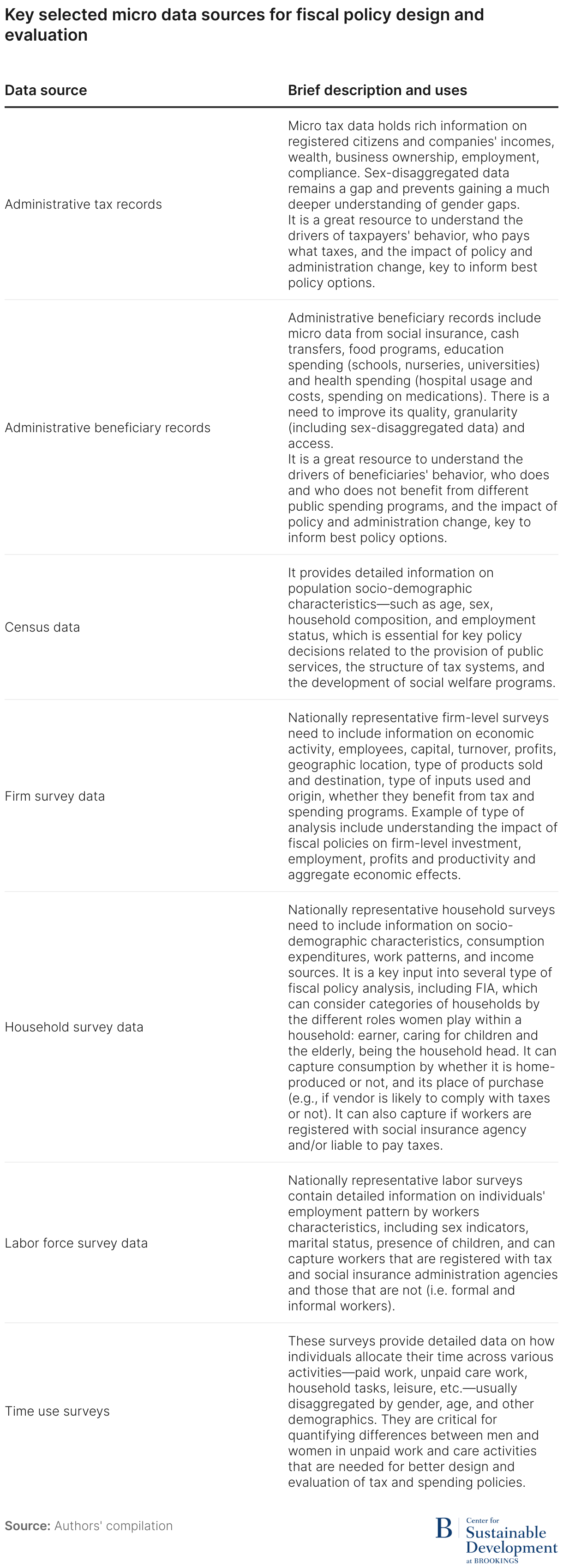

Timely, reliable, and representative survey microdata, complemented by comprehensive administrative records on taxpayers and beneficiaries of public programs, generate a granular and context-specific understanding of the population. Together, these data sources enable the analysis of socio-economic conditions and disparities—such as those between women and men—informing more equitable and evidence-based policy decisions. They need to cover not only central government but also local government and include sex-disaggregated data, to unlock the potential to gain a much deeper understanding of gender-related gaps.37 However, these are often lacking in many LMICs. While there are challenges with data access and privacy regulations, among others, investing in filling data gaps can be extremely valuable. Table 4 highlights some key selected data micro data sources that governments should collect for better fiscal policy design and evaluation.

Combining data sources has high returns in providing a more comprehensive picture of national populations that is essential for fiscal policy design and administration. For example, real progress has been made in measuring the formal income for high-income individuals within selected countries,38 which allows a more accurate characterization of income inequality, including between men and women, and the incidence of direct taxes on these individuals. The methods require access to micro level individual and household surveys and tax administrative data. Combined with national aggregates and specific assumptions, these data can yield better evidence for policy design and evaluation than using survey or administrative data separately. With global rules taking effect on disclosure and exchange of information on tax and incomes, more information than ever is available on the assets and incomes of HNWIs and multinational firms, including their ownership structures through better Beneficial Ownership registers,39 boosting the potential to improve the measurement of income and wealth.40

Combining survey and benefit and tax records can help understand fiscal policy impacts for low-income individuals and small firms, particularly in lower-income countries where a large share of the population does not interact with tax or benefit administrations.41

Investing in methods, modeling and capacities

Despite existing gaps, significantly more data is now being generated—but governments need stronger capacity to meaningfully analyze and apply it in policymaking. In particular, developing methods, modeling tools, and capacities to assess the impact of fiscal policies on both men and women—especially regarding income, employment, and how to address underlying constraints.

There may be many options and appropriate models and approaches, which often provide complementary insights. As a starting point, conducting systematic policy appraisals42 and costings,43 which aim to support evidence-based analysis of a proposed policy’s strengths, weaknesses, and impacts, provide insights to inform decision-making.

Related to this, an area where there has been remarkable progress has been with tax expenditure cost-benefit analysis across countries,44 including in LMICs. Tax expenditures—such as exemptions, credits, deductions, and reduced rates—are deviations from standard tax rules that benefit specific groups or activities. They aim to provide financial support or incentives but often lack the transparency of direct spending.45 However, important gaps remain in quantifying the distributional impact of a range of tax expenditures and the social returns to them, for which a combination of approaches is often needed. For example, using household-level microsimulation models and FIA can help understand the distributional impact of specific tax expenditures such as VAT exemptions or zero-rates on foodstuff across households.46 Evaluating the rationale and cost-benefit of tax incentives for firms (other type of tax expenditures) will require other approaches.47

Distributional analysis (microsimulation) models can also provide essential evidence to any policy appraisal or evaluation that is focused on informing the design of more equitable fiscal policy. Examples of these models, such as SOUTHMOD, have been used to assess the ex ante and ex post evaluation of policy (reforms), and policy alternatives, in terms of their distributional and poverty impact at the household or individual level in lower-income countries (e.g., the presumptive tax in Uganda48). These models can also quantify the overall incidence effect of fiscal policies across households according to the sex of the breadwinner or other gender characteristics.49 While they can be costly and resource-intensive to develop and maintain, they can be a worthwhile long-term investment. The principles of distributional analysis can also be applied in simpler ways, using analysis of household income and expenditure patterns to better understand how a policy may affect different income groups.

Authors

-

Acknowledgements and disclosures

The Brookings Institution is a nonprofit organization devoted to independent research and policy solutions. Its mission is to conduct high-quality, independent research and based on that research, to provide innovative, practical recommendations for policymakers and the public. The conclusions and recommendations of any Brookings publication are solely those of its author(s), and do not reflect the views or policies of the Institution, its management, its other scholars, or the funders acknowledged below.

This publication is supported by the Gates Foundation, the William and Flora Hewlett Foundation, and the Norwegian Agency for Development Cooperation (Norad). The findings and conclusions contained within are those of the authors and do not necessarily reflect positions or policies of the donors.

Brookings recognizes that the value it provides is in its absolute commitment to quality, independence, and impact. Activities supported by its donors reflect this commitment.

-

Footnotes

- Pal, Kusum Kali, Kim Piaget, Saadia Zahidi, and Silja Baller. 2024. “Global Gender Gap Report 2024.” World Economic Forum. https://www.weforum.org/publications/global-gender-gap-report-2024/

-

The UN recognises gender equality as a fundamental human right, which is embedded in Sustainable Development Goal 5. Hsieh et al. (2019), Kolovich et al. (2024) and Santos-Silva and Klasen (2021) discuss emerging evidence showing significant macroeconomic gains from increasing female labor force participation, access to financial assets and entrepreneurship. “United Nations: Gender Equality and Women’s Empowerment.” n.d. United Nations Sustainable Development. Accessed June 20, 2025.

https://www.un.org/sustainabledevelopment/gender-equality/; Hsieh, Chang-Tai, Erik Hurst, Charles I. Jones, and Peter J. Klenow. 2019. “The Allocation of Talent and U.S. Economic Growth.” Econometrica 87 (5): 1439–74.

https://doi.org/10.3982/ECTA11427; Lisa L Kolovich, Monique Newiak, Diego B. P. Gomes, Jiajia Gu, Vivian Malta, and Jorge Mondragon. “Why a Gender Lens Matters: Unlocking Solutions to Macroeconomic Challenges”, Gender Notes 2024, 003 (2024), accessed June 25, 2025.

https://doi.org/10.5089/9798400289538.067; Santos Silva, Manuel, and Stephan Klasen. 2021. “Gender Inequality as a Barrier to Economic Growth: A Review of the Theoretical Literature.” Review of Economics of the Household 19 (3): 581–614.

https://doi.org/10.1007/s11150-020-09535-6 -

Lo Bue et al. (2022) document that women are overrepresented among workers in vulnerable employment in developing countries. Lo Bue, Maria C., Tu Thi Ngoc Le, Manuel Santos Silva, and Kunal Sen. 2022. “Gender and Vulnerable Employment in the Developing World: Evidence from Global Microdata.” World Development 159 (November):106010.

https://doi.org/10.1016/j.worlddev.2022.106010 -

“Gender Data Portal: Assets.” n.d. World Bank Gender Data Portal. Accessed June 20, 2025.

https://genderdata.worldbank.org/en/topics/assets; Oliva, Nicolás, H. Xavier Jara, and Pia Rattenhuber. “What Explains the Gender Gap in Top Incomes in Developing countries?: Evidence from Ecuador”, WIDER Working Paper 2/109 Helsinki: UNU-WIDER, 2021. https://doi.org/10.35188/UNU-WIDER/2021/049-8; Del Carmen, Giselle, Santiago Garriga, Wilman Ponce, and Thiago Scot. 2025. “Two Decades of Top Income Shares in Honduras.” Journal of Public Economics 246 (June):105362. https://doi.org/10.1016/j.jpubeco.2025.105362; “Gender Data Portal: Employment and Time Use.” n.d. World Bank Gender Data Portal. Accessed June 20, 2025.

https://genderdata.worldbank.org/en/topics/employment-and-time-use; “Gender Data Portal: Entrepreneurship.” n.d. World Bank Gender Data Portal. Accessed June 20, 2025.

http://genderdata.worldbank.org/en/topics/entrepreneurship; Deere, Carmen Diana, and Cheryl R. Doss. “The gender asset gap: What do we know and why does it matter?.” Feminist economics 12, no. 1-2 (2006): 1-50. https://www.tandfonline.com/doi/abs/10.1080/13545700500508056; O’Donoghue, Cathal, Karina Doorley, and Denisa Maria Sologon. 2024. “Gender Difference in Household Consumption: Some Convergence Over Three Decades.” IZA Institute of Labor Economics, IZA Discussion Paper No. 16852, , March. https://docs.iza.org/dp16852.pdf “Women, Business and the Law 2024.” 2024. Washington, DC: World Bank. https://openknowledge.worldbank.org/entities/publication/853a55af-f1ba-4979-949c-61979af2fbb9 -

Abramovsky, Laura, and Irene Selwaness. 2023. “Fiscal Policy and Gender Income Inequality: The Role of Taxes and Social Spending.” ODI Working Paper. London: ODI.

https://media.odi.org/documents/DPF_R_Fiscal_policy_and_gender_income_inequality_-_the_role_of_taxes_and_socia_4fIDfpa.pdf - Ibid.

-

Warwick, Ross, Tom Harris, David Phillips, Maya Goldman, Jon Jellema, Gabriela Inchauste, and Karolina Goraus-Tańska. 2022. “The Redistributive Power of Cash Transfers vs VAT Exemptions: A Multi-Country Study.” World Development 151 (March):105742.

https://doi.org/10.1016/j.worlddev.2021.105742 - “Gender Data Portal: Health.” n.d. World Bank Gender Data Portal. Accessed June 20, 2025. https://genderdata.worldbank.org/en/topics/health

- “Gender Data Portal: Labor Force by Level of Education (%).” n.d. World Bank Gender Data Portal. Accessed June 20, 2025. https://genderdata.worldbank.org/en/indicator/sl-tlf-zs

-

“Women and Girls Bear Brunt of Water and Sanitation Crisis – New UNICEF-WHO Report.” 2023. WHO (blog). July 6, 2023.

https://www.who.int/news/item/06-07-2023-women-and-girls-bear-brunt-of-water-and-sanitation-crisis—new-unicef-who-report - Baselgia, Enea, and Reto Foellmi. “Inequality and Growth: A Review on a Great Open Debate in Economics”, WIDER Working Paper 2022/5 Helsinki: UNU-WIDER, 2022. https://doi.org/10.35188/UNU-WIDER/2022/136-5

- Stiglitz, Joseph. The Price of Inequality: How Today’s Divided Society Endangers Our Future, W. W. Norton & Company, 2012. https://wwnorton.com/books/the-price-of-inequality/; Baselgia and Foellmi, “Inequality and Growth”; “Poverty and Shared Prosperity 2022: Correcting Course.” 2022. Washington, DC: World Bank. https://openknowledge.worldbank.org/entities/publication/a33782e6-415e-5699-a9a8-4a50dc4ae3bc; Støstad, Morten Nyborg, and Frank Cowell. 2024. “Inequality as an Externality: Consequences for Tax Design.” Journal of Public Economics 235 (July):105139. https://doi.org/10.1016/j.jpubeco.2024.105139

- Grown, Caren, and Guilia Mascagni. 2024. “Towards Gender Equality in Tax and Fiscal Systems.” ICTD Policy Brief Number 5. ICTD, The Brookings Institution. https://www.brookings.edu/articles/towards-gender-equality-in-tax-and-fiscal-systems/

- Granger, Hazel, Laura Abramovsky, and Jessica Pudussery. 2022. “Fiscal Policy and Income Inequality: The Role of Taxes and Social Spending.” ODI Report. London: ODI. https://media.odi.org/documents/ODI_Report_Fiscal_policy_and_income_inequality_the_role_of_taxes_and_social_sp_GwknCLd.pdf; Abramovsky and Selwaness, “Fiscal policy and gender income inequality.”

- Granger et al. “Fiscal Policy and Income Inequality”; Abramovsky and Selwaness, “Fiscal policy and gender income inequality.”

- Granger et al. “Fiscal Policy and Income Inequality”; Abramovsky and Selwaness, “Fiscal policy and gender income inequality.”

- Abramovsky and Selwaness, “Fiscal policy and gender income inequality.”

- Ibid.

- Ibid.

- A neutral tax system often refers to taxing similar activities similarly, which tends to be fairer (taxes similar people doing similar things at the same rate), more efficient (people do not change behavior to get a lower tax rate) and simpler (less need to define and enforce boundaries). In the context of gender equality, it has been interpreted to mean neutral with respect to marital arrangements. Hemel, Daniel. 2019. “Beyond the Marriage Tax Trilemma.” Wake Forest Law Review 54:661. https://heinonline.org/HOL/LandingPage?handle=hein.journals/wflr54&div=25&id=&page=

-

Shaukat, Mahvish Ifrah, Ashima Neb, Hitomi Komatsu, and Ozer Ceren. 2023 “Knowledge Note 2. Building Gender Equality Objectives in Tax and Customs Administrations.” Knowledge Note Series. Washington, D.C.: World Bank. Accessed June 25, 2025.

https://documents1.worldbank.org/curated/en/099137312202333951/pdf/IDU1a4d2ab6e13b1e146f1189991c240603f5f3d.pdf?_gl=1*rzf1yp*_gcl_au*MTA4MjUyMzYwOC4xNzI0ODUyODI5 - Komatsu, Hitomi, Mahvish Ifrah Shaukat, and Ozer Ceren. 2024. “Unpacking Tax Compliance from a Gender Perspective. Gender and Tax Dialogue Knowledge Note.” Gender and Tax Dialogue Knowledge Note. Washington, D.C.: World Bank. https://documents.worldbank.org/en/publication/documents-reports/documentdetail/099936005242435341

- Advani, Arun, and Andy Summers. 2020. “Capital Gains and UK Inequality.” https://shs.hal.science/halshs-03022609; Bergolo, Marcelo, Juliana Londoño-Vélez, and Darío Tortarolo. 2023. “Tax Progressivity and Taxing the Rich in Developing Countries: Lessons from Latin America.” Oxford Review of Economic Policy, Autumn 2023, 39 (3): 530–49. https://doi.org/10.1093/oxrep/grad029; Del Carmen et al., “Two decades of top income.”

-

Delestre, Isaac, Wojciech Kopczuk, Helen Miller, and Kate Smith. 2024. “Top Income Inequality and Tax Policy.” Oxford Open Economics 3 (Supplement_1): i1086–1112.

https://doi.org/10.1093/ooec/odad068 - Bachas, Pierre, Anne Brockmeyer, Roel Dom, and Camille Semelet. 2025. “Effective Tax Rates, Firm Size and the Global Minimum Tax.” Policy Research Working Paper 11090. The World Bank. https://taxdev.org/effective-tax-rates-firm-size-and-global-minimum-tax; Leite, David. 2024. “The Firm as Tax Shelter Micro Evidence and Aggregate Implications of Consumption Through the Firm.” https://www.parisschoolofeconomics.eu/app/uploads/2024/11/LEITE-David-JMP-OK.pdf

-

Kindermann, Fabian, and Dirk Krueger. 2022. “High Marginal Tax Rates on the Top 1 Percent? Lessons from a Life-Cycle Model with Idiosyncratic Income Risk.” American Economic Journal: Macroeconomics 14 (2): 319–66. https://doi.org/10.1257/mac.20150170; Støstad and Cowell, “Inequality as an externality.”

However, as highlighted in Fuest and Neumeier (2023), the evidence on the incidence of CIT and its impact on investment and economic growth is inconclusive. Fuest, Clemens, and Florian Neumeier. 2023. “Corporate Taxation.” Annual Review of Economics 15 (Volume 15, 2023): 425–50.

https://doi.org/10.1146/annurev-economics-082322-014747 - Bergolo et al., “Tax progressivity and taxing the rich.”

- Jantijies, Dumisani, Kagiso Mamabolo, Mukundi Maphangwa, Seeraj Mohamed, Tshepo Moloi, Sithembiso Mthimkhulu, Nelia Orlandi, Lwazikazi Ntinzi, Mmapula Sekatane, and Sbusisiwe Sibeko. 2025. “2025 Budget: Second PreBudget Brief on Revenue Options and Fiscal Policy.” 21/2/4. Parliament of the Republic of South Africa. https://www.parliament.gov.za/storage/app/media/PBO/Budget_Analysis/2025/3-march/10-03-2025/PBO_Pre-budget_brief_Exploring_alternative_revenue_sources_and_fiscal_strategies_07_March_2025.pdf

- Bachas et al., “Effective Tax Rates.”

-

HNWIs tend to be men, are more likely to shield, either legally or illegally, their income and wealth from tax authorities, for example by holding financial assets or real estate holdings offshore (Alstadsæter et al., 2022, Londoño-Vélez and Ávila-Mahecha, 2021), achieving lower effective tax rates. Alstadsæter, Annette, Niels Johannesen, Ségal Le Guern Herry, and Gabriel Zucman. 2022. “Tax Evasion and Tax Avoidance.” Journal of Public Economics 206 (February):104587.

https://doi.org/10.1016/j.jpubeco.2021.104587; Londoño-Vélez, Juliana, and Javier Ávila-Mahecha. 2021. “Enforcing Wealth Taxes in the Developing World: Quasi-Experimental Evidence from Colombia.” American Economic Review: Insights 3 (2): 131–48.

https://doi.org/10.1257/aeri.20200319. - “Taxing Wages 2024: Tax and Gender through the Lens of the Second Earner.” 2024. Paris: OECD. https://www.oecd.org/en/publications/taxing-wages-2024_dbcbac85-en.html

- Granger et al., “Fiscal policy and income inequality.”

- Warwick et al., “The redistributive power of cash transfers.”

-

Motor fuels, motor vehicle ownership and road use are often progressive and equalizing in LICs and lower-middle income countries given consumption patterns, although they can increase poverty. Sin taxes are usually regressive and poverty-increasing in most contexts in the short term. However, the long-run health benefits may outweigh the initial regressive impact on income. Advani, Arun, Ross Warwick, Andrea Smurra, and Dániel Prinz. 2021. “What Is the Case for Carbon Taxes in Developing Countries?” Institute for Fiscal Studies (blog). November 2021. https://ifs.org.uk/articles/what-case-carbon-taxes-developing-countries; Kavuma, Susan Namirembe, Christine Byaruhanga, Nicholas Musoke, Patrick Loke, Michael Noble, and Gemma Wright. “An Analysis of the Distributional Impact of Excise Duty in Uganda Using a Tax-Benefit Microsimulation Model”, WIDER Working Paper 2020/70 Helsinki: UNU-WIDER, 2020.

https://doi.org/10.35188/UNU-WIDER/2020/827-6; Dorband, Ira Irina, Michael Jakob, Matthias Kalkuhl, and Jan Christoph Steckel. 2019. “Poverty and Distributional Effects of Carbon Pricing in Low- and Middle-Income Countries – A Global Comparative Analysis.” World Development 115 (March):246–57.

https://doi.org/10.1016/j.worlddev.2018.11.015; Arunatilake, Nisha, Gabriela Inchauste, and Nora Lustig. 2017. “The Incidence of Taxes and Spending in Sri Lanka.” Commitment to Equity (CEQ) Working Paper Series, Commitment to Equity (CEQ) Working Paper Series, May.

https://ideas.repec.org//p/tul/ceqwps/63.html; Inchauste, Gabriela, Mashekwa Maboshe, Catriona Mary Purfield, Ingrid Denise Woolard, and Nora C. Lustig. 2015. “The Distributional Impact of Fiscal Policy in South Africa.” 019. Poverty and Equity Global Practice Working Paper Series. Washington, D.C.: World Bank.

https://documents1.worldbank.org/curated/en/502441468299632287/pdf/WPS7194.pdf. Fuchs, Alan, and Francisco Jalles Meneses. 2017. “Regressive or Progressive? The Effect of Tobacco Taxes in Ukraine.” Poverty & Equity Global Practice Working Paper 121.

https://documents1.worldbank.org/curated/en/712811524485287678/pdf/125569-NWP-PUBLIC-POV121-PRWP8227.pdf; Fuchs, Alan, and Francisco Jalles Meneses. 2017. “Are Tobacco Taxes Really Regressive? Evidence from Chile.” Policy Research Working Paper 7988. Washington, D.C.

https://documents1.worldbank.org/curated/en/919121488376958052/pdf/WPS7988.pdf; Fuchs, Alan, Giselle Del Carmen, and Alfred Kechia Mukon. 2018. “Long-Run Impacts of Increasing Tobacco Taxes: Evidence from South Africa.” Washington, D.C.: World Bank.

https://openknowledge.worldbank.org/entities/publication/5123f6d1-af98-5138-a722-d938e16aa41e -

Charmes, Jacques. 2022. “Variety and Change of Patterns in the Gender Balance between Unpaid Care-Work, Paid Work and Free Time across the World and over Time: A Measure of Wellbeing?” Wellbeing, Space and Society 3 (January):100081.

https://doi.org/10.1016/j.wss.2022.100081 -

“Jobs and Growth.” 2025. World Bank. March 2025.

https://www.worldbank.org/en/topic/jobsandgrowth/overview -

Mascagni, Guilia, Sripriya Iyengar Srivatsa, Attu Daisy, Homi Komatsu, and Maria Jouste. 2025. “Unlocking the Power of Sex-Disaggregated Administrative Tax Data: Insights from the Latest CoPGT Meeting.” ICTD (blog). March 2025.

https://www.ictd.ac/news/sex-disaggregated-administrative-tax-data - Del Carmen et al., “Two decades of top income.”

-

“Open Ownership: Impact.” n.d. Open Ownership. Accessed June 23, 2025.

https://www.openownership.org/en/impact/ - Bachas et al., “Effective Tax Rates.”

-

According to ILO (2023), 89% of all workers are considered informal in low-income countries (defined as employees that are not registered with social security agency, own-account workers or employers that are not registered with national authorities or contributing family workers). According to the World Bank (2025), 78% of the population is missed by social protection systems (i.e. live in a household in which no member benefited from any social protection program or contributed to any social insurance scheme) in low-income countries. International Labour Organization (2023). Women and Men in the informal economy: A statistical update. 2023. https://www.ilo.org/sites/default/files/wcmsp5/groups/public/%40ed_protect/%40protrav/%40travail/documents/publication/wcms_869188.pdf; World Bank. 2025. State of Social Protection Report 2025: The 2-Billion-Person Challenge. Washington, DC: World Bank.

http://hdl.handle.net/10986/42842 - Granger, Hazel, David Phillips, and Ross Warwick. 2021. “Tax Policy Appraisal Manual.” London: The Institute for Fiscal Studies. https://www.taxdev.org/explainers-tools/tax-policy-appraisal-manual

- Phillips, David, Yani Tyskerud, and Ross Warwick. 2021. “Tax Policy Costing Manual.” London: The Institute for Fiscal Studies. https://www.taxdev.org/explainers-tools/tax-policy-costing-manual

-

Granger, Hazel, Kyle McNabb, and Harshil Parekh. 2022. “Tax Expenditure Reporting in Rwanda and Uganda.” ODI Working Paper. London: ODI.

https://cdn.odi.org/media/documents/ODI_Working_paper_Tax_expenditure_reporting_in_Rwanda_and_Uganda.pdf -

Redonda, Agustin, Lucas Millan, Christian von Haldenwang, and Flurim Aliu. 2023. “The Global Tax Expenditures Transparency Index Companion Paper.” Bonn, Germany: Tax Expenditures Lab.

https://www.taxexpenditures.org/2023/10/08/the-global-tax-expenditures-transparency-index-companion-paper/ - Warwick et al., “The redistributive power of cash transfers.”

- “Tax Incentives Principles” 2025. Platform for Collaboration on Tax. https://www.tax-platform.org/sites/pct/files/publications/Tax-Incentives-Principles.pdf

-

Waiswa, Ronald, Jesse Lastunen, Gemma Wright, Michael Noble, Joseph Okello Ayo, Milly Isingoma Nalukwago, Tina Kaidu Barugahara, Susan Kavuma, Isaac Arinaitwe, Martin Mwesigye, Wilson Asiimwe, and Pia Rattenhuber. “An Assessment of Presumptive Tax in Uganda: Evaluating the 2020 Reform and Four Alternative Reform Scenarios Using UGAMOD, a Tax-Benefit Microsimulation Model for Uganda”, WIDER Working Paper 2021/163 Helsinki: UNU-WIDER, 2021.

https://doi.org/10.35188/UNU-WIDER/2021/103-7 -

Robayo, Monica, Ana Maria Tribin Uribe, and Jose Andres Oliva Cepeda. 2023. “Fiscal Policy as a Tool for Gender Equity in El Salvador.” Policy Research Working Paper Series 10547. Washington, D.C.: The World Bank.

https://ideas.repec.org//p/wbk/wbrwps/10547.html

https://www.un.org/sustainabledevelopment/gender-equality/; Hsieh, Chang-Tai, Erik Hurst, Charles I. Jones, and Peter J. Klenow. 2019. “The Allocation of Talent and U.S. Economic Growth.” Econometrica 87 (5): 1439–74.

https://doi.org/10.3982/ECTA11427; Lisa L Kolovich, Monique Newiak, Diego B. P. Gomes, Jiajia Gu, Vivian Malta, and Jorge Mondragon. “Why a Gender Lens Matters: Unlocking Solutions to Macroeconomic Challenges”, Gender Notes 2024, 003 (2024), accessed June 25, 2025.

https://doi.org/10.5089/9798400289538.067; Santos Silva, Manuel, and Stephan Klasen. 2021. “Gender Inequality as a Barrier to Economic Growth: A Review of the Theoretical Literature.” Review of Economics of the Household 19 (3): 581–614.

https://doi.org/10.1007/s11150-020-09535-6

https://doi.org/10.1016/j.worlddev.2022.106010

https://genderdata.worldbank.org/en/topics/assets; Oliva, Nicolás, H. Xavier Jara, and Pia Rattenhuber. “What Explains the Gender Gap in Top Incomes in Developing countries?: Evidence from Ecuador”, WIDER Working Paper 2/109 Helsinki: UNU-WIDER, 2021. https://doi.org/10.35188/UNU-WIDER/2021/049-8; Del Carmen, Giselle, Santiago Garriga, Wilman Ponce, and Thiago Scot. 2025. “Two Decades of Top Income Shares in Honduras.” Journal of Public Economics 246 (June):105362. https://doi.org/10.1016/j.jpubeco.2025.105362; “Gender Data Portal: Employment and Time Use.” n.d. World Bank Gender Data Portal. Accessed June 20, 2025.

https://genderdata.worldbank.org/en/topics/employment-and-time-use; “Gender Data Portal: Entrepreneurship.” n.d. World Bank Gender Data Portal. Accessed June 20, 2025.

http://genderdata.worldbank.org/en/topics/entrepreneurship; Deere, Carmen Diana, and Cheryl R. Doss. “The gender asset gap: What do we know and why does it matter?.” Feminist economics 12, no. 1-2 (2006): 1-50. https://www.tandfonline.com/doi/abs/10.1080/13545700500508056; O’Donoghue, Cathal, Karina Doorley, and Denisa Maria Sologon. 2024. “Gender Difference in Household Consumption: Some Convergence Over Three Decades.” IZA Institute of Labor Economics, IZA Discussion Paper No. 16852, , March. https://docs.iza.org/dp16852.pdf “Women, Business and the Law 2024.” 2024. Washington, DC: World Bank. https://openknowledge.worldbank.org/entities/publication/853a55af-f1ba-4979-949c-61979af2fbb9

https://media.odi.org/documents/DPF_R_Fiscal_policy_and_gender_income_inequality_-_the_role_of_taxes_and_socia_4fIDfpa.pdf

https://doi.org/10.1016/j.worlddev.2021.105742

https://www.who.int/news/item/06-07-2023-women-and-girls-bear-brunt-of-water-and-sanitation-crisis—new-unicef-who-report

https://documents1.worldbank.org/curated/en/099137312202333951/pdf/IDU1a4d2ab6e13b1e146f1189991c240603f5f3d.pdf?_gl=1*rzf1yp*_gcl_au*MTA4MjUyMzYwOC4xNzI0ODUyODI5

https://doi.org/10.1093/ooec/odad068

However, as highlighted in Fuest and Neumeier (2023), the evidence on the incidence of CIT and its impact on investment and economic growth is inconclusive. Fuest, Clemens, and Florian Neumeier. 2023. “Corporate Taxation.” Annual Review of Economics 15 (Volume 15, 2023): 425–50.

https://doi.org/10.1146/annurev-economics-082322-014747

https://doi.org/10.1016/j.jpubeco.2021.104587; Londoño-Vélez, Juliana, and Javier Ávila-Mahecha. 2021. “Enforcing Wealth Taxes in the Developing World: Quasi-Experimental Evidence from Colombia.” American Economic Review: Insights 3 (2): 131–48.

https://doi.org/10.1257/aeri.20200319.

https://doi.org/10.35188/UNU-WIDER/2020/827-6; Dorband, Ira Irina, Michael Jakob, Matthias Kalkuhl, and Jan Christoph Steckel. 2019. “Poverty and Distributional Effects of Carbon Pricing in Low- and Middle-Income Countries – A Global Comparative Analysis.” World Development 115 (March):246–57.

https://doi.org/10.1016/j.worlddev.2018.11.015; Arunatilake, Nisha, Gabriela Inchauste, and Nora Lustig. 2017. “The Incidence of Taxes and Spending in Sri Lanka.” Commitment to Equity (CEQ) Working Paper Series, Commitment to Equity (CEQ) Working Paper Series, May.

https://ideas.repec.org//p/tul/ceqwps/63.html; Inchauste, Gabriela, Mashekwa Maboshe, Catriona Mary Purfield, Ingrid Denise Woolard, and Nora C. Lustig. 2015. “The Distributional Impact of Fiscal Policy in South Africa.” 019. Poverty and Equity Global Practice Working Paper Series. Washington, D.C.: World Bank.

https://documents1.worldbank.org/curated/en/502441468299632287/pdf/WPS7194.pdf. Fuchs, Alan, and Francisco Jalles Meneses. 2017. “Regressive or Progressive? The Effect of Tobacco Taxes in Ukraine.” Poverty & Equity Global Practice Working Paper 121.

https://documents1.worldbank.org/curated/en/712811524485287678/pdf/125569-NWP-PUBLIC-POV121-PRWP8227.pdf; Fuchs, Alan, and Francisco Jalles Meneses. 2017. “Are Tobacco Taxes Really Regressive? Evidence from Chile.” Policy Research Working Paper 7988. Washington, D.C.

https://documents1.worldbank.org/curated/en/919121488376958052/pdf/WPS7988.pdf; Fuchs, Alan, Giselle Del Carmen, and Alfred Kechia Mukon. 2018. “Long-Run Impacts of Increasing Tobacco Taxes: Evidence from South Africa.” Washington, D.C.: World Bank.

https://openknowledge.worldbank.org/entities/publication/5123f6d1-af98-5138-a722-d938e16aa41e

https://doi.org/10.1016/j.wss.2022.100081

https://www.worldbank.org/en/topic/jobsandgrowth/overview

https://www.ictd.ac/news/sex-disaggregated-administrative-tax-data

https://www.openownership.org/en/impact/

http://hdl.handle.net/10986/42842

https://cdn.odi.org/media/documents/ODI_Working_paper_Tax_expenditure_reporting_in_Rwanda_and_Uganda.pdf

https://www.taxexpenditures.org/2023/10/08/the-global-tax-expenditures-transparency-index-companion-paper/

https://doi.org/10.35188/UNU-WIDER/2021/103-7

https://ideas.repec.org//p/wbk/wbrwps/10547.html

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).