Since the 2008-2009 global financial crisis, international investors have shown increased appetite for bonds issued by emerging market and developing economies. The stock of bonds issued by their governments and corporations in the hands of international investors has risen from less than $1 trillion in 2009 to $3.5 trillion in 2021, according to our External Wealth of Nations database. Of particular note is the boom in international holdings of bonds issued by China, which were negligible in 2009 ($9 billion) and reached $788 billion at the end of 2021.

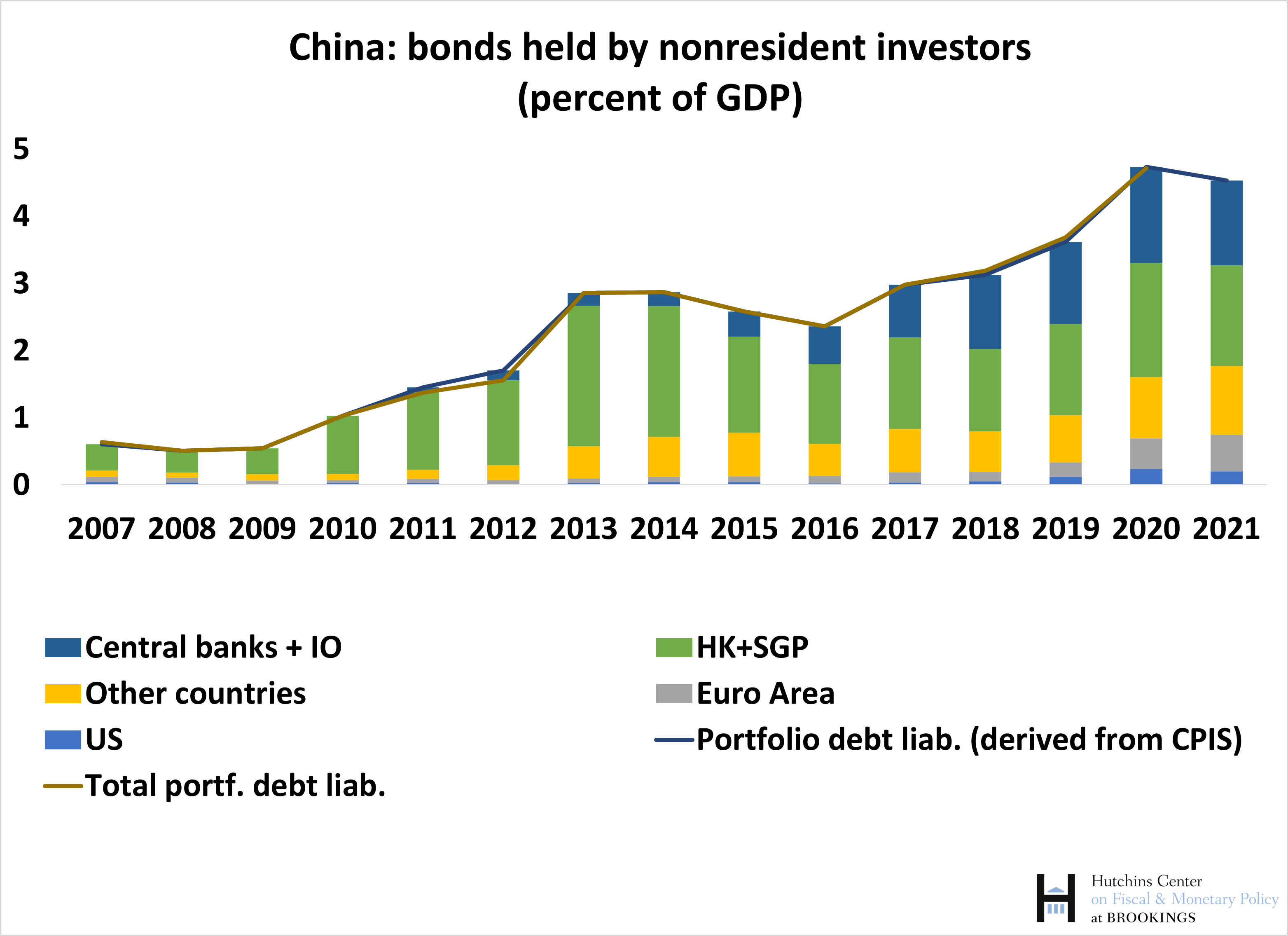

In a paper with Katharina Bergant and Martin Schmitz, we show that the largest holders of Chinese debt are Asian financial centers (especially Hong Kong and Singapore) and foreign central banks, including importantly Russia’s (chart).

The largest international investors—the United States and the euro area—play instead a much more modest role, even though their holdings have been increasing rapidly as well. The increase in foreign purchases of Chinese bonds—notable even as a share of rapidly rising Chinese GDP—reflect both the increased use of the Chinese renminbi as a reserve currency, following its inclusion in the International Monetary Fund’s SDR basket in 2016, and the increase in purchases of Chinese equities and bonds following China’s inclusion in major international indices in 2019.[1] Clearly holdings of international financial centers such as Hong Kong and Singapore will likely be on behalf of investors from other countries, and hence uncertainty remains on the nationality of the ultimate holders of these bonds.

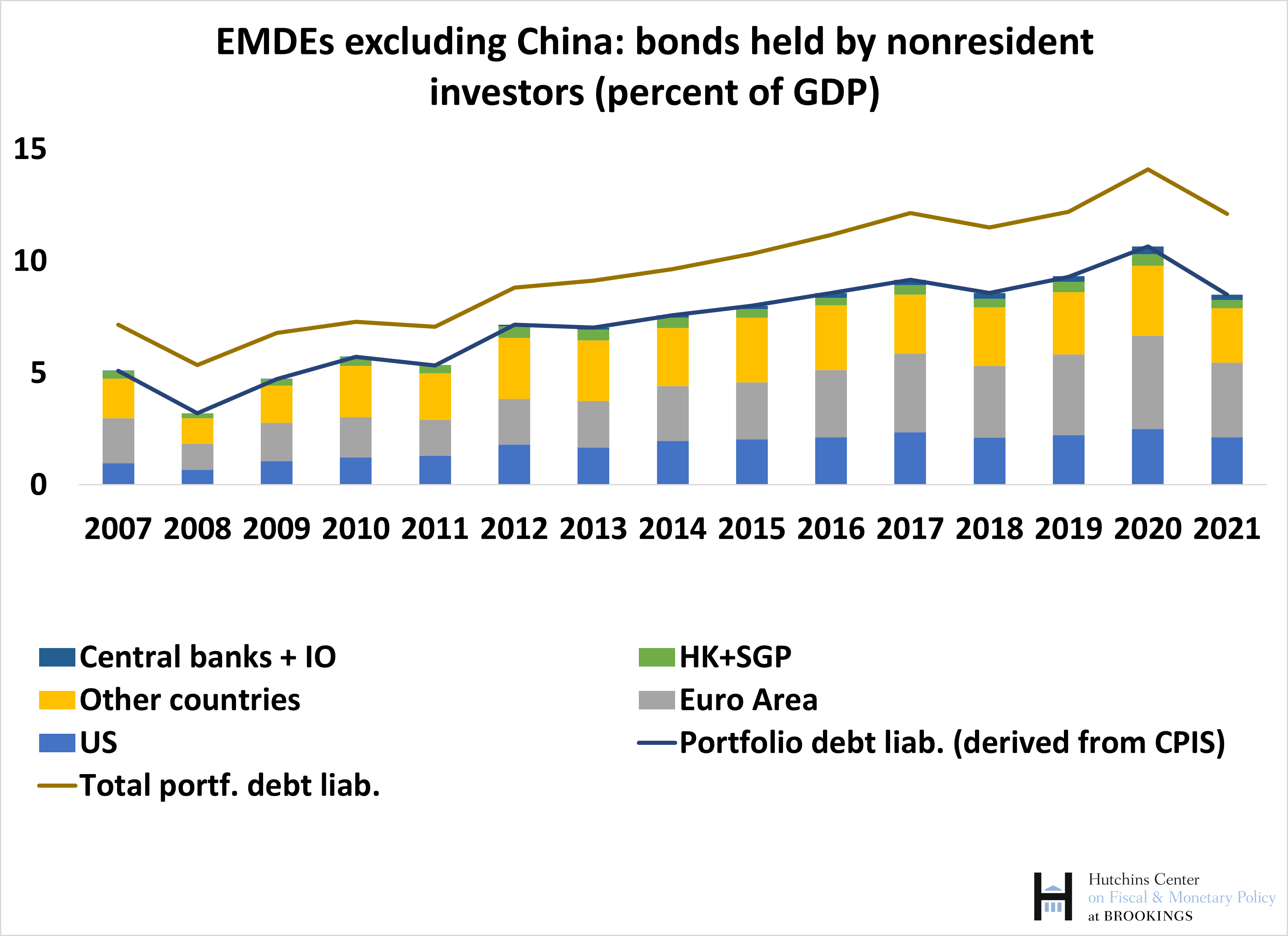

In contrast, the majority of investment in bonds issued by countries such as Mexico, Brazil, Indonesia, Poland, and the Gulf states comes from advanced economies, with the euro area being the largest investor, followed by the United States (chart).

These holdings rose rapidly during the decade 2009-2019 and are higher in absolute terms ($2.7 trillion at end-2021, of which $2 trillion tracked by the CPIS) and as a share of the recipient countries’ GDP compared to holdings in China.

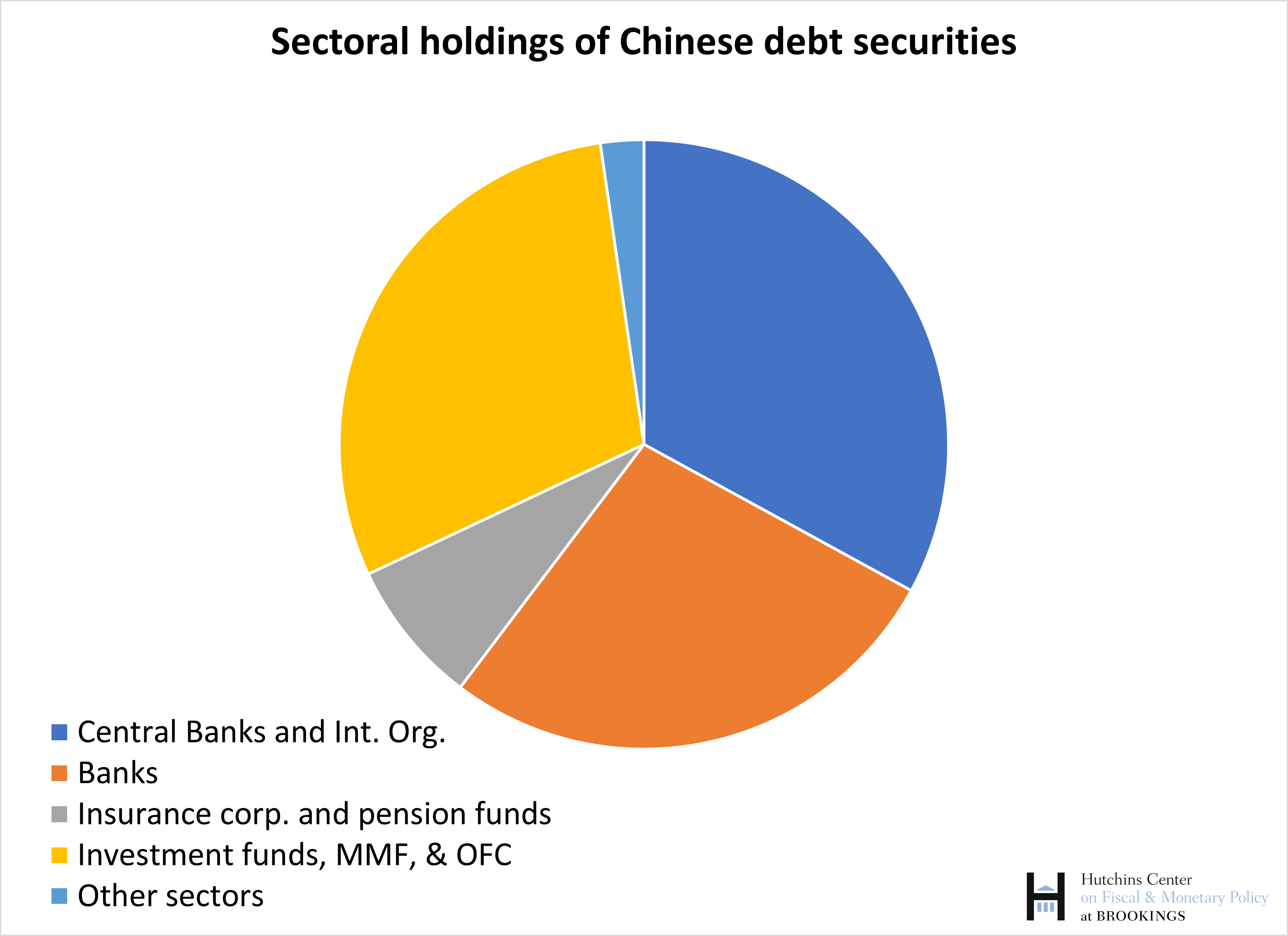

Using detailed information on sectors holding portfolio instruments including bonds shows the differences in the investors who hold Chinese bonds and those who hold bonds issued by other EMs. Estimates for holdings as of December of 2020 (chart) suggest that the largest investors are foreign central banks, followed by banks, while the shares held by investment funds and banks are broadly similar.[2]

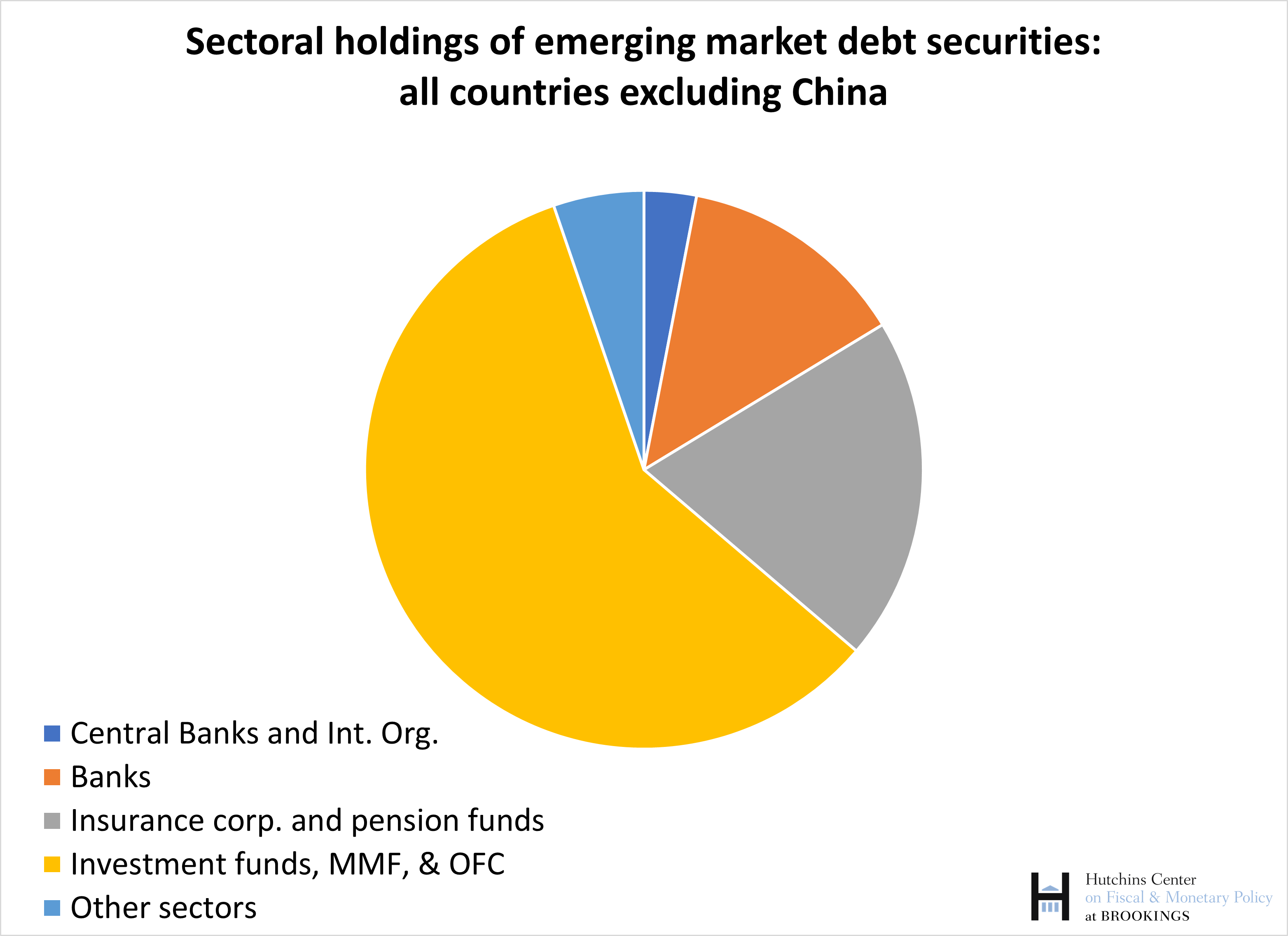

In contrast, investment funds are by far the largest sector investing in bonds issued by EMs excluding China, followed by insurance companies and pension funds and then banks (chart).

The much lower presence of foreign central banks indicates that virtually the entirety of global foreign exchange reserves is held in advanced economies’ currencies or in renminbi.[3]

Offshore finance

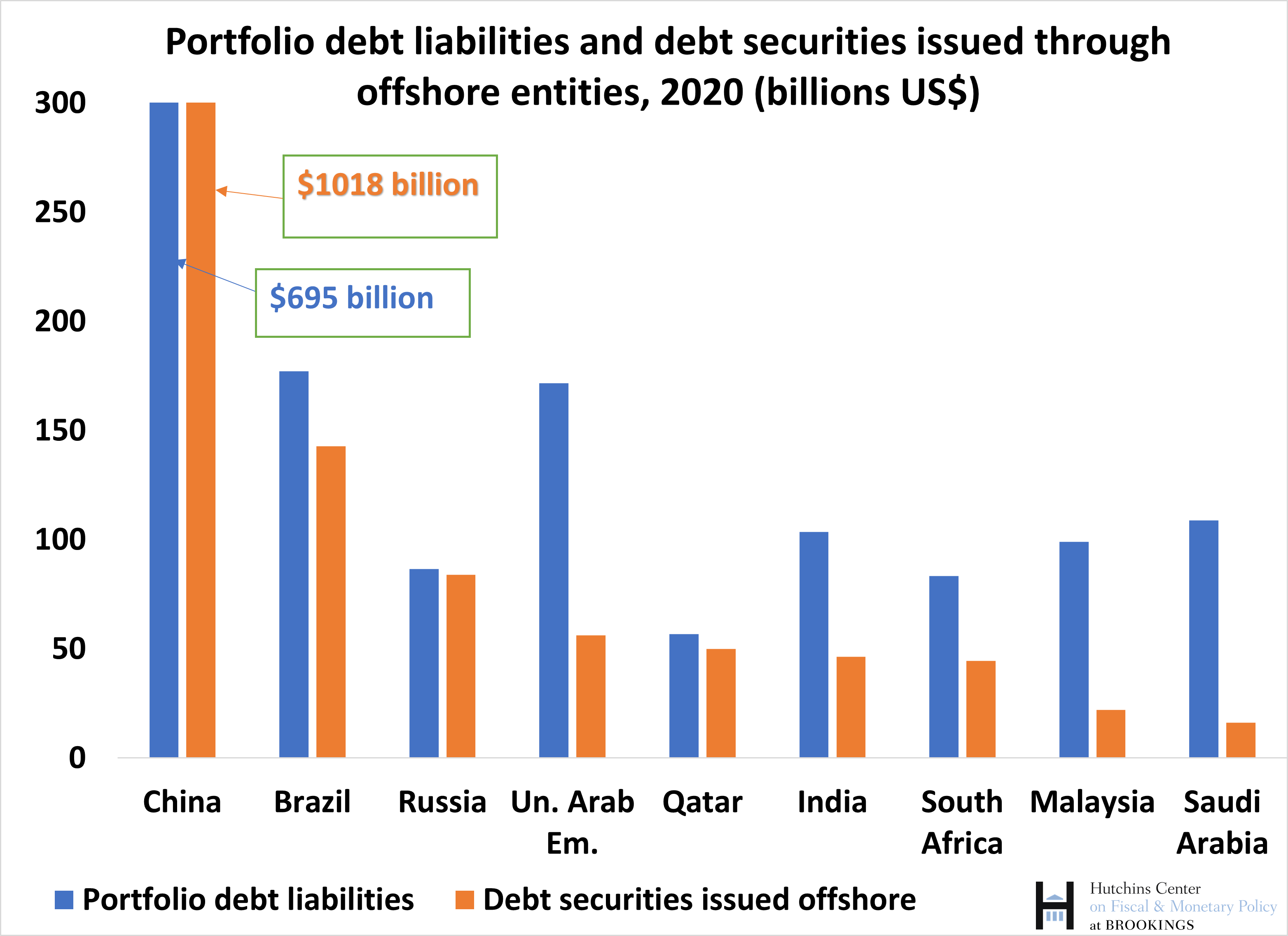

Chinese corporate entities also issue a large amount of bonds through affiliates domiciled in financial centers (such as the Cayman Islands or the British Virgin Islands).[4] In general, firms choose this strategy for tax and regulatory reasons. For China, an additional incentive is the presence of capital controls that affect foreign access to local bond markets. The funds raised by these offshore affiliates are then channeled to the parent company via intercompany loans. Corporate bonds issued through offshore affiliates are mostly denominated in foreign currency (with a primary role for U.S. dollar issues), while bonds issued directly by onshore entities and held by nonresidents include government bonds, which are at least in part denominated in the domestic currency of the issuing country.

The stock of outstanding bonds issued through offshore affiliates exceeded $1 trillion as of December 2020, according to data from the Bank of International Settlements. This amount exceeds total foreign holdings of bonds issued directly by domestic Chinese entities, and is an order of magnitude larger than the amounts issued by Brazil, Russia, South Africa, and Gulf states (chart).

It is difficult to establish general patterns of ownership for those bonds—in surveys such as the CPIS, they are classified as bonds issued by, say, the Cayman Islands rather than China. However, data for the U.S. (as described in Bertaut, Bressler, and Curcuru, 2019) and the euro area (as shown in our paper) suggest that their holdings of bonds issued by offshore affiliates of Chinese corporate entities are broadly of the same order of magnitude as holdings of bonds issued directly by domestic Chinese entities, and therefore represent a relatively modest fraction of China’s offshore-issued bonds.[5] This relatively small share may have to do with the characteristics of the bonds, including the extent of disclosure required by major U.S. and European investment vehicles. It also raises the question of who the main investors in those instruments are, and whether they include resident Chinese investors as well.

In conclusion, foreign investors have been increasing their exposure to emerging market bonds over the past decade. At the same time, the investor base for Chinese bonds held overseas appears to be quite different from the one of the other main issuers, such as Brazil, Indonesia, Mexico, and Poland. Specifically, the weight of U.S. and euro area investors among all foreign investors is much smaller for China, where instead investors from Asia as well as foreign central banks (notably the Central Bank of Russia) play a larger role. Chinese corporate entities also issue a large amount of bonds through offshore affiliates. While it is difficult to establish general patterns of ownership for those bonds, existing data suggest that U.S. and euro area investors do not play a major role in that market either.

The evidence presented in this blog is a small slice of the work in the underlying paper. There we provide stylized facts on nonresident holdings of emerging market bonds and analyze the determinants of euro area investors’ purchases of such securities, using a comprehensive security-level dataset to track net transactions by euro area residents of individual bonds issued by emerging market economies. Euro area investors show a preference for euro-denominated and sovereign EM bonds. Net purchases tend to be higher when the macroeconomic outlook of the respective EMs improves, and U.S. monetary policy is loosened. Conversely, euro area investors—in particular, investment funds—sell emerging market debt when global financial stress is high. In a case study for the BRICS countries, we find that euro area investors treat EM bonds issued through offshore affiliates differently from onshore securities, likely reflecting differences in currency composition. The sell-offs of EM debt in 2018 as well as during the COVID-19 shock only affected securities issued directly by domestic entities, primarily in local currency, while euro area investors held on to securities issued through offshore affiliates.

[1] To link countries investing in EM bonds—and their investor sectors—to destination countries, we make use of data from the International Monetary Fund’s Coordinated Portfolio Investment Survey (CPIS) to help identify the residence of investors in emerging market securities. Countries participating to the survey, conducted annually between 2001 and 2012 and every 6 months thereafter, provide a breakdown by geographical destination of their holdings of foreign equities and bonds. The survey also provides the same breakdown for a group including participating central banks and international organizations. Aggregating investor holdings for each destination country enables us to construct a “derived” measure of bonds held by nonresidents (“portfolio debt liabilities” in balance of payments statistics). These derived liabilities are typically a bit lower than the corresponding liabilities reported by the destination country, given the incomplete investor coverage by the survey. At the same time, the participation to the survey of almost all large investor countries makes the data quite representative.

[2] Data for China rely on reported or estimated sectoral breakdowns for about 85 percent of total holdings identified in the CPIS. The calculation requires several assumptions. The most consequential one for China concerns Hong Kong (the largest investor in Chinese bonds). For that economy we don’t have a sectoral breakdown of its portfolio investment by country in CPIS, but we do have an aggregate breakdown of its total portfolio investment in bonds in its reported IIP. We apply the ratios derived from that breakdown to holdings in each individual destination country, including China. In particular, that breakdown indicates that deposit money banks account for 2/3 of total reported portfolio investment in bonds.

[3] For this group of countries, we can track or estimate investing sectors for over 90 percent of total bond holdings identified in the CPIS.

[4] Bonds may be issued on domestic markets or on international markets. What matters for their classification is the residence of the issuer—bonds issued by the government or a resident corporate entity and bought by a nonresident are classified as portfolio debt liabilities of the issuing country, while bonds issued by an affiliate of an EM corporate entity domiciled offshore are liabilities of the offshore center.

[5] Maggiori et al (2023) discuss in more detail the use of offshore affiliates by Chinese entities for equity and bond finance.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Author

-

Acknowledgements and disclosures

The author is grateful to David Wessel and Henry Hoyle for useful comments.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Destinations for portfolio investment in emerging economies: China is different

February 21, 2023