The paper summarized here is part of the Spring 2024 edition of the Brookings Papers on Economic Activity (BPEA), the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. The conference draft of this paper was presented at the Spring 2024 BPEA Conference on March 28-29, 2024 (conference drafts, recordings, and slides are available via the link). Submit a proposal to present at a future BPEA conference here.

Final version posted: November 2024

Download final paper with discussant comments, discussion summary, and appendix

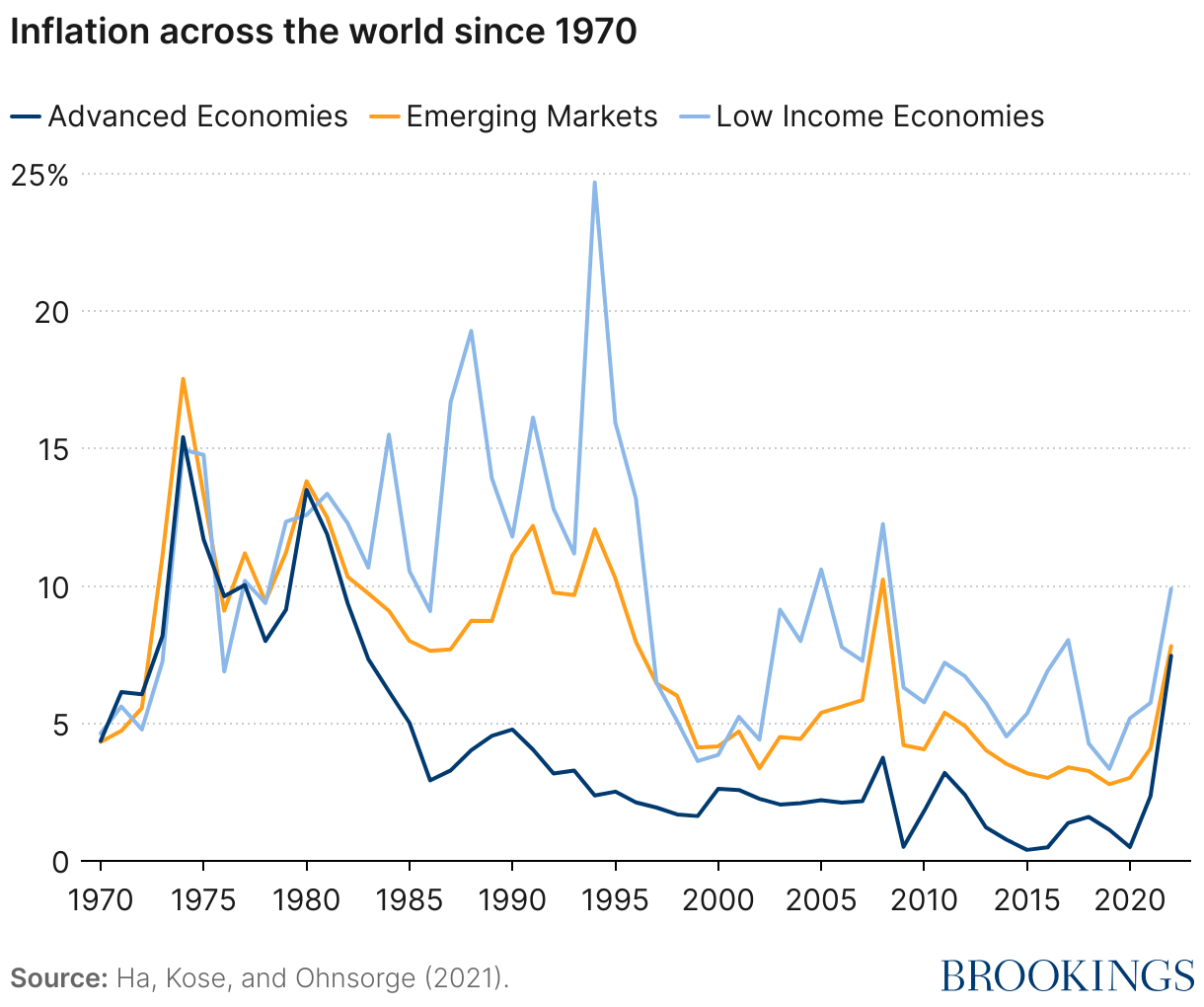

Globalization, market liberalization, and other factors that helped reduce inflation in the four decades before the COVID-19 pandemic may be reversing, complicating central banks’ efforts to tame the post-pandemic inflation surge, suggests a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on March 29. “We argue that several global economic trends will, more likely than not, increase pressures on central banks to inflate,” write the authors—Pierre Yared and Hassan Afrouzi of Columbia University, Marina Halac of Yale University, and Kenneth Rogoff of Harvard University. In the paper—”Changing Central Bank Pressures and Inflation”—they use a simple, long-run aggregate demand-and-supply framework to analyze how economic and political factors generate pressures on central banks and affect the prospects for long-run inflation. Before spiking in the wake of the pandemic, inflation, according to the paper, reached a 40-year trough by the mid-to-late 2010s: 0.40% in advanced economies, 2.79% in emerging markets, and 3.35% in low-income countries.

Factors that helped reduce it include increased trade and globalization; the so-called “Washington Consensus” favoring market liberalization, privatization, and fiscal discipline; the decline of unionization; and central bank reforms that promoted political independence and inflation targeting. International trade, which puts competitive pressure on firms in open economies to keep prices down, increased as a proportion of global gross domestic product (GDP) from 25% to 61% between 1970 and 2008, according to a World Bank report cited in the paper. Meanwhile, the fraction of countries classified as market-oriented increased from 30% to almost 80% between 1985 and 2001. Twenty out of 24 advanced economies experienced a reduction in unionization rates from 1980 to 2010. And 80 out of 113 central banks experienced an improvement in independence between 1990 and 2010. “An important, natural question is whether global inflation in the 2020s will return to the levels of the 2010s, or instead increase to the levels of the 2000s or even the 1990s,” the authors write. “Our model tells us that the answer depends on the likely evolution of economic and political economy forces.” According to the paper, three long-standing developments that drove inflation down appear to be reversing.

- First, globalization has stalled, with trade as a percentage of global GDP falling from its 2008 peak to 57% by 2021. With rising geopolitical tensions (wars in Ukraine and Gaza) and continued protectionist trade policies (applied after the 2007-2009 financial crisis and again after the pandemic), deglobalization likely will continue.

- Second, the International Monetary Fund projects higher government debt, which raises inflationary pressures. It is driven by the debt overhang from pandemic-era government spending and the higher interest rates that governments must pay to finance the debt. Other factors likely to add to fiscal pressures include the acceleration of population aging and the resulting expansion of entitlement spending, increased spending by many countries to achieve net-zero carbon emissions targets, additional defense spending in response to geopolitical tensions, and the expansion of subsidies to support domestic industries.

- Third, the anti-inflation tilt in central bank policies created by the very low pre-pandemic interest rates has ended. Because central banks could not lower short-term interest rates much below zero, they were constrained in their ability to expand monetary policy. Now, with higher rates, they have more room to cut rates to stimulate their economies, boosting inflation.

“Thus … implementing stable and low inflation in future decades may require reforms, such as (even further) strengthened central bank independence or (as unlikely as it may seem) more credible public debt policy, to offset the inflationary pressures on central bankers,” the authors write.

CITATION

Afrouzi, Hassan, Marina Halac, Kenneth Rogoff, and Pierre Yared. 2024. “Changing Central Bank Pressures and Inflation.” Brookings Papers on Economic Activity, Spring: 205–241.

Kohn, Donald. 2024. “Comment on ‘Changing Central Bank Pressures and Inflation.’” Brookings Papers on Economic Activity, Spring: 242–249.

Tenreyro, Silvana. 2024. “Comment on ‘Changing Central Bank Pressures and Inflation.’” Brookings Papers on Economic Activity, Spring: 249–261.

Authors

Authors

Discussants

-

Acknowledgements and disclosures

For helpful comments, the authors are grateful to Janice Eberly, Brett House, Donald Kohn, Jennifer La’O, Christian Moser, Jesse Schreger, Jón Steinsson, Silvana Tenreyro, Shang-Jin Wei, and participants at the Brookings Papers on Economic Activity Spring 2024 Conference. The authors thank Krishna Kamepalli for excellent research assistance.

David Skidmore authored the summary language for this paper. Chris Miller assisted with data visualization.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).