Digital connectivity is helping agricultural producers in sub-Saharan Africa mitigate the risks common to people who rely on farming for income. Digital payments, in particular, enable more secure transactions and traceability, while creating opportunities for recipients to safely save their income between harvests, access insurance products, build credit histories, and reduce the time and cost of receiving payments. Cash, by contrast, is difficult to trace, easy to lose or steal, and leaves no financial record—making it harder for farmers to demonstrate creditworthiness or benefit from targeted government support. Digital payments also reduce the cost of moving money across distances, which matters most in rural areas where travel to collect payments might be costly and require time away from productive work.

Yet despite these disadvantages, cash still dominates agricultural payments. This is one of the most striking findings of the World Bank’s Global Findex 2025, which draws on nationally representative surveys from more than 140 countries and identifies agricultural payment recipients as adults who report receiving payment for the sale of agricultural products or livestock. We use this data to examine why cash remains dominant among agricultural producers and what can be done to change it. We focus on sub-Saharan Africa—the region with the world’s largest share of agricultural producers, who represent about 30% of the adult population (all data are from the Global Findex 2025 database).

Is financial exclusion a barrier to digital payment adoption in agriculture?

At the outset, it may seem that agricultural producers rely on cash because they lack financial accounts. However, that barrier only exists for some. In fact, 57% of agricultural producers in sub-Saharan Africa have some form of financial account in 2024 (Figure 1). This includes 36% with a bank or similar financial institution account and 40% with a mobile money account; 19% had both. The use of mobile money among these adults has expanded rapidly over the past decade, rising from 17% in 2014 to 40% in 2024. Mobile money plays an especially important role in southern and West Africa, where a large share of agricultural payment recipients rely on the convenience and affordability of mobile money accounts.

Yet only 25% of agricultural sellers in sub-Saharan Africa receive their payments directly into an account, including 18% who receive the money into a mobile money account. The rates are even lower for female sellers, who are slightly less likely than men to earn income from agriculture, and far less likely to receive their payments digitally into any account—18% compared with 30% for men.

However, both female and male agricultural producers use other types of digital payments. For example, they do use digital payments to pay bills or merchants at similar rates as their non-agricultural peers.

The question, then, is what constrains the adoption of digital payments for agricultural income and what can be done to encourage a shift away from cash—especially among producers who already have financial accounts, as well as those who do not.

Dethroning cash as king: How to promote digital payments in agriculture

Leveraging mobile money payments

Mobile money accounts, in particular, offer a practical solution to pay farmers and rural residents living far from a bank branch, as they typically have no minimum balance requirements or monthly fees. In fact, mobile money has been pivotal in economies with high rates of digital agricultural payments. In the 10 sub-Saharan African economies with the highest share of adults receiving agricultural payments, recipients who get paid digitally do so mostly through mobile money accounts (Figure 2). In Kenya, Senegal, and Uganda, nearly all digital agricultural sellers receive their money into a mobile money account.

Digitizing the broader agricultural ecosystem

Limited digital adoption across the broader ecosystem reinforces cash as the default for everyday payments. Payments to agricultural suppliers—such as agrovets (small retail shops that sell agricultural inputs like seeds, fertilizers, and pesticides) and rural merchants—often remain entirely cash based. Subsidy systems may also fail to use digital rails to deliver payments, further entrenching cash.

Addressing these challenges requires more than just facilitating account opening or offering farmers the option to be paid digitally. It calls for coordinated efforts with wholesale buyers to modernize payment practices, as well as strengthening the agricultural payments ecosystem of intermediaries and government agriculture programs.

For example, digitalizing agrovet networks—through Quick Response acceptance codes, point-of-sale tools, and subsidy integration—can transform these retail hubs into last-mile financial access points. There are also business incentives: evidence suggests that digitalizing supplier payments can reduce costs for wholesalers.

Investing in digital infrastructure

Digitalizing cash payments also depends on foundational infrastructure. Weak rural broadband coverage remains a constraint in some countries, and handset affordability continues to limit mobile phone ownership among agricultural producers (see Figure 3). In fact, only 66% of producers who receive payments exclusively in cash own a phone.

Expanding phone ownership brings additional downstream benefits—and 72% of all agricultural sellers own a phone. Two-thirds of agriculture sellers that own a phone read text messages, which can be used to deliver technical support and facilitate communication with buyers, even on basic phones.

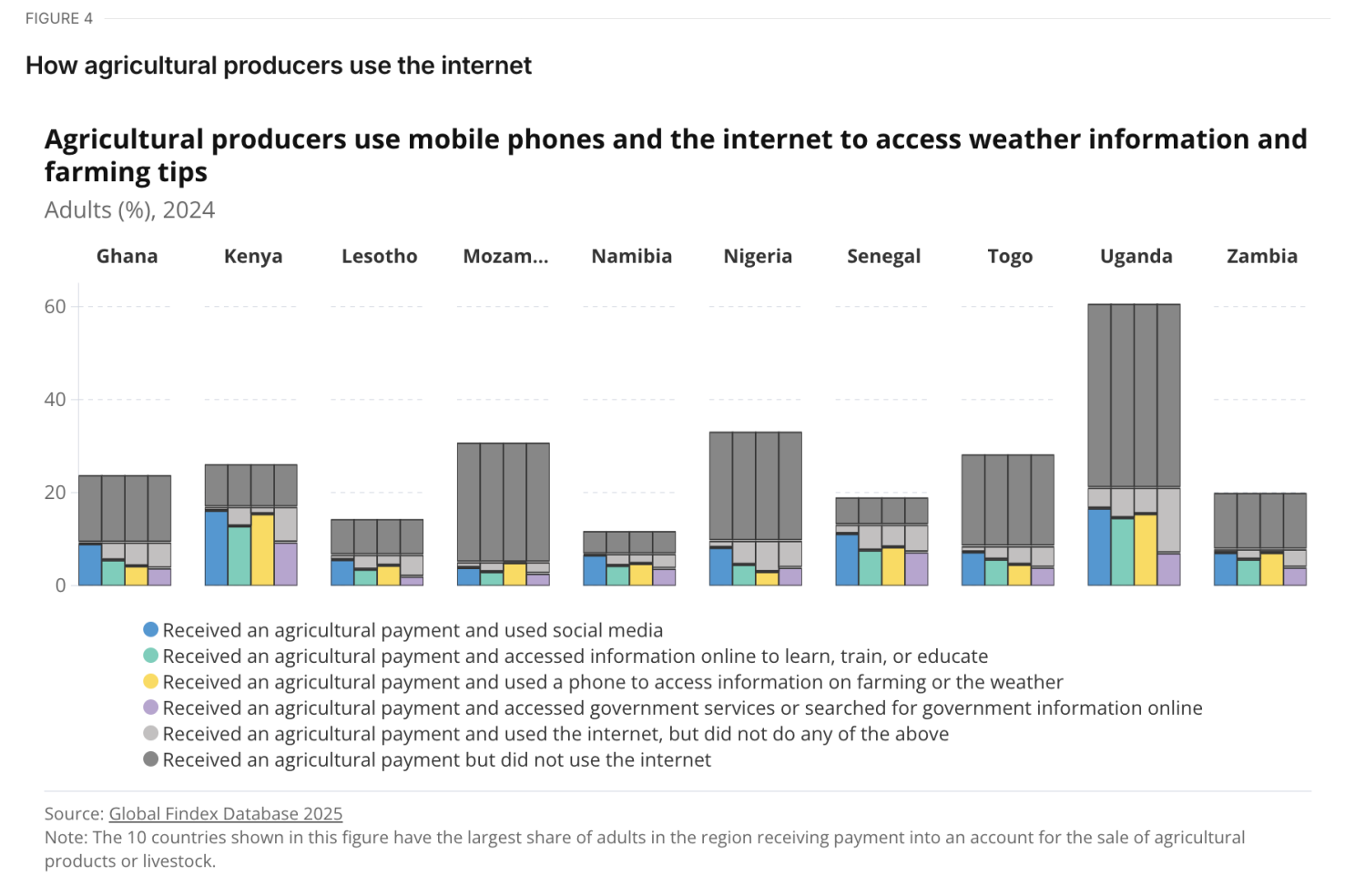

As of 2024, 28% of agricultural producers in sub-Saharan Africa already use the internet. About one in five access farming-specific information, such as weather reports, and just over one in ten use online government services (Figure 4).

Greater internet access could allow agricultural sellers to pair digital payments with valuable information and services, including AI-enabled advisory and financial tools. Digital payments also generate transaction data that can power text- or app-based weather alerts, crop recommendations, and price insights. The same data can support alternative credit scoring, pre-qualified loan offers aligned to crop cycles, and more responsive insurance products.

In sum, digital infrastructure and better connectivity can transform digital payments from being just a transfer of funds to a foundation for smarter farming, better financial access, and greater resilience.

Conclusion

While beneficial, moving beyond cash will not eliminate climate shocks or price volatility. But when agricultural payments generate reliable digital transaction data, they create visibility. That visibility can unlock tailored credit, working capital for agrovets, insurance products, and more responsive subsidy systems. In this way, digitalizing agricultural payments moves beyond convenience to help build the foundation for resilient and inclusive agricultural finance.

The path forward requires coordinated action involving agricultural buyers, governments, and financial service providers. When these pieces align, digital agricultural payments can become scalable infrastructure.

Related Content

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

Agriculture’s cash problem has a digital solution

May 7, 2026