As I was making my New Year’s resolutions a few days ago, I found myself distracted by an old item of news. It said that the civil servant in the United Kingdom who was responsible for increasing the pension age to 67 was to retire at the age of 61 with a pension pot of 1.8 million pounds—another example, the article suggested, of the establishment helping themselves while applying a different set of rules to the rest of us.

Regardless of the rights and wrongs of that particular case, it set me thinking about inequality—not just in the U.K., but more generally for developed countries. There has been a huge amount written in recent years about the problem of growing inequality—ranging from Thomas Piketty’s major treatise on capitalism’s fundamentally dis-equalizing forces, Branko Milanovic’s extraordinary data on world inequality, the Oxford Martin School’s recent work with Citibank, Tony Atkinson’s final book, before his passing last year, expounding his life’s work on tackling inequality, and there is even a network that focuses on global poverty and inequality dynamics. But, the issue that has really captured the public’s imagination and fury has been the individual examples of excess in midst of misery, not least the bankers who receive multi-million dollar bonuses and the entrepreneurs who raid their firm’s pensions schemes and walk away to their mansions. Politicians who have vented about the need to curb executive pay have jumped on this understandable outrage. Yet, to date, nothing has been done. Indeed, the bankers that received almost universal condemnation for their role in the financial crisis are back in the business of awarding themselves eye-watering salaries and bonuses—nothing much, it appears, has changed at all.

Which begs the question “why not?” There are two obvious answers. The first, and hardest to solve, is that the very people awarding themselves huge rewards are the same elite that make the rules. Fundamentally, tackling executive pay and wage inequality more generally is a political problem, not a technical one. But the second reason that pay inequality remains virtually unconstrained, does have an obvious solution. Of course, one can tax the rich more—but very high marginal tax rates merely encourage tax avoidance (and evasion) by those rich enough to hire good tax accountants. Higher taxes on the rich might be part of the solution—but history suggests that it has both economic and political limits.

What else might work? At the more radical end is the idea of a maximum income. Why should anyone earn more than, say, $1 million a year? Just place a cap, some say. However, despite its simplicity and populist appeal, there are obvious drawbacks to such a policy. How do you set the amount? Too low an amount could cause a brain drain as high earners just leave the country and work in places that don’t have such rules; too high and it makes no difference. How do you adjust the cap each year? By inflation? By average wage growth? And there would be a risk that the cap could become a sort of corporate target for the elite, worsening rather than improving wage inequality.

If a cap is a bad idea, what about a ratio? For example, some suggest that a limit should be placed on the ratio between the income of the chief executive and that of the lowest paid. This is getting closer to something that tackles inequality, rather than just high pay. But what ratio to choose? The highest to the lowest? The highest to the average? The 90th percentile to the 50th? Or the 10th? Each has its appeal, but they all suffer from the same flaw: They attempt to describe wage inequality using only two values. Consider a firm where all the employees earn the same good wage—but the owner pays themselves 100 times more. The ratio of highest to lowest (or average) would portray this as a very unequal firm; the ratio of the 90th percentile pay to any other percentile would portray it as a paragon of equality.

Fortunately, there is a simple solution to this problem and astonishingly, to my knowledge, it has never been attempted. What is needed to reduce wage inequality within firms is neither a cap nor a ratio—it is an inequality index—and the economics profession has worked on these for decades. In particular, there are well established indices of inequality that are specifically designed to look at the full distribution of wages or income—not just two values—and produce a single number that describes how equal, or unequal, that distribution is. The best known of these indices is the Gini index, which provides a number between 0 (perfect equality) and 1 (one fat cat gets it all) for any distribution of incomes. However, less known, is that there is a whole class of inequality indices—known as the generalized entropy measures—that enable you to decide whether you care more about inequality at the bottom end of the distribution, the middle, or the top. In these formulas, a policymaker can choose a value for a parameter, α. If α=0, then the index worries more about inequality among the poor; when α=1, the index puts more emphasis on inequality in the middle of the distribution; and when α=2, it stresses inequality at the top of the distribution (see here for how the math works).

Normally, in public policy, we are most worried about the poor; but in the discussions on wage inequality, what we are most concerned with is huge inequality at the top of the distribution. Hence an index with a high value of α makes most sense.

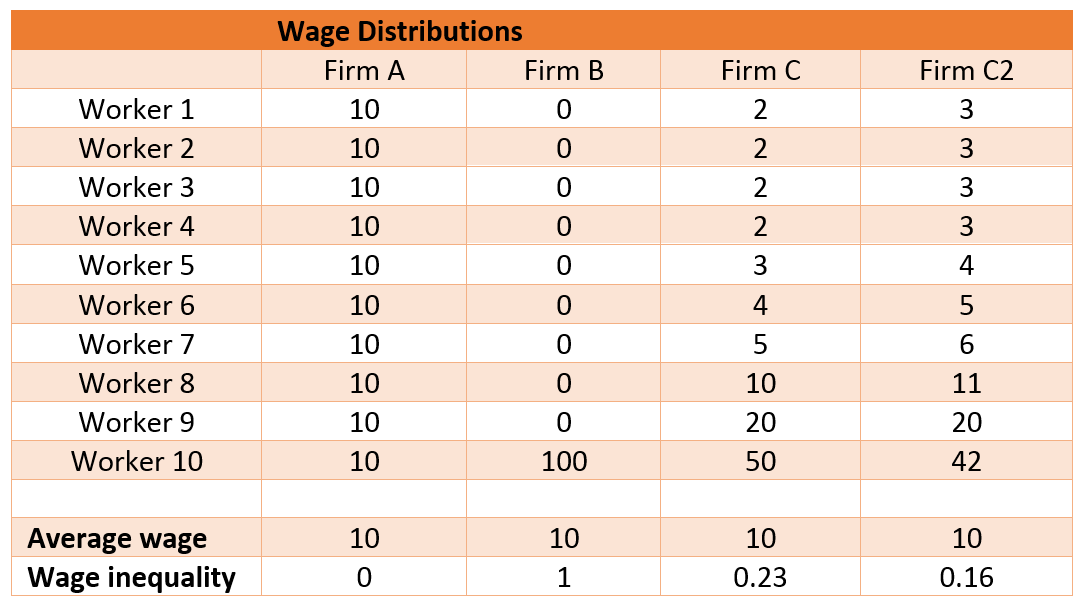

Table 1 provides a simple example for three firms with different wage distributions (for simplicity, we have shown firms with 10 employees, but it works for any number).

Table 1: Wage inequality for three different distributions of wages

Note: Wage inequality calculated using the Relative Entropy index with α=2. The Relative Entropy index is a generalized entropy index normalized to lie between 0 and 1.

For Firm A, everyone gets the same wage; consequently, wage inequality is 0. Firm B is the extreme opposite in which nine of the workers receive nothing while one owner receives a very high income—this yields an inequality score of 1. Firm C represents the more typical case in which most workers get relatively low wages, but a minority of senior management and executives get significantly more with the chief executive earning 25 times the pay of the poorest paid. The overall wage inequality score in this case is 23 percent, but this is still an extremely high value for this index.

Consider how such an index might be used in practice to reduce wage inequality. The first and easiest would be simply to require firms to calculate and publish their wage inequality figure. Firms have all the information that could be calculate through a simple formula on a spreadsheet. Perhaps small firms could be exempt, but no firm with more than, say, 100 employees lacks the capacity to calculate such a figure.

More controversially, would be to set a limit, which is to require firms not to have wage inequality above a certain value. The value could be chosen to only catch the most egregiously unequal firms—the top 1 or 5 percent. Firms exceeding the wage inequality threshold might be subject to a fine, or perhaps an inequality tax based on the value of their score, providing a strong financial incentive for firms to take wage inequality seriously.

The beauty of this approach is that it keeps decisions on what people should be paid with the firm. If firms wish to pay very high wages, they are free to do so, but, if they wish to avoid the inequality tax, they must share the gains with a much larger share of the workforce. Thus, instead of focusing on the pay of particular individuals, or chief executives, the wage inequality index approach changes the incentives for firms themselves, encouraging them to share the wealth around. Consider Table 1 again and imagine that Firm C has been told that it cannot have wage inequality above 20 percent—how might the board of this firm achieve this, while keeping the wage bill (shown by the average wage) exactly the same? Firm C2 shows one way to achieve this: Reducing the most highly paid worker’s wage from 50 to 42 provides space to increase the wages of all other workers except the top two. Indeed the bottom four workers get a 50 percent increase and yet the total wage bill for the firm remains the same, and the chief executive still receives 14 times as much as the lowest paid. Wage inequality declines from an egregious 23 percent, to a (still high) 16 percent.

Of course, the practical implementation of such an approach would require a lot of work. But why not start simply with the publication of wage inequality figures? That only requires a set of guidelines and a spreadsheet. That simple measure would enable us all to see just how bad (or good) the problem of wage inequality is and could simulate a debate about how to provide firms with real incentives for addressing it. And that would be a New Year’s resolution worth keeping.

To come: How might a similar approach be used to tackle inequality in developing countries?

Related Content

Author

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

A New Year’s resolution to address wage inequality in firms

January 8, 2018