Well before the first Medicare cards were printed, the government began subsidizing health care spending through a provision that continues to this day: the itemized medical deduction (IMD), which allows taxpayers to deduct certain out-of-pocket medical spending from their income in the calculation of their taxes. While the IMD was originally intended to provide tax relief to those incurring high medical costs, it currently serves only a small fraction of that population due to the way its design interacts with other features of the tax code and large barriers to claiming the IMD that result in unclaimed tax savings. The combination of these attributes means that those most in need of relief from high medical spending tend to not benefit from the IMD.

Reforming the structure of the IMD could expand its reach to more people with a high medical cost burden, and streamlining and simplifying the claiming process could increase the share of tax savings that are claimed. However, policymakers should revisit the IMD as a way to address the financial risks of deterioration in health relative to alternatives, such as expanding public health insurance programs or subsidizing private health insurance coverage.

Background and significance

The IMD was created by the Revenue Act of 1942. This landmark legislation expanded the federal income tax from a system that applied only to a thin slice of high-income households to a large-scale levy to finance the ongoing war effort. The rationale behind the IMD was to cushion lower-income families from “undue hardship” created by the tax system on taxpayers with “extraordinary” medical expenses (Sierk 1966). Since only 14% of the U.S. population had health insurance coverage at the time the act was passed, it is likely that many taxpayers qualified for relief from this provision.1

Some policy changes since the Revenue Act of 1942 have led to modifications of the income threshold and changes in the items that can be included as qualifying medical expenses. However, the IMD has largely remained intact through eight decades of significant changes in the role the government plays in subsidizing health care, including IRS rulings that allowed for the tax-exempt status of employer-sponsored health insurance, the introduction of Medicare and Medicaid in 1965, and the implementation of the Affordable Care Act (ACA) in 2014.

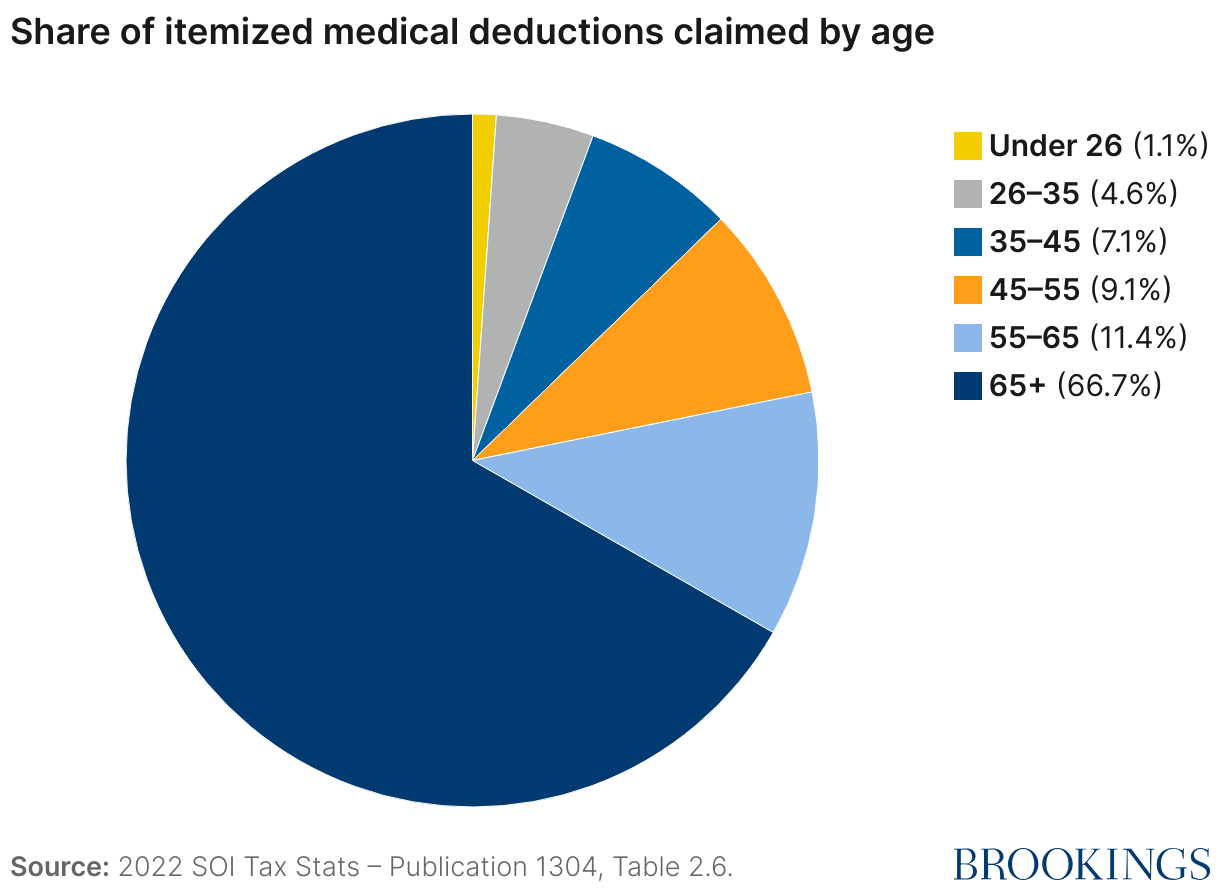

Today, the IMD represents a notable share of out-of-pocket medical spending and forgone tax revenue. In 2022, taxpayers deducted $92.9 billion in IMDs, almost one fifth of total out-of-pocket medical spending that year.2 These deductions equated to an estimated $9.5-12.3 billion in forgone federal tax revenue.3 Measured against other ways the tax code subsidizes health care spending—such as premium tax credits to purchase health insurance through exchanges or the exclusion of employer-sponsored health insurance from income taxes—the forgone revenue from the IMD is more modest. However, the IMD is still consequential, especially for those 65 and older: In 2022, approximately $62 billion—or 2/3 of total IMDs—were claimed by taxpayers over 65 (see Figure 1).

How does the IMD work, and who receives the tax savings?

The itemized medical deduction allows taxpayers to deduct certain out-of-pocket health care costs from their taxable income. Deductible medical expenses include amounts spent out-of-pocket for the diagnosis, treatment, or prevention of disease, including payments to doctors, dentists, and other licensed practitioners; hospital and nursing home care; prescription drugs; and medical equipment like wheelchairs and hearing aids.4 Deductible expenses also include insurance premiums for medical care that are not paid by an employer, transportation costs to receive medical care, improvements made to a home to accommodate a disabling condition like ramps or bathroom modifications, or long-term care services for a chronically ill individual.5 It is worth noting that some of the allowable expenses—for instance, capital-intensive expenses to modify a home—can only be claimed as deductions by those who have the resources to pay for these expenses in the first place. Only medical expenses paid out-of-pocket that exceed a particular threshold—7.5% of the taxpayer’s Adjusted Gross Income (AGI) in 2025—can be included on one’s tax return.

To benefit from the itemized medical deduction, a taxpayer must first choose to itemize his or her deductions. Taxpayers have the choice of claiming the standard deduction or itemizing their deductions and generally choose the option that minimizes their tax liability. In addition to medical expenses above 7.5% of AGI, itemized deductions include other provisions, such as interest paid on a home mortgage, state and local taxes, and charitable donations; thus, the decision to itemize depends on how the total of these items compares to the standard deduction. In 2024, the standard deduction was $14,600 for a single taxpayer and $29,200 for taxpayers married filing jointly.

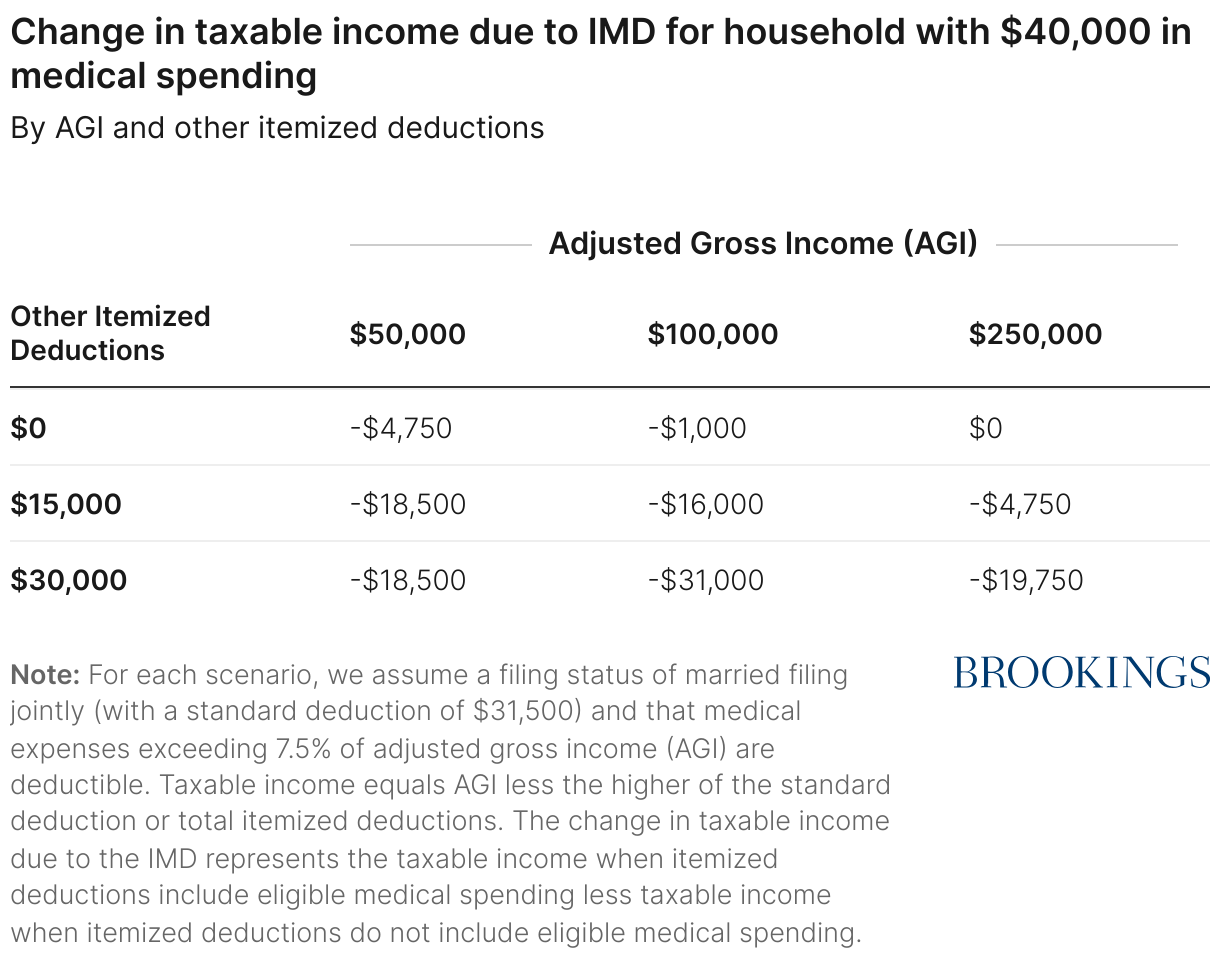

Table 1 shows how the IMD affects the taxable income of a household with $40,000 in medical spending for different values of adjusted gross income (AGI) and other itemized deductions. All else equal, someone with the same medical spending but higher AGI can include less of their medical spending on their tax return than someone with lower AGI because only the amount that exceeds 7.5% of AGI is deductible. This can be seen by moving across columns to the right: Holding their other itemized deductions fixed, households with higher incomes see a smaller reduction in their taxable income.

However, the deduction becomes more valuable for taxpayers with more itemized deductions aside from medical spending, such as mortgage interest or property taxes. This can be seen by moving down each row: As other itemized deductions increase, the reduction in taxable income from the IMD is larger. Since households with more resources tend to have both higher incomes and higher itemized deductions besides medical spending, the IMD tends to result in greater reductions in taxable income among these higher-resourced taxpayers.

The tax savings from the IMD can be determined by calculating the tax liability with and without deductible medical expenses included and finding the difference. For a given reduction in taxable income, the tax savings is typically larger for higher-income taxpayers who are in higher tax brackets, reinforcing the relationship described above.6

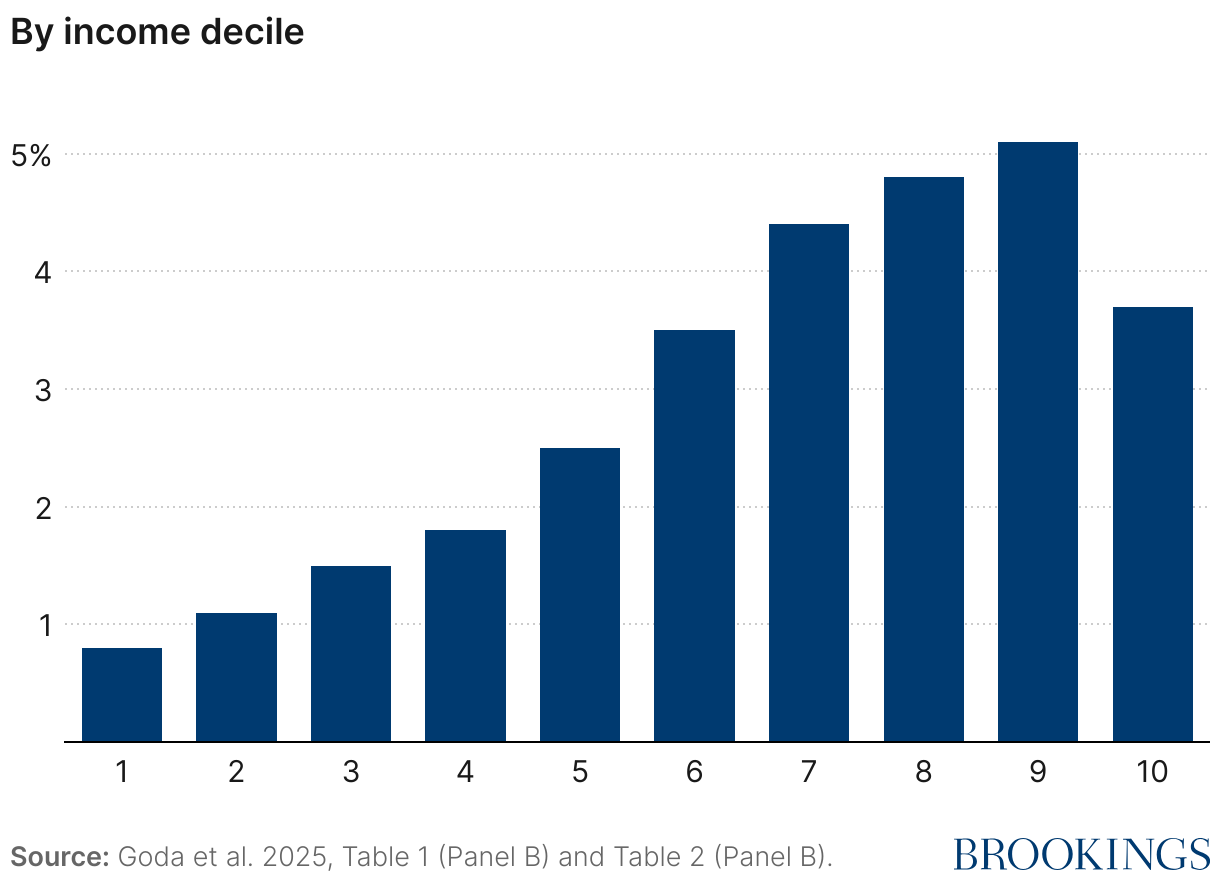

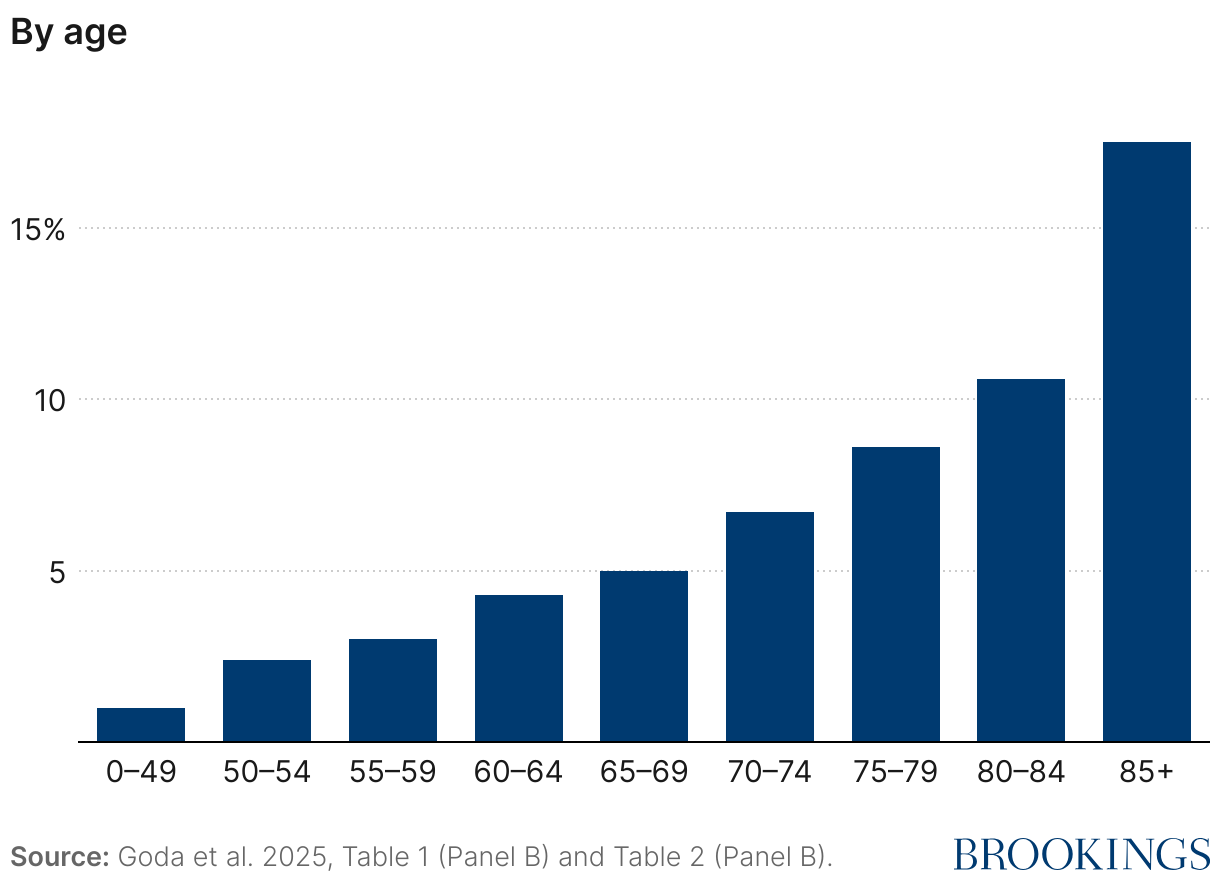

How the tax savings are distributed across the population depends on the relationship between income, out-of-pocket medical spending, and the value of other itemized deductions. Prior work examined the distribution of IMD tax savings and found that they are heavily skewed towards higher-income and older taxpayers (Goda et al. 2025). Approximately 94% of the tax savings accrue to the top half of the income distribution and 41% accrue to the top 10%. This is because both itemization rates and marginal tax rates increase with income, and these factors are stronger than the effect of the lower threshold. Figure 2 shows the share claiming IMDs generally increases by income and by age. Despite the fact that higher income taxpayers face a higher income threshold, claiming rates go up with income for all but the highest decile of the income distributions. Claiming rates increase from only 1% of taxpayers under age 50 to more than one in six taxpayers – 17.5% – age 85 and over. These data underscore the IMD’s importance as a mechanism for financing health care costs at older ages.

Figure 2: Share claiming Itemized Medical Deduction, 2018-2019

How well does the IMD deliver benefits to those with high medical costs?

The notional goal of the IMD is to provide relief to people with high out-of-pocket medical spending. However, the IMD falls short of this objective in three key ways.

- Most people with high medical costs are not eligible for tax relief from the IMD.

The first way the IMD deviates from the broader objective is that not everyone with medical costs above 7.5% of their AGI is even eligible for tax relief from the IMD. This results from the requirement that taxpayers itemize their deductions and have positive taxable income to deduct. According to data from the nationally representative Health and Retirement Study (HRS) in 2018, while approximately 47.1% of households age 50 and over have medical spending above 7.5% of their AGI, only 6.0% are eligible to receive additional federal tax savings due to their high medical spending. In combination with the fact that marginal tax rates rise with income, the requirements above result in tax savings that are concentrated among high-income households—who are also likely to have other means to cushion losses from high medical expenses.

- A substantial share of tax savings from the IMD are left unclaimed.

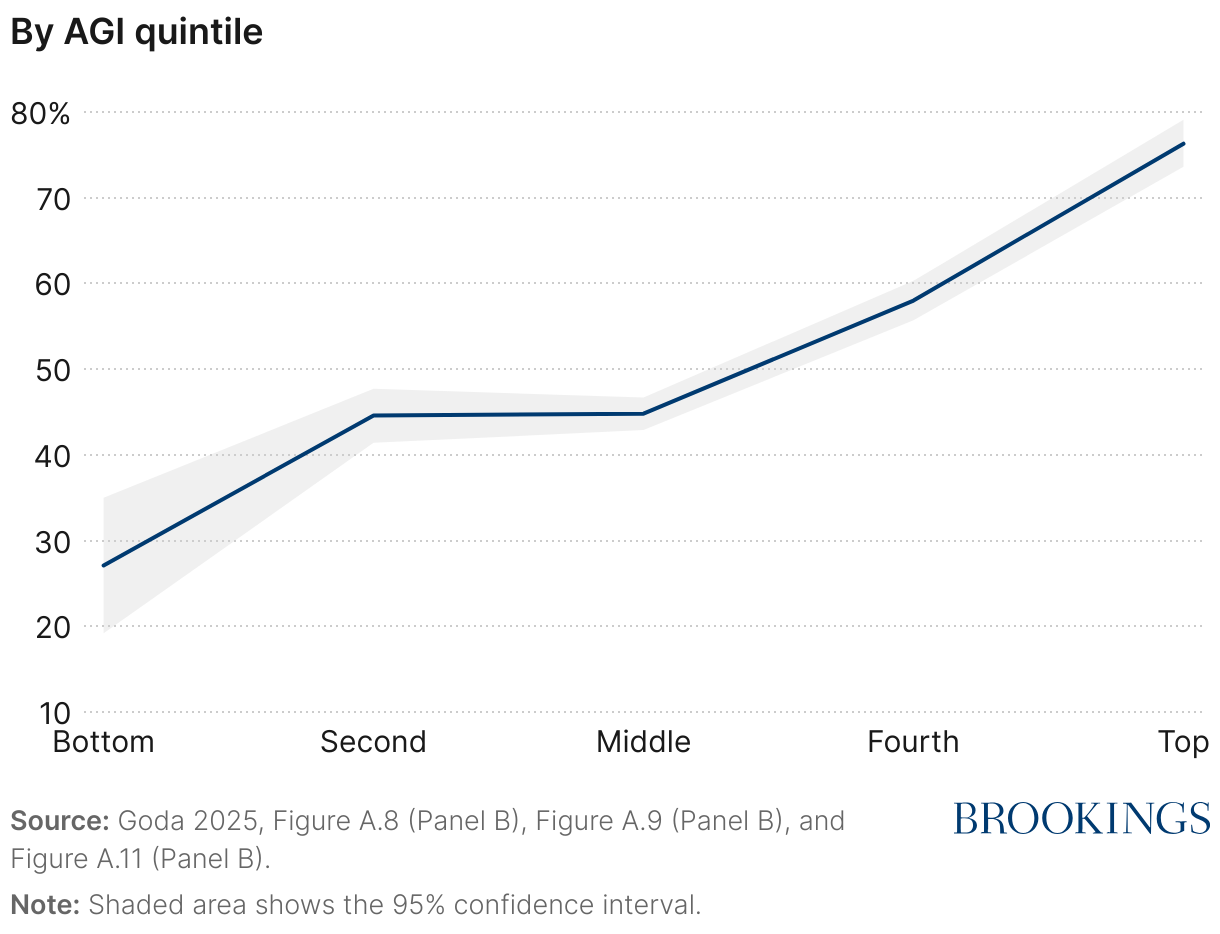

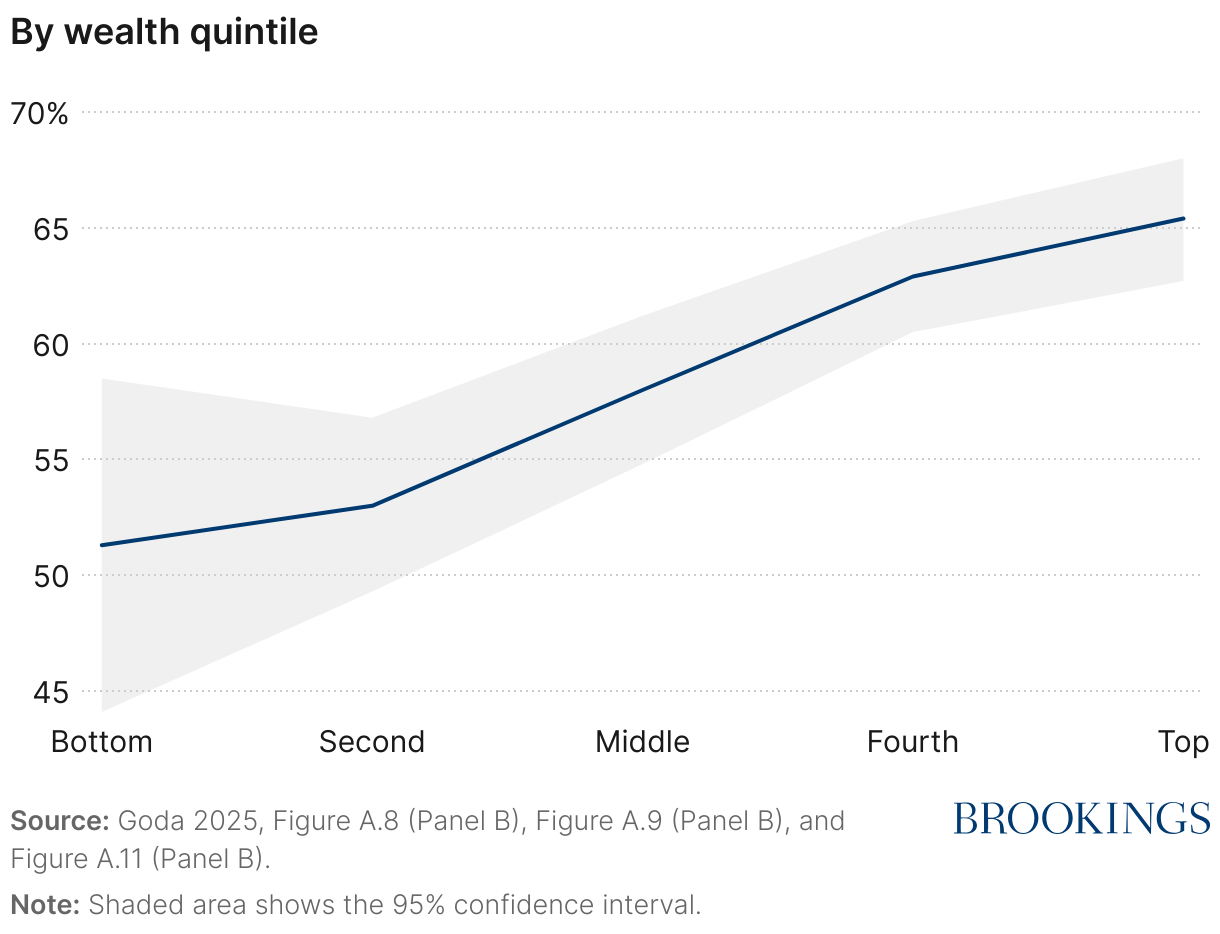

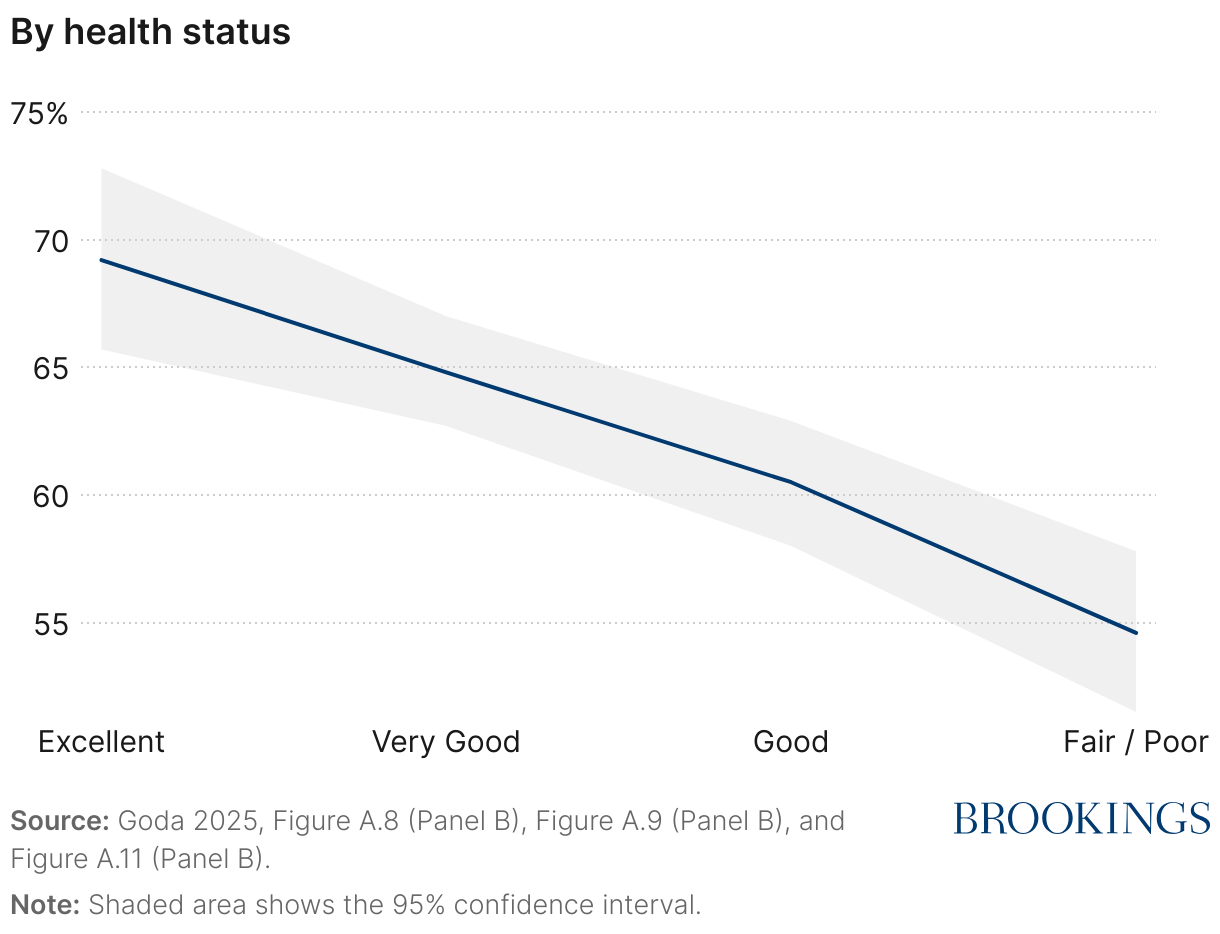

Taking advantage of the IMD requires knowing that it exists, keeping records of out-of-pocket expenses, determining eligibility, and filing the appropriate tax forms. In previous work analyzing the HRS, I found that among older households, approximately 62% of potential tax savings were claimed over the 1996-2012 period (Goda 2025). The ratio of claimed-to-potential tax savings was even lower among those with lower levels of income and wealth and those in poorer health (see Figure 3). Thus, the fact that not all available benefits are claimed counteracts some of the IMD’s effectiveness in redistributing to those who incur high health care costs.

Figure 3: Share of potential tax savings from Itemized Medical Deduction that are claimed

- Compliance costs eliminate most of the benefits that claimants receive.

The fact that many of those eligible for the IMD fail to claim it reveals that there are meaningful barriers to claiming. One can quantify the economic burden of a tax deduction by assuming that those who are not claiming are rationally weighing the costs of claiming—in terms of time and hassle—against the benefits—in terms of tax savings—and taking the action associated with greater economic benefits.7 Data from the HRS suggest that the implied time and hassle costs of claiming the IMD are large relative to the expected tax savings: On average, the implied costs are around $1,000, while the tax savings are approximately $1,300. In other words, the hassle and complexity of claiming the IMD is both keeping people from utilizing it and reducing the net economic benefit to those who do claim it.

How have recent policy changes affected the IMD?

The Affordable Care Act (ACA) raised the AGI threshold for claiming the itemized medical expense deduction from 7.5% to 10% for most taxpayers beginning in 2013, though taxpayers aged 65 and older were temporarily exempted from the increase until 2017. The Tax Cuts and Jobs Act (TCJA), signed into law in December 2017, temporarily reversed this change, restoring the 7.5% threshold for all taxpayers for tax years 2017 and 2018. Subsequent legislation extended the lower threshold and made it permanent in 2020.

The TCJA also included a large increase in the standard deduction. A higher standard deduction results in fewer taxpayers benefitting from itemizing their deductions and thus fewer tax returns itemizing. However, the taxpayers who still choose to itemize when the standard deduction is higher have higher average deductions. In 2017, when the standard deduction was much lower, 30.6% of tax returns claimed the itemized deduction and 6.7% claimed the IMD, while in 2018, 11.4% of tax returns itemized and 3.0% claimed the IMD. However, among those who claimed the itemized medical deduction, the average amount claimed increased from $10,081 to $17,069. On net, the changes in the TCJA reduced the forgone tax revenues from the IMD and also concentrated the tax savings among an even smaller subset of the population who tended to be older and have higher income (Goda et al. 2025).8

In July 2025, the One Big Beautiful Bill Act (OBBBA) was passed by Congress and signed into law by President Donald Trump. Among the hundreds of provisions in its approximately 1,000 pages, OBBBA contains several changes to federal health care programs, such as imposing work requirements on Medicaid enrollees starting in 2027. In addition, the enhanced Premium Tax Credits in the American Rescue Plan are scheduled to expire at the end of 2025. Combined, the Congressional Budget Office predicts that these changes will reduce health insurance coverage for an estimated 16 million people by 2034, which could impact the amount of unreimbursed medical spending subject to the IMD.

The bill made also several changes to itemized deductions that more directly impact the IMD. These changes include:

- Higher standard deduction. The TCJA nearly doubled the standard deduction starting in 2018, increasing it from $6,500 to $12,000 for single filers and $13,000 to $24,000 for married couples filing jointly. This increase was set to expire at the end of 2025, but the OBBBA made higher levels permanent and set them to $15,750 for single filers and $31,500 for married couples filing jointly.

- Increase in State and Local Tax (SALT) deduction. The OBBBA temporarily increased the cap on the itemized deduction for state and local taxes from $10,000 to $40,000 for 2025, increasing by 1% each year until 2029. This cap phases out for high earners and is scheduled to revert back to $10,000 after 2029.

- Tax treatment of charitable contributions. A tax deduction for charitable contributions made by an individual taking the standard deduction is now allowed for cash donations up to $1,000 (or $2,000 for married couples filing jointly). Those who itemize their deductions are now subject to an income floor, where contributions that exceed 0.5% of AGI are allowed.

The higher standard deduction was carried forward from the 2017 TCJA, but the others are new to the 2025 bill. A higher cap on the SALT deduction increases the likelihood that someone will benefit from itemizing their deductions, so all else equal, this change will result in more tax returns claiming the IMD. Conversely, allowing some charitable donations to be deducted without itemizing and reducing the amount that can be included in itemized deductions might push slightly in the other direction.

On net, it is likely that these changes will result in some increases in the share of taxpayers claiming the IMD and a slightly lower average amount claimed over the next few years relative to recent history. However, these changes will likely be small relative to the changes from 2017 to 2018 stemming from the TCJA.

How should policymakers think about the IMD going forward?

The IMD operates as a form of insurance: If someone experiences a health shock that results in higher medical spending, lower income, or both, the IMD may reduce the tax liability they owe with a subsidy rate related to one’s marginal tax rate. However, unlike health insurance payments that are often made directly from insurers to providers at or around the time of service, the tax relief from the IMD is generally delivered many months later. Moreover, taking advantage of it requires knowing that it exists, keeping records of out-of-pocket expenses, determining eligibility, and filing the appropriate tax forms.

Taking a step back, it is important to evaluate the IMD as a policy lever relative to other potential policies, such as expanding public insurance programs like Medicaid or Medicare or encouraging private insurance coverage through subsidies, tax exclusions, or more generous government payments to providers. A complete comparison requires not only understanding the degree to which benefits are targeted to high medical spenders but also incorporating potential positive impacts on risk protection and/or health and any distortionary impacts on other economic decisions. However, the high implied economic burden of claiming a medical subsidy through the tax code combined with its redistributive features suggests that replacing the IMD with, for example, more generous coverage for long-term services and supports would likely improve risk protection more efficiently.

Within the existing framework, the IMD would be more likely to insure health risks by increasing claiming among those eligible and/or expanding eligibility among those with high medical spending.

What interventions could increase IMD claiming among those eligible?

Many forms of government benefits are not fully claimed by those who are eligible, and understanding why can help inform appropriate policy actions. In the case of the IMD, the data show that households in the Health and Retirement Study are more likely to claim the IMD when they have been eligible for the IMD multiple times, suggesting that households might learn about the IMD over time or are able to streamline the tracking of their medical spending. It is worth noting that interventions that increase claiming among those eligible are likely to make the IMD more progressive, since a smaller share of eligible low-income households claim the IMD.

- Reduce the administrative burdens associated with claiming the IMD. The most ambitious intervention would be to require health care providers and insurers to track and report eligible amounts that an individual paid in a new Form 1098-M, similar to Form 1098 that requires financial institutions to report mortgage interest paid or Form 1098-E that does the same for student loan interest. The requirements would apply to amounts above a dollar threshold.9 These amounts would have to be adjusted by the taxpayer up or down depending on whether they were paid through a tax-favored health savings account or the individual paid for other expenses eligible for deduction that are not within scope of Form 1098-M. While likely to reduce the frictions in claiming the IMD, this reform would likely be costly for providers to comply with.

- Increase awareness of the IMD through educational campaigns. While unlikely to have the same impact as third-party reporting, efforts by tax preparers, health care providers, and the IRS to increase awareness of the IMD could be meaningful given the complexity involved in understanding what expenses are deductible and how the IMD works.10

What policy changes would expand eligibility among high medical spenders without dramatically increasing the cost to the government?

The changes described below modify the structure of the IMD and serve to either increase the tax savings available to lower-income households or enhance the progressivity of the IMD by reducing the tax savings available to higher-income households. Each can be calibrated to “right-size” the subsidy as the structure of the tax subsidy is largely independent of the optimal level of the subsidy.

- Increase the IMD income floor. The most straightforward way to reduce the concentration of tax savings among higher-income households is to increase the AGI threshold that medical spending must exceed in order to be eligible. Increasing the income floor from 7.5% of AGI to 30% of AGI results in the bottom half of the income distribution incurring 76.5% of eligible medical spending. Prior work suggests that this change in isolation would reduce forgone tax revenues to approximately 26% of its current level.

- Remove the requirement to itemize. Higher-income households are more likely to itemize their deductions due to factors like higher homeownership rates that result in itemized deductions larger than the standard deduction. Thus, removing the requirement to itemize would increase the share of eligible households at lower points of the income distribution. While lifting this requirement alone would be costly—resulting in approximately 382% higher forgone revenues—prior research suggests that combining it with an income floor of 30% of AGI could change the distribution of tax savings across income in a roughly budget-neutral way (Goda et al. 2025).

- Convert the subsidy from a deduction to a refundable credit. As in many areas of tax policy, deductions are more valuable to high-income taxpayers due to the progressive income tax schedule. In contrast, the value of a refundable tax credit is independent of income and reduces someone’s taxes dollar-for-dollar. Expanding access by converting the IMD to a refundable credit worth 2% of out-of-pocket spending that exceeds 7.5% of AGI would be approximately budget-neutral and would lead to tax savings that are progressive, on net (Goda et al. 2025).

- Reduce the scope of allowable medical spending. The types of services that can be included as an itemized medical deduction have expanded over time through court rulings and evolving medical standards. Some of the allowable expenses—for instance, capital expenses to accommodate a disability—are likely to accrue to taxpayers with more resources. Refocusing the list of allowable expenses would reduce costs and could make the subsidy more equitable.

The IMD was originated in 1942 with a worthy goal—to mitigate the tax burden on those facing hardship from high health care costs at a time when the tax code was expanding significantly and there was little formal protection against those risks. However, today the IMD is costly to claim, and its benefits are concentrated among a small share of the households with high medical costs—disproportionately those who tend to have more resources. Given the dramatic changes in both the health insurance landscape and the government’s role in the provision of health care services over the ensuing 80 years, this policy should be revisited by policymakers.

Related Content

2025

Author

-

References

Cranor, Taylor, Jacob Goldin, and Sarah Kotb. 2019. “Does Informing Employees About Tax Benefits Increase Take-Up? Evidence from EITC Notification Laws.” National Tax Journal, 72(2): 397–434.

Gillitzer, Christian, and Peer Ebbesen Skov. 2018. “The Use of Third-Party Information Reporting for Tax Deductions: Evidence and Implications from Charitable Deductions in Denmark.” Oxford Economic Papers, 70(3): 892–916.

Goda, Gopi Shah. 2025. “Subsidizing Medical Spending Through the Tax Code: Take-Up, Targeting and the Cost of Claiming.” National Bureau of Economic Research.

Goda, Gopi Shah, Ithai Lurie, Priyanka S. Parikh, and Chelsea Swete. 2025. “The Distributional Implications of the Itemized Medical Deduction.” Tax Policy and the Economy, 38.

Guyton, John, Dayanand S. Manoli, Brenda Schafer, and Michael Sebastiani. 2016. “Reminders & Recidivism: Evidence from Tax Filing & EITC Participation Among Low-Income Nonfilers.” National Bureau of Economic Research.

Jones, Damon. 2010. “Information, Preferences, and Public Benefit Participation: Experimental Evidence from the Advance EITC and 401(k) Savings.” American Economic Journal: Applied Economics, 2(2): 147–163.

Kopczuk, Wojciech, and Cristian Pop-Eleches. 2007. “Electronic Filing, Tax Preparers and Participation in the Earned Income Tax Credit.” Journal of Public Economics, 91(7): 1351–1367.

Linos, Elizabeth, Allen Prohofsky, Aparna Ramesh, Jesse Rothstein, and Matthew Unrath. 2022. “Can Nudges Increase Take-Up of the EITC? Evidence from Multiple Field Experiments.” American Economic Journal: Economic Policy, 14(4): 432–452.

Reed, Louis S. 1967. “Private Health Insurance: Coverage and Financial Experience, 1940–66.” Social Security Bulletin, 30: 3.

Sierk, Caroll. 1966. “The Medical-Expense Deduction—Past, Present and Future.” Mercer Law Review, 17: 381.

-

Acknowledgements and disclosures

This research was made possible by support from the Institute of Consumer Money Management and the Peter G. Peterson Foundation. The author gratefully acknowledges her collaborators on related cited work that informed this piece, and gives special thanks to Aidan Creeron for providing valuable research assistance. The views expressed in this report are those of the author and do not represent the views of the funders, their officers, or employees.

-

Footnotes

- Reed (1967) reports that 19.5 million individuals were enrolled in plans that provided coverage for hospital benefits in 1942 (Table 5), and population data for 1942 were obtained from FRED Series B230RC0A052NBEA.

- Total out-of-pocket medical spending in 2022 was $471.4 billion as reported by “National Health Expenditures 2022 Highlights,” Office of the Actuary, Centers for Medicare and Medicaid Services, December 13, 2023.

- Total amounts deducted in 2022 from “Individual Income Tax Returns Complete Report, 2022,” Publication 1304 (Rev. 1-2025), Internal Revenue Service, Table 1.3. Forgone federal tax revenue reported from “Tax Expenditures – FY2025,” U.S. Treasury, Table 1 for fiscal year 2023 and “Estimates of Federal Tax Expenditures for Fiscal Years 2023-2027,” for fiscal year 2023.

- The IRS defines what medical expenses are deductible in IRS Publication 502.

- While similar in some respects, the IMD differs significantly from Health Savings Accounts (HSAs), which are custodial accounts that can be used to pay qualified medical expenses on a tax-free basis. Only those with high-deductible health plans are able to contribute to an HSA, and qualified medical expenses do not need to meet a threshold to qualify. More information is available in IRS Publication 969.

- This feature is similar to other so-called “tax expenditures” that reduce tax liabilities through deductions or exclusions that reduce the amount of income subject to tax.

- Note that this assumption does not fully account for those who fail to claim it but are unaware of potential tax savings for which they may qualify.

- Prior to the TCJA, the AGI threshold was 10% for taxpayers under age 65 and 7.5% for taxpayers over age 65. The TCJA equalized the threshold to 7.5% for all taxpayers.

- For example, the thresholds for Form 1098 and Form 1098-E are $600.

- An extensive literature on interventions designed to increase claiming of tax-related programs suggests that interventions that reduce the administrative burdens that people face when claiming tax benefits lead to higher claiming among eligible people (Kopczuk and Pop-Eleches 2007, Gillitzer and Skov 2018), but that informational interventions have limited success (Jones 2010, Guyton et al. 2016, Cranor, Goldin and Kotb 2019, Linos et al. 2022).

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

A little-known way the tax code subsidizes spending on health care

And what policymakers need to know about it

November 19, 2025