What is the FIM?

The Fiscal Impact Measure (FIM) is a tool created by the Hutchins Center to illustrate how much local, state and federal fiscal policy adds to or subtracts from overall economic growth. When the FIM is positive, policy is expansionary in the sense that it is pushing growth in real Gross Domestic Product (GDP) above its longer-run potential. When the FIM is negative, policy is lowering real GDP growth relative to potential. The FIM is broader than measures of fiscal impetus that rely on the size of the federal deficit because it includes the includes the direct effects of federal, state, and local government purchases as well as the more indirect effects of government taxes and government transfers, which affect private consumption. The FIM is closely related to a measure of fiscal stance developed by Federal Reserve Board staff (see Cashin et al. 2018).

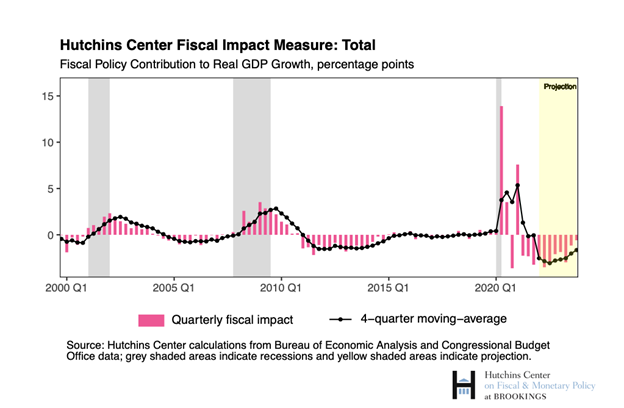

As the figure below illustrates, between 2008 and 2011, the years of the Obama stimulus (The American Recovery and Reinvestment Act) fiscal impact was positive, indicating that government policy was stimulative. For several years after, due to the spending sequesters, the fiscal impact was negative, indicating a restraint on growth.

Fiscal impact hovered around zero through the second half of the 2010s, indicating that fiscal policy was growing roughly in line with potential GDP during that time. With the arrival of the COVID-19 pandemic and three subsequent rounds of stimulus legislation, however, fiscal impact hit a historic high— boosting GDP growth by 13.9 percentage points in the second quarter of 2020 alone. As the spending from this pandemic legislation wanes, fiscal policy has become a drag on growth in recent quarters and remains negative through our projection period.

How is the FIM different from the size of the federal deficit?

The FIM is a broader and more timely measure of the effects of fiscal policy on the economy than is the federal deficit. The deficit is the difference between the flow of federal government spending and the flow of government revenues (taxes). The FIM is broader because it encompasses the effects of spending and tax policies at the state and local level as well as the federal government. In addition, the FIM estimates how tax and transfer policies affect private consumption, whereas the federal deficit simply reports the dollars transferred from the government to households and businesses. Finally, the FIM more precisely captures the timing of realized government expenditures on near-term measures of economic growth, relative to the slower-moving and budget-focused measure of the deficit.

How is the FIM different from BEA’s numbers?

Each quarter, the Bureau of Economic Analysis (BEA) measures how much local, state, and federal governments spend on goods and services and reports what contribution those expenditures made to the headline GDP number (see Table 1.1.2 in the GDP release, for example). The FIM is related to this measure, but estimates instead the contribution that government policies are making to GDP beyond the contribution they would make if they were growing in line with the longer-run, potential path of the economy. The FIM can be interpreted as a measure of how expansionary or contractionary fiscal policy is relative to the potential path of the economy.

How does the Hutchins Center construct its FIM Forecast?

The FIM Forecast takes a projected path for spending and tax revenues and projections of the economy and translates them into quarterly estimates of those policies’ contributions to GDP growth. The Hutchins Center uses budgetary and economic projections from the Congressional Budget Office to inform these forecasts. In most cases, we assume that current laws will remain in place over the projection period, but in some instances, we deviate from this assumption.

Do you actually forecast tax and spending policy at the state and local level?

No. We assume that nominal spending, taxes, and transfers at the state and local level will rise about in line with our projections of overall GDP growth, and then apply appropriate price deflators.

Authors

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).

Commentary

A guide to the Hutchins Center Fiscal Impact Measure

February 17, 2022