A version of this report was originally published in Health Affairs Forefront on June 16, 2022.

On May 13, 2019, Washington state’s governor, Jay Inslee, signed SHB 1087 establishing WA Cares, a state-level program to provide qualifying Washington residents up to $36,500 to cover the cost of long-term services and supports (LTSS)1.

The law was enacted to close a gap in our current policy landscape. An estimated 70 percent of people who reach the age of 65 will at some point in their remaining lives use some form of long-term medical care or aid with activities of daily living, at home or in an institution. And yet, such services get short shrift from current payers.

Medicaid covers LTSS for people with meager income and assets and accounted for 42.9 percent of all spending on long-term care. Medicare covers limited home or institutional care for people after they have spent three or more days in a hospital and accounted for 20.5 percent of LTSS spending. Private long-term care insurance plans covered only about 5 percent. Much of the rest is paid out of pocket by individuals or charitable organizations. All of these coverage options are fragmented and flawed in various ways.

What is more, these statistics, and the programs they describe, omit the imputed value of unpaid services provided by family and friends to millions of people of all ages with disabilities or limited capacity to perform activities of daily living. The value of these services and the costs they impose on those who–out of love, kindness, or duty–provide these services must not be forgotten in weighing the value of public action to pay for LTSS.

It is against this backdrop, that Washington state created WA Cares.

After Enactment

The program is to be paid for by a payroll tax of 0.58 percent levied on all employees unless they attest that they have private LTSS insurance providing benefits at least equivalent to those available under the state plan. The plan does not cover the self-employed unless they “opt in.” The distinction between the treatment of employees and the self-employed reflects the fact that Washington has information on employee earnings through its state unemployment insurance and paid family and medical leave insurance programs, but, like eight other states, has no state-based income tax and therefore lacks easy access to data on self-employment income.

After enactment of WA Cares, administrators recognized that the law would create certain inequities. Washington workers who live in another state, workers resident under non-immigrant visas, and military spouses were all subject to the payroll tax but were unlikely to derive benefits from WA Cares because they would probably leave the state, and WA Cares bars non-residents from claiming benefits. In addition, veterans with at least 70 percent disability already qualify for benefits from the Veterans Administration equivalent to or better than offered under WA Cares.

To correct these problems, the state legislature passed amendments authorizing members of these four groups to apply for exemptions from the payroll tax. In addition, it authorized Native American tribes, which the original legislation did not cover, to opt in. Because of these changes in the plan, the amendments also pushed back the date on which taxes would first take effect (from January 1, 2022, to July 1, 2023) and when benefits would first be paid (from January 1, 2025, to July 1, 2026).

By early December 2021, 443,649 Washington employees—about 12 percent of employees in the state— attested that they had private long-term care coverage and were therefore exempt from the payroll tax.

Reports Of A Program’s Death, Greatly Exaggerated

In a recent Health Affairs Forefront article, Mark Warshawsky described the WA Cares program as “deeply unpopular, poorly designed, unstable, insolvent ab initio, perhaps illegal, and, without major changes, failed.” This death notice appeared just after the Washington state legislature amended and improved the program and before it was implemented. He presents no evidence that the program is unpopular. He treats as settled legal challenges by groups that had opposed enactment but that no court has upheld. He expressed doubt about the legitimacy of many workers’ attestations2 and cites an increase in the number of exemption claims in November 2021 to support his fear that a flood of additional dubious claims could drown WA Cares in adverse selection. In brief, he predicts that WA Cares is headed to the junk heap of failed good intentions.

With respect to exemption claims, the pace slowed considerably in December 2021 and since then has almost halted. From November 2021 until February 2022, an additional 28,718 people filed attestations but only 1,385 more did so by mid-April. All claims must be based on coverage in force before November 1, 2022, and no claims for any reason can be filed after 2022. And actuarial studies prepared by Milliman for the Washington state legislature incorporated the effects of adverse selection.

Furthermore, the Washington legislature recognized the possible adverse selection problem and instructed the commission responsible for overseeing WA Cares to explore ways to require recertification of attestations. Such a requirement, if enacted and coupled with a requirement to show documentation of coverage and to repay taxes that should have been paid (with interest), would greatly attenuate the basis for concern about adverse selection3.

Thus, the Washington legislature is in process of dealing with such past adverse selection as has occurred. And, with appropriate safeguards, the risk of a further increase in adverse selection is much diminished. Furthermore, the flow of opt-out requests has slowed to a trickle, and no opt-outs will be permitted after the end of this year.

The original WA Cares legislation contained a different sort of adverse-selection problem. The self-employed could elect to participate in the program or remain out, at their option. The self-employed with high earnings were more likely to remain out than would those with low earnings because the payroll tax is uncapped. Furthermore, most self-employed workers have been, are, or will be employed by others at some point in their working lives. They will be covered under WA Cares because they are employees, and under current policy they will not be taxed on self-employment income, unless they opt in, which seems unlikely. As a result, workers who have both employment and self-employment tax will pay less in tax than would employees with the same total income.

As described in an April 1, 2022, letter to state officials from Milliman’s chief actuary Christopher Giese, the actuarial studies of program revenues and expenditures incorporated both problems in their estimates of program costs. But the legislature did not initially provide guidance on how to deal, administratively, with workers as they change status from “employed” to “self-employed.”

In 2021, the legislature addressed this omission in part by requiring the self-employed who wish to participate in the program to opt in within three years of when premium collection begins. They remain enrolled and subject to tax on self-employment income (with credit toward benefits for each year that such income exceeds 500 times the state minimum hourly wage) unless they file a notice that they are no longer self-employed or that they have retired. To enforce this requirement, Washington will likely need to secure Internal Revenue Service (IRS) cooperation so that the state can verify self-employment income. Actuarial estimates described in the April 2022 Milliman letter indicate that this amendment slightly lowers program costs.

While this amendment is a step in the right direction, it does not go far enough, as some workers have discretion over whether to take compensation as ordinary wage income or through contract. Most importantly, treating employees and the self-employed differently serves no programmatic purpose.

To simplify administration and avoid any incentives to structure compensation to avoid the WA Cares tax, the state should seek IRS cooperation in verification of total W-2 and Schedule C income of everyone who participates in the WA Cares program, employed or self-employed, and base the payroll tax on the sum of W-2 earnings and Schedule C income. Such a “treaty” between the state and the IRS—which is desirable because Washington state has no state income tax—would increase program fairness, improve finances of WA Cares, and enable the state to greatly simplify the verification of earnings for everyone under this program.

Long-Term Financial Balance

In December 2020, Milliman published actuarial estimates commissioned by the Washington State Actuary indicating that WA Cares will run a substantial cash-flow surplus for the first 30 years of operation, building up a reserve that will top out at $12.3 billion (discounted to 2022 dollars). This surplus will result because benefits will start three years after tax collections begin; even then, the number of claimants will initially be small and increase only gradually. Thus, revenues (including interest earnings on accumulated reserves) are projected to exceed program expenditures until 2052.

After that, accumulated reserves will fall until 2076, when they are projected to be depleted, after which 70 percent to 85 percent of scheduled benefits will be payable out of incoming premium revenues, even if no action is taken to close the funding gap. Over 75 years, current projections indicate that revenues are sufficient to cover 87 percent of scheduled benefits.

These estimates take no account of projected savings to the state Medicaid program. WA Cares will enable some people to avoid using Medicaid at all and will reduce use by others. These savings, as the same Milliman actuarial estimates indicated, will amount to approximately 10 percent of projected program costs. Arguably, projections should treat Medicaid savings as an offset to the cost of WA Cares. If one counts this offset, then as of 2022, payroll tax revenues represent 97 percent of the cost of WA Cares net of Medicaid savings over the succeeding 75 years. In addition, the state is considering whether to authorize investment of a part of reserves in private stocks and bonds, which would boost expected yields.

The bottom line is that many of the concerns that Warshawsky expressed have been dealt with by legislation. Others were based on an exaggerated reading of available evidence. If one credits WA Cares with future reductions in Medicaid spending that the program will generate, the program is almost, but not quite, funded for the period through 2097.

Sustainable Solvency

This is not quite the end of the story, however. As afficionados of the annually revised trust fund projections of the Social Security (Old-Age, Survivors, and Disability Insurance) system are aware, the course of projections of balance over time depends not only on the accuracy of assumptions used but also on the projection period to which projections apply. Even if every revenue and expenditure projection precisely matches what subsequently happens and those revenues cover all spending over the projection period as of the base year, projections of the balance between revenues and expenditures can move into surplus or deficit in successive years entirely because of the passage of time.

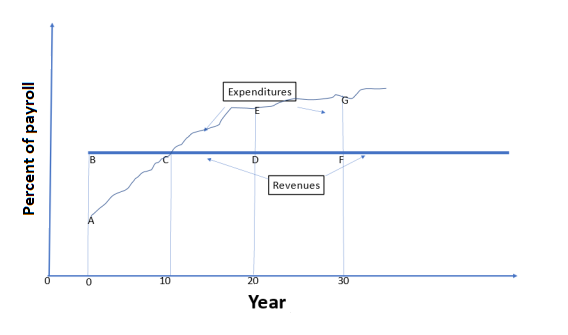

Exhibit 1 shows a hypothetical pattern of revenues and expenditures over time that produces such a result.

Exhibit 1: The balance between long-term revenues and expenditures can shift over time even if projections of revenues and expenditures do not change

Source: Author’s illustrative example.

As drawn, projections based on the 20 years after year one show approximate balance between revenues (represented by the area below the bold line BCD from time 0 to time 20) and expenditures (represented by the area below the lighter line ACE). Early surpluses (shown by the area ABC) offset later deficits (shown by the area CDE). Move forward to year 10, however, and a projection over the succeeding 20 years indicates a deficit (shown by the area CFG), although the annual projections of spending and revenues in each year are unchanged. To maintain financial balance over succeeding 20-year periods, it is necessary either to raise revenues or cut expenditures.

Projections of revenues and outlays under WA Cares likewise show early surpluses followed by later deficits. Washington state has chosen to follow the practice of the Social Security Administration by presenting projections 75 years into the future. Over this period, actuarial estimates indicate that the present value of WA Cares revenues do not quite cover the present value of outlays. Were one to focus on a 50-year window, legislated revenues are more than sufficient to cover benefits. The key point is that over time, the profile of revenues and expenditures, if realized, means that financial balance in WA Cares will tend to turn negative.

Current law requires the Office of the State Actuary to report every two years on the projected balance of revenues and expenditures over successive 75-year windows. Such projections are quite likely to show emerging and growing long-term deficits, even as WA Cares reserves are growing. Current law requires the commission to present options to raise future revenues or cut future benefits to eliminate any deficits that actuarial projections indicate. But current law does not make implementation of those recommendations automatic unless the legislature enacts alternative equivalent measures.

Because WA Cares will have large and growing accumulated reserves for many years, even as actuarial projections indicate emerging long-term deficits, the state legislature may be tempted to delay action to restore long-term balance, much as Congress has delayed action to close projected long-term deficits in Social Security because that program has sizeable accumulated reserves.

Reports that show persistent and growing projected long-term deficits could undermine support for WA Cares. Legislators can forestall erosion of political support caused by repeated projections of long-term deficits by enacting a rule that the commission’s recommendations on how to maintain long-term financial balance will take effect automatically unless the legislators enact an equivalent alternative. Such a measure would discourage future legislators from simply “kicking the can down the road,” while preserving their responsibility for deciding on just how to maintain long-term balance.

Of course, underlying economic, demographic, and administrative trends may change as time passes, causing shifts in program balance independently of the passage of time. For example, the legislature is considering and could authorize investing a portion of reserves in higher-yielding assets than current law permits. Such a move could defer or forestall required adjustments in payroll tax rates or benefits. Higher-than-projected wage growth would increase revenues and likewise delay or avoid the need to raise payroll taxes or cut benefits. Alternatively, events such as an economic slowdown or reduced labor force growth could reduce revenues more than projected benefits. In either case, automatic adjustments would maintain financial balance and help preserve public confidence in WA Cares, while allowing future legislatures to modify the adjustments as they see fit.

Conclusion

Public policy makers face a large problem, and one that is sure to grow–how to fashion a system to help people pay for the cost of LTSS for those no longer able to take adequate care of themselves. How much of this problem should be left to individuals, their families, and their friends, how much to private insurance, and how much to collective support through public programs (social insurance or income-/means-tested benefits) is a large and challenging question about which well-intentioned people can and will disagree. Currently, Medicaid provides wide, if uneven, coverage for the needs of those with little income and few assets, a system that directly helps many but is thought to reduce the incentive of others to buy private insurance coverage.

After careful study, the Washington state legislature established the first state-based program to help residents finance LTSS—a modest but important step. It provides state residents with financial backing sufficient for short institutional stays or for roughly one year of in-home assistance. Any state action faces many difficult challenges including, but not limited to, those same challenges that national legislators must also face. The Washington legislature failed initially to address or to recognize certain of these problems but corrected them quickly with specific amendments.

Other problems remain. The first and overarching challenge is that tying coverage to state residency is inherently problematic. Social insurance coverage is best managed at the national level given the fact of inter-state mobility. Pending such a national decision, the only question for a state interested in providing some supports for state residents is how to go about that job in a responsible manner. Washington has met that challenge. Washington faces a problem all states without an income tax and the information it generates must confront: how to deal with the self-employed. A second question for a state legislature is whether to build into current law automatic adjustments for future financial imbalances that may emerge or that are built into the current system. It appears that the Washington payroll tax rate of 0.58 percent may be insufficient to pay for currently promised benefits, a situation that would increase the likelihood that unfriendly future state administrations might terminate the program.

One point is clear. The decision by the Washington legislature to delay implementation of WA Cares was very much not a confession of failure. Rather, it was a prudent action to give time to implement modifications to correct genuine problems in the original legislation. Legislators in other states can look to WA Cares for a model of how to take modest steps to help people build a nest egg to help defray costs of long-term services and supports that most will find they need.

Original publication information:

Henry J. Aaron, The Future Of WA Cares: A Response To Warshawsky, Health Affairs Forefront, June 16, 2022, https://www.healthaffairs.org/do/10.1377/forefront.20220615.206408

Copyright © [2022] Health Affairs by Project HOPE – The People-to-People Health Foundation, Inc.

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

Author

-

Footnotes

- Under current law, benefits may be indexed for as much as price inflation according to a Washington State-based CPI. Consideration is now being given to mandating full price indexation. Such a step would serve two purposes, reducing or eliminating the risk that price inflation could erode benefits and facilitating the design and pricing of private insurance coverage to supplement WA Cares benefits, an objective that current law mandates the Long-term Supports Services and Services Supports Commission to pursue.

- The skepticism was two-fold. First, private long-term care insurance covered only 5 percent of the national population. Second, those attesting to private coverage had higher-than-average earnings, and their exclusion would deprive the plan of revenues needed to pay for benefits. The difference between the proportion of workers claiming exemptions and the share of people nationally who carry long-term care insurance is significant and may be even larger than he suggests. The hyperlink source Warshawsky cites that 7.5 million “people” had long-term care insurance in 2020 but did not indicate the groups to which this account applied. The labor force in February 2020 (pre-COVID-19) was 164.6 million. This number includes the self-employed, who are exempt from WA Cares unless they choose to join. If the long-term care coverage number applies to groups other than those currently in the labor force, the 5 percent estimate may overstate the share of the workforce covered by long-term care insurance. But the actuarial computations on which the state relied had already factored in the costs of exemptions.

- Even with documented recertification, adverse selection could remain from past claims, as those who made attestations of coverage have higher earnings than average, as Warshawsky observed–$63.60 (twice statewide average earnings if earned for 50 full-time weeks a year). But the likelihood of much additional adverse selection is negligible, given the decline in claims to a trickle. Furthermore, the actuarial studies undergirding WA Cares have already taken account of such adverse selection and built it in to their estimates of program costs.

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).