Introduction

A founding principle of The Hamilton Project’s economic strategy is that long-term prosperity is best achieved by fostering economic growth and broad participation in that growth. This strategy includes an essential role for effective government to make much-needed public investments. This month The Hamilton Project is focusing on the need for public investments in our nation’s transportation infrastructure with the release of a new discussion paper by Roger Altman of Evercore, Aaron Klein of the Bipartisan Policy Center, and Alan B. Krueger of Princeton University, entitled “Financing U.S. Transportation Infrastructure in the 21st Century.” As part of this focus, we offer this primer document, “Racing Ahead or Falling Behind? Six Facts about Transportation Infrastructure in the United States.” While each part of the nation’s infrastructure is vital—from the electrical grid that powers our cities to the water systems that deliver clean drinking water around the country—these facts focus on the state of investment in transportation-related infrastructure.

The economy of the United States depends on our nation’s transportation infrastructure. Every day, tens of millions of people commute to work in the United States using public roads and transportation systems. Billions of dollars’ worth of freight is transported using the nation’s highways, railroads, ports, and inland waterways (Fact 3). Significant public investment—at all levels of government—is required to maintain this system, conduct periodic repairs, and expand our nation’s transportation systems to safely handle movement of greater numbers of goods and people. A well-functioning system of mass transportation is both a substitute for and a complement to our nation’s highway system (Fact 4), but funding for these systems is also stretched thin.

The facts make it clear that the state of public financing for transportation infrastructure warrants serious attention. Federal spending as a share of GDP has fallen (Fact 1) and the federal Highway Trust Fund (HTF)—the designated source of revenue for spending on our nation’s highways—is about to run out of money (Fact 2). The primary source of funding for the HTF is the federal gas tax, but that tax has not been raised since 1993. Of course, state and local governments also play an active role in both the funding and building of infrastructure projects. Interestingly, there is large variation across states in both their reliance on state-level gas taxes (Fact 5) and the amount of federal funding states receive for the construction and maintenance of roads (Fact 6).

An efficient and reliable transportation infrastructure facilitates the transactions that enable the economy to grow and to create private sector jobs. Many observers agree on the need for increased investment in America’s aging infrastructure, including roads, bridges, and airports. However, determining how to fund and finance infrastructure investment presents important policy and political challenges. The purpose of this document is to provide objective background facts to help guide those necessary policy and political discussions.

Read The Facts

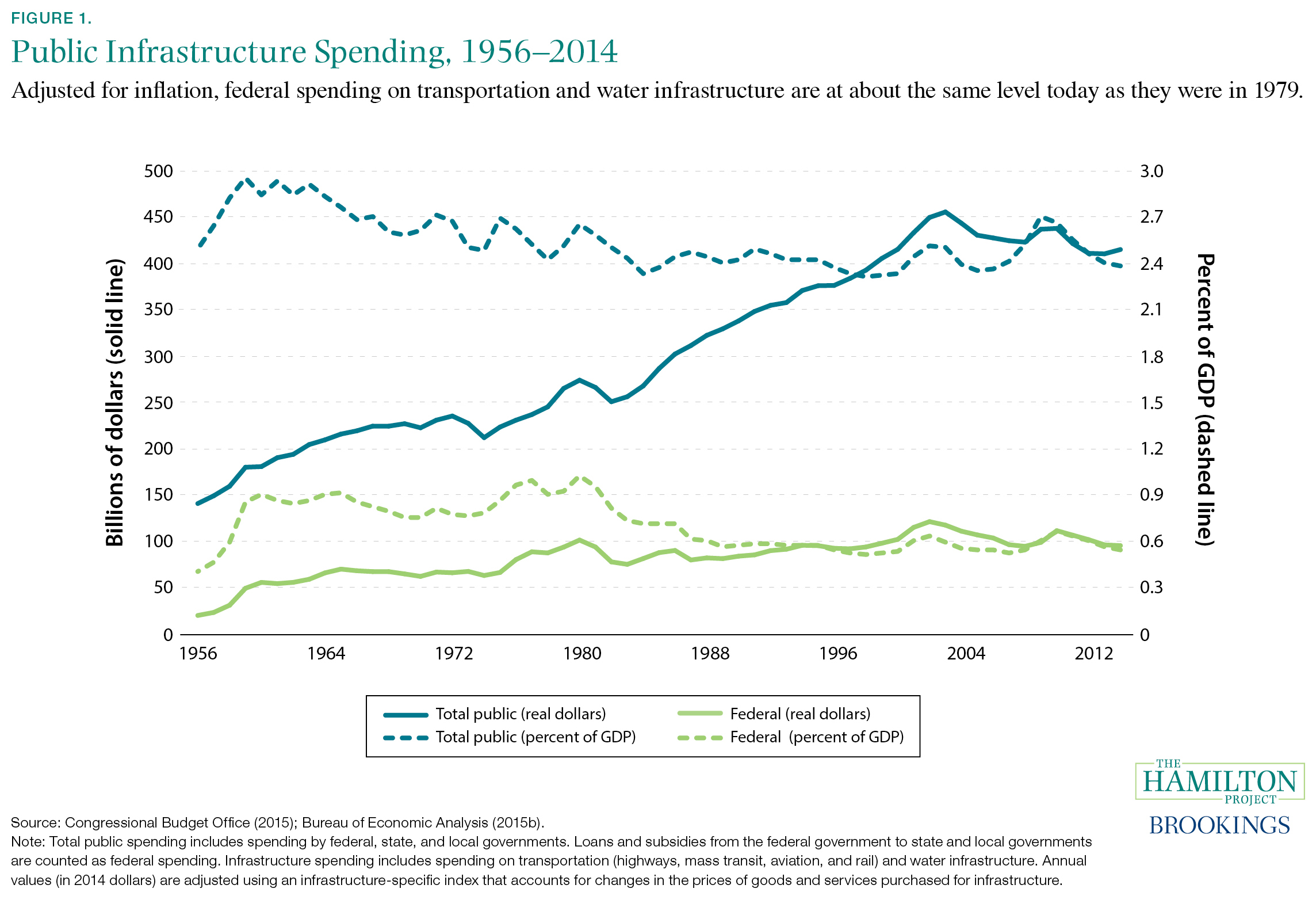

Fact 1. As a share of GDP, public infrastructure spending has been stagnant between 1979 and 2014.

Figure 1. Adjusted for inflation, federal dollars spent on transportation and water infrastructure are at about the same level today as they were in 1979.

Public infrastructure spending from all levels of government totaled $416 billion in 2014—$41 billion (9 percent) less than its peak of $457 billion in 2003 (solid blue line in the figure; Congressional Budget Office [CBO] 2015). This total includes spending on highways, mass transit, rail, aviation, ports, waterways, dams, and water supply networks. As shown in the figure, total public spending on infrastructure as a share of GDP (dashed blue line) peaked in the late 1950s, during the initial stages of construction of the Interstate Highway System. Since the mid-1980s, however, total public spending as a share of GDP has remained relatively flat.

Infrastructure spending by the federal government, as indicated by the solid green line, has been relatively flat over the past thirty-five years, equaling about $96 billion in both 1979 and 2014. Some of this money covers direct outlays on capital and operations and maintenance, but much of it is in the form of grants and loan subsidies to state and local governments. In 2014 these intergovernmental transfers constituted 70 percent of federal infrastructure dollars; 90 percent of these funds went specifically to capital projects rather than to operations and maintenance (CBO 2015).

The majority of infrastructure spending consists of funds raised by state and local governments—reflected in the figure as the difference between the blue and green lines—and is used primarily for operations and maintenance. Over the past thirty-five years, this category of spending nearly doubled from $170 billion to $320 billion. Because federal spending was flat, the share of overall infrastructure spending coming solely from state and local governments increased from 63 percent in 1980 to 77 percent in 2014.

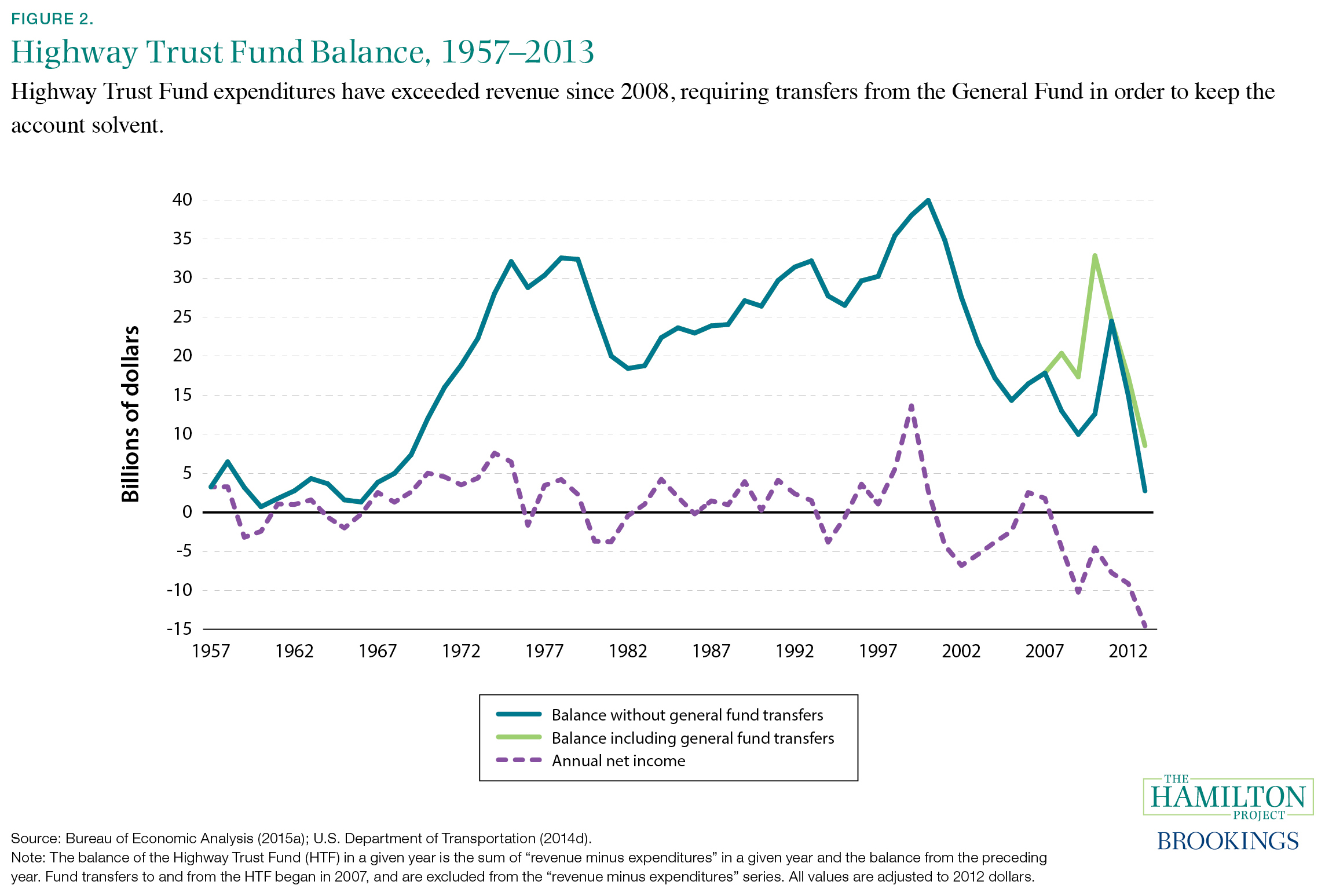

Fact 2. The Highway Trust Fund is at its lowest balance since 1969, and is set to run out of money by summer of 2015.

Figure 2. Highway Trust Fund expenditures have exceeded revenue since 2008, requiring transfers from the General Fund in order to keep the account solvent.

The HTF, established by the Federal-Aid Highway Act of 1956, was the first dedicated funding source for highway construction and maintenance (U.S. Department of Transportation [USDOT] 2015a). Supported by a federal motor fuels tax—as well as additional taxes on tires and trucks—the HTF’s revenue helps pay for federal highways and, through grants to other levels of government, many state roads as well. Since 1982 HTF revenues have also been set aside to support mass transit (USDOT 2015a).

For most of its history, the HTF was well in the black, even as the Interstate Highway System was being built. Over the past fifteen years, however, expenditures have routinely exceeded revenues (as shown by the dashed purple line’s position below the horizontal axis). As a consequence, the HTF’s balance (shown by the blue line) has plummeted to levels last reached in the late 1960s. This resulting shortfall has led Congress to make repeated transfers from general revenue to keep the HTF solvent (the green line). If these transfers do not continue, the HTF is expected to be bankrupt by summer of 2015 (CBO 2014).

If avoiding dependence on transfers from the General Fund is a future objective of the HTF, increasing the federal tax on gasoline is one way to achieve it. The federal tax on gasoline has been fixed at 18.4 cents per gallon (in nominal terms) since 1993, even as average fuel efficiency has improved and the growth in total miles driven has slowed (USDOT 2014b, 2015b). The CBO estimates that raising the gas tax by between 10 and 15 cents per gallon would be sufficient to cover expected HTF shortfalls over the next ten years (CBO 2014).

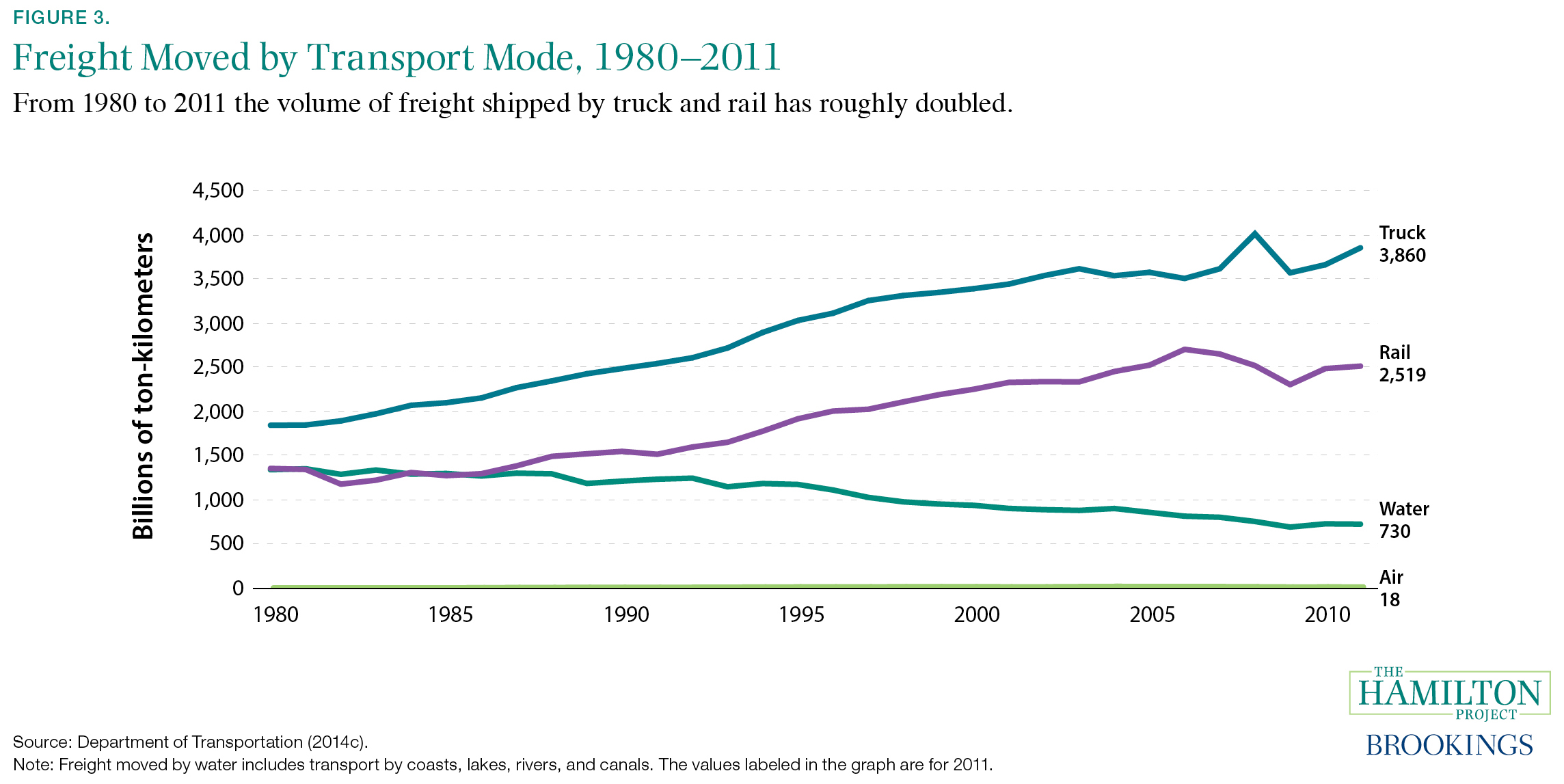

Fact 3. Truck and rail together accounted for 90 percent of the total freight moved in 2011, up from 70 percent in 1980.

Figure 3. From 1980 to 2011 the volume of freight shipped by truck and rail has roughly doubled.

Truck and rail are the dominant forms for moving freight in the United States. As shown in the figure, in 2011 trucks transported almost 3.9 trillion ton-kilometers of cargo, an increase of 109 percent from 1980. (A ton-kilometer is the movement of one ton of goods by one kilometer, thus accounting for both weight and distance.) By the same measure, freight moved by rail has increased by 85 percent. Air cargo has grown even more rapidly, by 168 percent, but still accounts for only a tiny sliver—0.25 percent—of all freight moved. This growth adds to the wear and tear on transportation infrastructure (Patton 2007), investment in which, as documented in Fact 1, has slowed.

In contrast, freight moved by waterways—including coasts, lakes, rivers, and canals—has fallen by 46 percent over the same period. Because of this decline, truck and rail together now move 90 percent of the country’s cargo, up from 70 percent in 1980. (All of these figures include only domestic cargo, and exclude imports and exports.)

However, it should be noted that the amount of freight moved is not the same as the value of freight moved. In 2012 the average value per ton of air cargo (including freight moved by both air and other transport modes) was almost $75,000 (in 2012 dollars), or about eighty times the average value of cargo moved by truck (about $900 per ton), and roughly 250 times the average value of water and rail cargo (each about $300 per ton; Center for Transportation Analysis [CTA] 2015). By total value, truck accounts for 91 percent of freight, rail for almost 5 percent, air for 3 percent, and water just 2 percent.

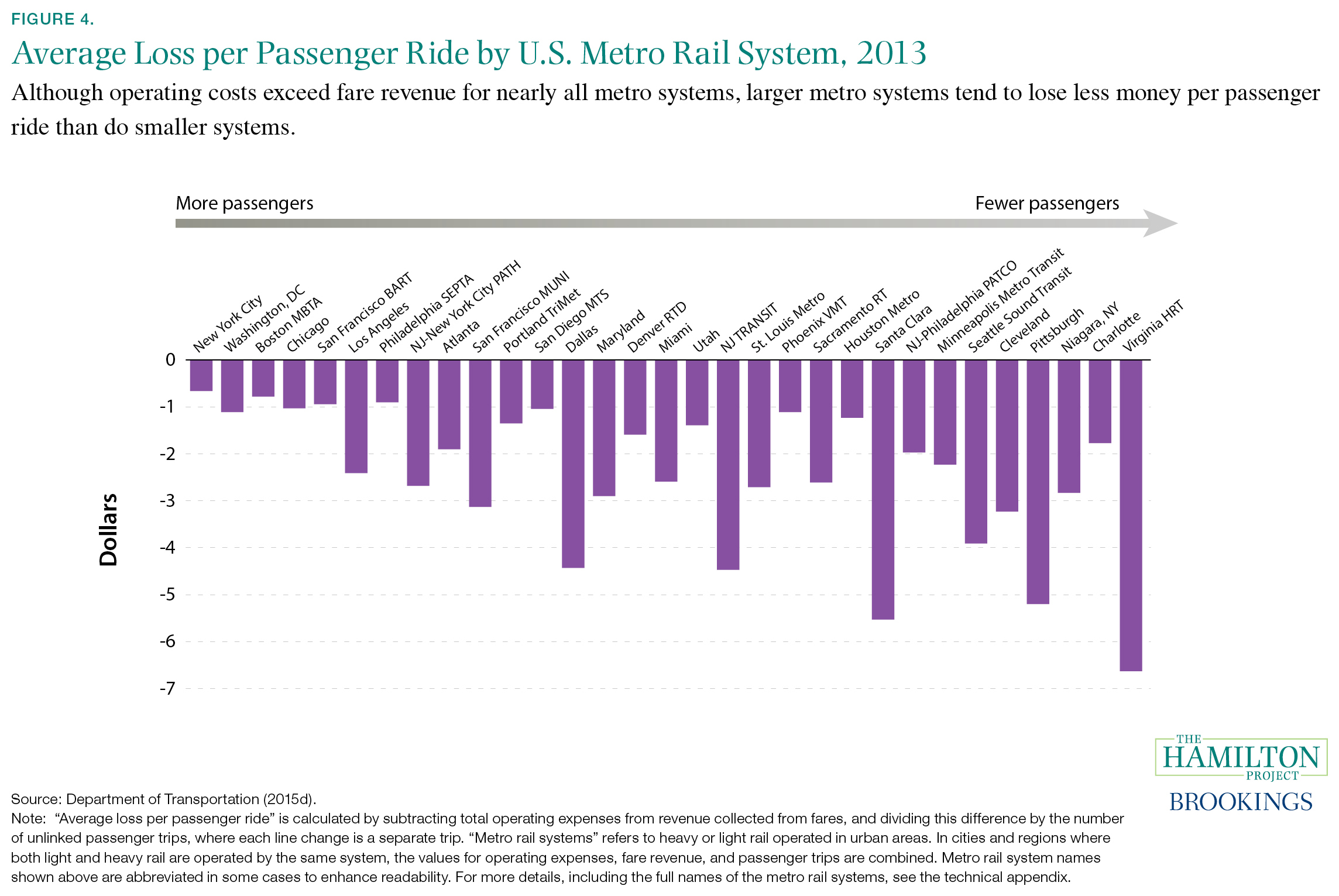

Fact 4. In every metro rail system, passenger fares do not cover operating costs.

Figure 4. Although operating costs exceed fare revenue for nearly all metro systems, larger metro systems tend to lose less money per passenger ride than do smaller systems.

Of the more than 1,800 mass transit systems in the United States—including those running trains, buses, or other transport modes—roughly 2 percent reported that fare revenue exceeded operating expenses in 2013 (USDOT 2015d). As shown in the figure, metro rail systems—including heavy rail, such as subways and elevated trains, and light rail, which operates at street level—all operate at a loss (USDOT 2015c).

In general, average losses per trip are smaller for larger metro systems. For instance, metro riders in the five largest systems—those in New York, Washington, DC, Boston, Chicago, and the San Francisco Bay Area—pay about a dollar less than the actual cost of each trip. Riders of the smaller systems in Seattle, Cleveland, and Pittsburgh, on the other hand, pay approximately four dollars less than the cost of each trip. Of course, these are average losses, and some riders’ trips are more expensive than others, primarily depending on the distance traveled. (Notably, these cost figures count each line transfer as a separate trip; USDOT 2015c).

Like roads, mass transit is not self-sustaining: both roads and mass transit require a combination of user fees and other government funding to pay for operations, maintenance, and expansion. There is evidence that government subsidies may be justified for mass transit. Development of transit stations has been linked to higher land values, higher office rents, and lower office vacancy rates (Cervero 1994; Knapp, Ding, and Hopkins 2001). Mass transit also alleviates congestion for drivers: a strike by Los Angeles transit workers that temporarily shut down service in 2003 resulted in a 47 percent increase in highway delays (Anderson 2014).

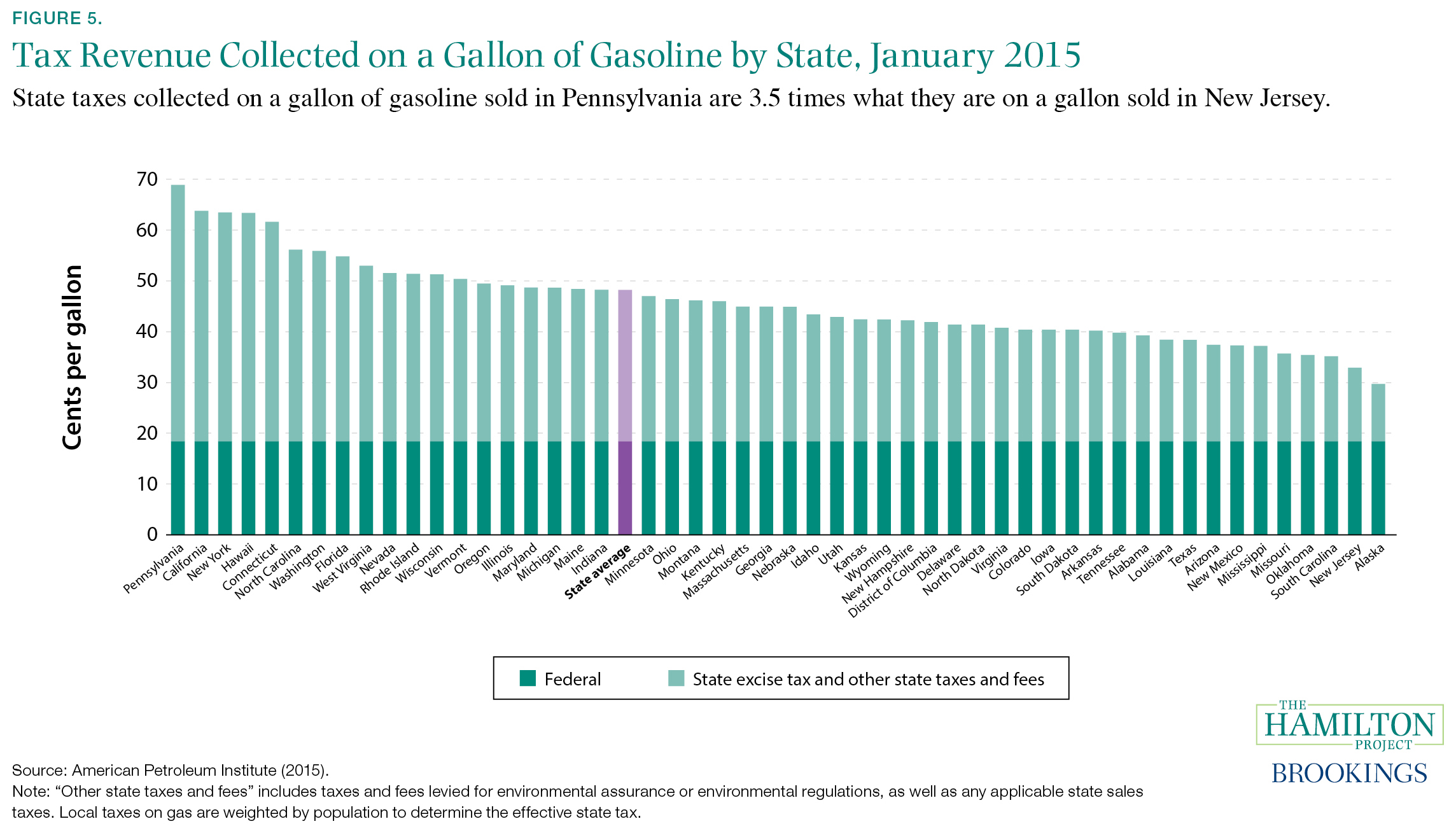

Fact 5. Taxes and fees levied on gasoline vary widely across states, ranging from 11.3 cents to 50.5 cents per gallon.

Figure 5. State taxes collected on a gallon of gasoline sold in Pennsylvania are 3.5 times what they are on a gallon sold in New Jersey.

Several different taxes and fees are levied on gasoline in order to support U.S. roads and transit, including federal taxes, state taxes and fees, and, in some cases, local government taxes (American Petroleum Institute 2015). Federal taxes, which are constant across states, amount to 18.4 cents per gallon—of which 15.44 cents go to the highway portion of the Highway Trust Fund (HTF), 2.86 cents to the mass transit portion of the HTF, and 0.1 cent to maintaining underground storage tanks (USDOT 2014a).

State taxes on gasoline vary considerably. As of early 2015 Pennsylvania levied the highest state tax, at 50.5 cents per gallon. Its neighbor across the Delaware River, New Jersey, charged less than a third as much, at 14.5 cents per gallon; the typical state levied a tax of about 29 cents per gallon (American Petroleum Institute 2015).

Unlike the federal gasoline tax, state taxes on gasoline have been raised a number of times in recent years (Auxier 2014). Since 1993, the last time the federal tax on gasoline was increased, twenty-one states have raised their gas tax by more than 5 cents per gallon, and eleven states have raised their gas tax by more than 10 cents per gallon (Auxier). Nonetheless, because most states (similar to the federal government) do not automatically adjust gas taxes for inflation, the real tax rate on a gallon of gasoline today is lower than it was in 1993 in forty-one states (Auxier).

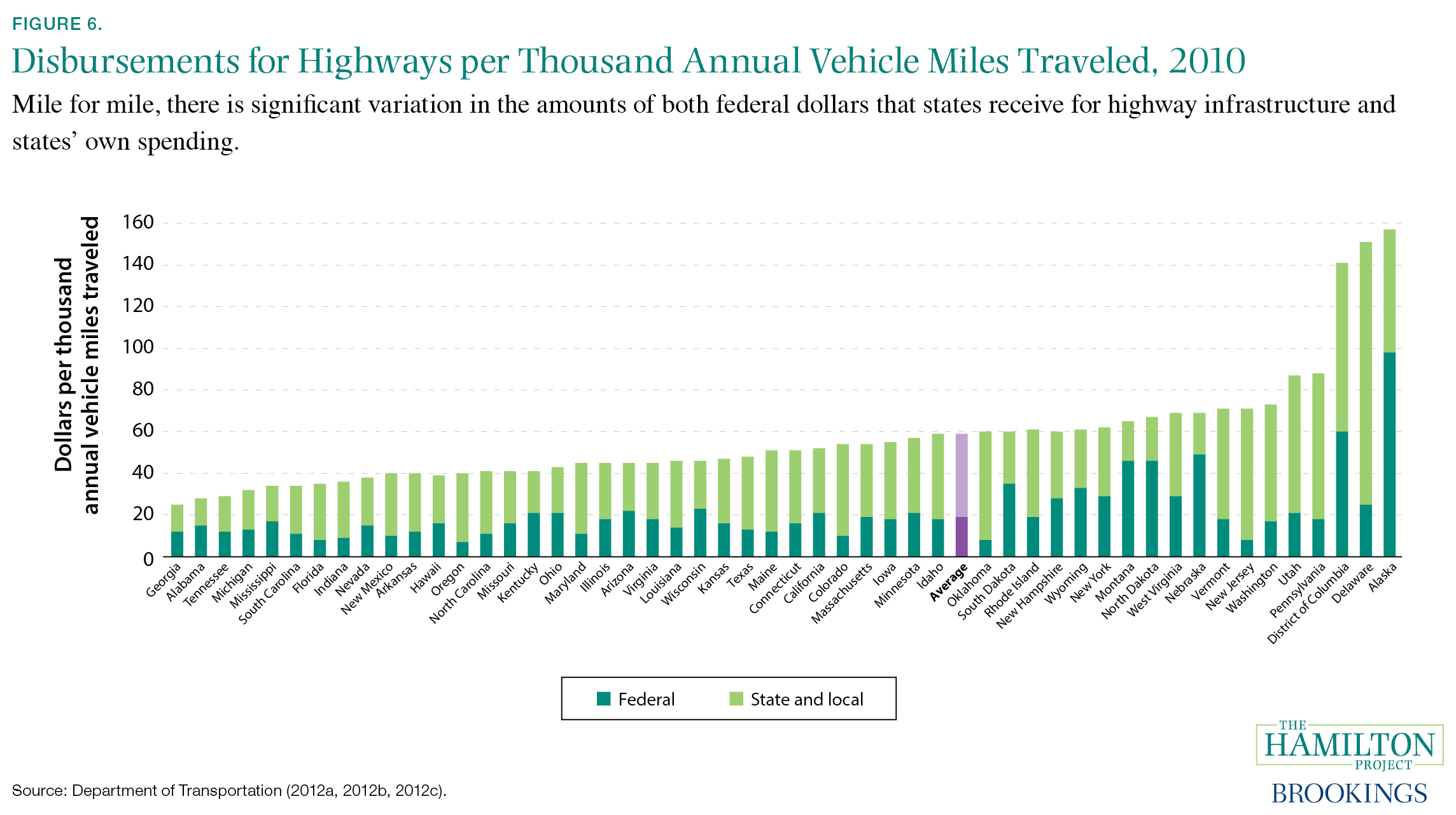

Fact 6. Controlling for miles driven, total spending on highways in some states is three times as much as in others.

Figure 6. Mile for mile, there is significant variation in the amounts of both federal dollars that states receive for highway infrastructure and states’ own spending.

State and local governments account for the majority of outlays on roads and highways, using both their own money and federally provided funds. Yet, even when adjusting for the total number of miles driven, total spending varies tremendously across states. For example, Michigan, the birthplace of the American automobile, spends a total of about $34 on highways for every thousand vehicle miles driven, while Pennsylvania—which has comparable levels of driving—spends nearly three times as much, at $88 for every thousand vehicles miles driven (including both federal and state sources of money).

There is substantial variation in the amount of federal funding that states receive for highway spending (dark green bars), and these amounts are not closely tied to the amount of driving in each state. For example, in 2010 Tennessee and New Jersey recorded a similar number of vehicle miles traveled—70.4 billion and 73.0 billion, respectively (USDOT 2012c). However, Tennessee received 42 percent more funding from the federal government than New Jersey did: $877 million versus $619 million. In fact, after adjusting for the amount of driving, the level of federal highway funding in some states, such as Wyoming and Montana, exceeds the total level of funding—federal plus state and local—in others, such as Florida and Indiana.

To more closely align the level of federal support with the level of driving, in 2014 apportionments were adjusted so that each state receives at least 95 percent of the dollars it contributes to the Highway Trust Fund (USDOT 2013). However, this apportionment formula does not recognize contributions through general fund revenue that has been used to shore up the HTF (see Fact 2). Because higher-income states disproportionately contribute to general tax revenue, to the extent that general fund revenue is increasingly used to support the HTF, states such as California, Massachusetts, and New York will effectively subsidize road construction and maintenance in states such as Georgia, Texas, and Montana (Puentes and Tomer 2009).

Technical Appendix

Fact 1. As a share of GDP, public infrastructure spending has been stagnant between 1979 and 2014.

Figure 1. Public Infrastructure Spending, 1956–2014

Source: Bureau of Economic Analysis (2015b); Congressional Budget Office (2015).

Note: Estimates of federal, state, and local spending on infrastructure came from the CBO (2015). Federal spending data originally came from the Office of Management and Budget. State and local spending data originally came from the U.S. Census Bureau. The CBO converted nominal estimates into real values using an infrastructure-specific index that accounts for changes in the price of goods and services purchased for infrastructure. Total public infrastructure spending is the sum of federal spending and state and local spending. To calculate the share of GDP spent on infrastructure in each year, we construct annual shares using nominal infrastructure spending amounts (from CBO 2015) and nominal GDP numbers (from BEA 2015b) in each given year.

Fact 2. The Highway Trust Fund is at its lowest balance since 1969, and is set to run out of money by summer of 2015.

Figure 2. Highway Trust Fund Balance, 1957–2013

Source: Bureau of Economic Analysis (2015a); U.S. Department of Transportation (2014d).

Note: Data for the Highway Trust Fund (HTF) and Mass Transit Trust Fund came from U.S. Department of Transportation (USDOT; 2014d). In all three series, the HTF balance is equal to the sum of annual values for the Mass Transit Trust Fund and annual values for the HTF. “Balance without General Fund transfers” is equal to the annual closing balance for that year minus the net transfers for that year. “Revenue minus expenditures” is equal to the total income from the HTF and Mass Transit Trust Fund minus the total expenditures from the HTF and Mass Transit Trust Fund, and excludes net transfers. All values are adjusted to 2012 dollars using the GDP deflator, which came from BEA (2015b).

Fact 3. Truck and rail together accounted for 90 percent of the total freight moved in 2011, up from 70 percent in 1980.

Figure 3. Freight Moved by Transport Mode, 1980–2011

Source: Department of Transportation (2014c).

Note: Data on volume of freight shipped came from USDOT (2014c). The Bureau of Transportation Statistics notes that values for ton-kilometers of freight moved in the United States by transport mode are collected from a number of sources, including the Freight Analysis Framework of the Federal Highway Administration, the Air Carrier Statistics Green Book authored by the Office of Airline Information within the Bureau of Transportation Statistics, the Surface Transportation Board’s Waybill Sample (as estimated by the Association of American Railroads), and the Highway Statistics series authored by the Federal Highway Administration. Freight moved by water includes transport by coasts, lakes, rivers, and canals.

Fact 4. In every metro rail system, passenger fares do not cover operating costs.

Figure 4. Average Loss per Passenger Ride, U.S. Metro Rail Systems, 2013

Source: Department of Transportation (2015d).

Note: Data on operating expenses, revenue collected from fares, and unlinked passenger trips came from USDOT (2015d). “Average loss per passenger ride” is calculated by subtracting total operating expenses from revenue collected from fares, and dividing the net of these values by the number of unlinked passenger trips. In cities where both light and heavy rail are operated by the same system, the values for operating expenses, fare revenue, and passenger trips are combined.

“Metro rail systems” refers to heavy or light rail operated in urban areas. Metro rail systems that lack data in 2013 are excluded from the figure, as are data for metro rail in Puerto Rico. Staten Island Rapid Transit Operating Authority—reported separately in the table, but a part of the Metropolitan Transportation Authority of New York—is included as a part of New York City’s metro rail system in the figure. Metro rail system names are abbreviated to the city name if the metro rail system chiefly or solely operates in the jurisdiction of that city. If the rail system has significant operations outside the host city, if there are multiple independent rail systems operating within the same city, or if the name of the metro system does not have the name of the host city in it, then the commonly used name or acronym by which the metro rail system is referred is included in the figure after the name of the host city of operations. This logic also applies if the metro rail system is regionally based. See appendix table 1 for the full list of metro systems.

Fact 5. Taxes and fees levied on gasoline vary widely across states, ranging from 11.3 cents to 50.5 cents per gallon.

Figure 5. Tax Revenue Collected on a Gallon of Gasoline in January 2015, by State

Source: American Petroleum Institute (2015).

Note: Taxes on gasoline are divided between federal excise taxes and state taxes and fees: state taxes and fees consist of state taxes on gasoline, as well as other state and local taxes and fees that affect the price of gasoline. Local taxes on gas are weighted by population to determine the effective state tax.

Fact 6. Controlling for miles driven, total spending on highways in some states is three times as much as in others.

Figure 6. Expenditures on Highways per Thousand Annual Vehicle Miles Traveled in 2010

Source: Department of Transportation (2012a, 2012b, 2012c).

Note: Data on total disbursements for highways in 2010 for each state came from USDOT (2012b). Data on federal disbursements for highways in 2010 for each state came from USDOT (2012a). Data on vehicle miles traveled in 2010 for each state came from USDOT (2012c). For both federal and total disbursements, disbursements per vehicle mile traveled were calculated by dividing disbursements in each state in 2010 by the vehicle miles traveled in that state in 2010.

Appendix Table 1: Metro Rail System Key

| Metro Rail System Name Shown in Figure | Full Metro Rail System Name | Mode | Fare Revenues Earned | Total Operating Expenses | Unlinked Passenger Trips |

|---|---|---|---|---|---|

| New York City | Metropolitan Transit Authority (MTA) New York City Transit (NYCT) | HR | 3,038,009,034 | 4,806,247,870 | 2,663,461,884 |

| Washington, DC | Washington Metropolitan Area Transit Authority (WMATA) | HR | 605,538,195 | 909,456,911 | 273,828,461 |

| Boston MBTA | Massachusetts Bay Transportation Authority (MBTA) | HR + LR | 281,792,807 | 467,311,677 | 238,746,106 |

| Chicago | Chicago Transit Authority (CTA) | HR | 278,183,527 | 513,644,769 | 229,113,934 |

| San Francisco BART | San Francisco Bay Area Rapid Transit District (BART) | HR | 406,055,540 | 525,014,638 | 126,546,495 |

| Los Angeles | Los Angeles County Metropolitan Transportation Authority (Metro) | HR + LR | 79,318,221 | 351,862,052 | 113,168,662 |

| Philadelphia SEPTA | Southeastern Pennsylvania Transportation Authority (SEPTA) | HR | 95,724,944 | 186,688,392 | 101,035,800 |

| NJ-New York City PATH | Port Authority Trans-Hudson Corporation (PATH) | HR | 141,335,701 | 330,513,965 | 70,547,639 |

| Atlanta | Metropolitan Atlanta Rapid Transit Authority (MARTA) | HR | 75,606,822 | 208,150,500 | 69,629,901 |

| San Francisco MUNI | San Francisco Municipal Railway (MUNI) | LR | 40,336,412 | 182,399,900 | 45,358,815 |

| Portland TriMet | Tri-County Metropolitan Transportation District of Oregon (TriMet) | LR | 46,442,818 | 99,326,676 | 39,174,406 |

| San Diego MTS | San Diego Metropolitan Transit System (MTS) | LR | 35,553,838 | 66,350,716 | 29,699,366 |

| Dallas | Dallas Area Rapid Transit (DART) | LR | 20,435,200 | 151,020,981 | 29,471,890 |

| Maryland | Maryland Transit Administration (MTA) | HR + LR | 20,254,093 | 89,418,764 | 23,855,754 |

| Denver RTD | Denver Regional Transportation District (RTD) | LR | 49,408,379 | 87,140,504 | 23,773,844 |

| Miami | Miami-Dade Transit (MDT) | HR | 22,845,276 | 77,684,301 | 21,198,687 |

| Utah | Utah Transit Authority (UTA) | LR | 19,004,819 | 45,452,097 | 18,997,860 |

| NJ TRANSIT | New Jersey Transit Corporation (NJ TRANSIT) | HR + LR | 19,484,408 | 100,684,938 | 18,169,307 |

| St. Louis Metro | Bi-State Development Agency of the Missouri-Illinois Metropolitan District (Metro) | LR | 18,608,919 | 64,814,600 | 17,054,484 |

| Phoenix VMT | Valley Metro Rail (VMR) | LR | 12,791,801 | 28,711,628 | 14,286,093 |

| Sacramento RT | Sacramento Regional Transit District (Sacramento RT) | LR | 14,729,637 | 50,023,110 | 13,513,471 |

| Houston Metro | Metropolitan Transit Authority of Harris County, Texas (Metro) | LR | 4,483,444 | 18,385,54 |

Related Content

Related Books

The Brookings Institution is committed to quality, independence, and impact.

We are supported by a diverse array of funders. In line with our values and policies, each Brookings publication represents the sole views of its author(s).